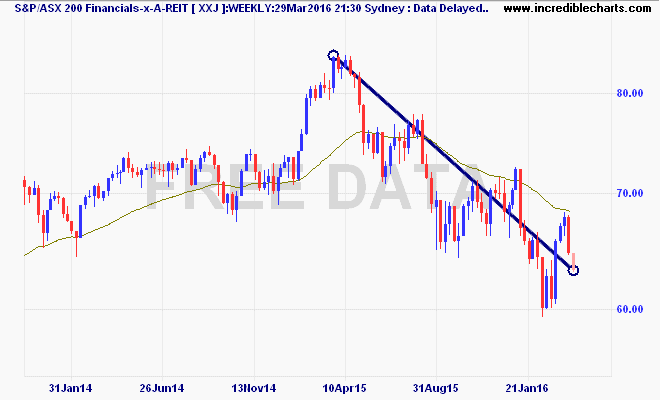

Banks are under pressure, with the financials index (XXJ) now down almost 25% since the 2015 high, as concern over bad and doubtful debt (BDD) charges is finally coming to the fore:

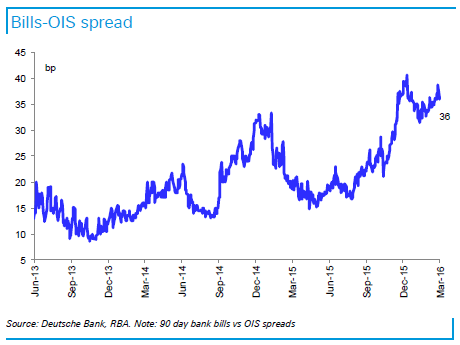

Of course the major headwind is wholesale funding costs, and Deutsche Bank are right to point out that this while major bank credit default swap (CDS) spreads have been improving slightly from its recent highs, its the ever widening bank bill spread that is starting to bite.

More:

Advertisement

Over the past month we have seen an improvement in major bank CDS spreads (5bps lower to 119bps), albeit off relatively high levels, the 90-day bank bill-OIS spread deteriorated by~2bps over the last month, and remains at elevated levels relative to the last few years.

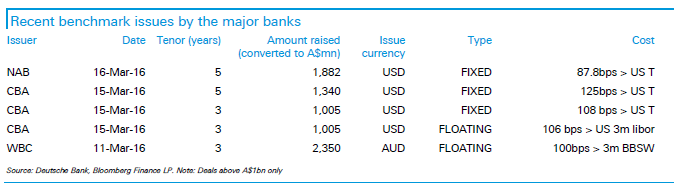

Recent bank debt issuances have shown that while funding is available, pricing has moved higher. Term funding costs at present are likely to be a little higher than the average of the back book. While this will still take time to work its way through bank margins, it does present downside risk to earnings and we think the likelihood of further repricing of housing and business loans remains high.

Westpac raised $2.35bn in 3-year money domestically at 100bps above BBSW, which is similar to NAB’s $2.25bn transaction in February (98bps above BBSW). However it is ~12bps more expensive than ANZ’s $1.4bn transaction in January (88bps above BBSW).

CBA raised A$1.3bn in 5-year money in the US at 125bps over US Treasuries, which is 20bps more expensive than NAB’s similar transaction in January (A$1.4bn at 105bps over US Treasuries).

If wholesale funding costs remain where they are, this is likely to be a headwind for the banks as they work their way through bank margins. Should short and long term funding costs not improve we wouldn’t rule out further asset repricing.

The bells…the bells…do I hear dividend cuts coming?