From Brian Johnson at CLSA, the best in the business:

BJ notes that having significantly underperformed since the peak in April 2015 the Australian banks have rallied hard in late February/early March 2016 with the rally likely reflecting a prior degree of “over-shorting” and easier global credit conditions. That said, Australian bank funding costs, both wholesale and retail deposit rates seem to be still rising, Australian banks are over-earning (loan loss writebacks, treasury and tax) and he continues to think the banks are undercapitalised – which sees the structural risks to the existing high ~70% dividend payout ratios in which case ~+10% mid-cycle EPS declines would translate to ~15% to ~28% declines in DPS as sustainable dividend payout ratios decline. While the derating of Australian banks has tempered the pre-existing degree of over-valuation BJ would recommend selling into this macro factor driven sectoral rebound but look to participate in expected recapitalisations in late CY16/early CY17. In particular he would recommend selling ANZ: too many international shareholders, too much financial markets earnings, too much NZ dairy, not enough collective provisioning, too much resources exposure – both on and off balance sheet, too much capitalised software, not enough investment in replatformed core IT systems, and much Asian exposure.

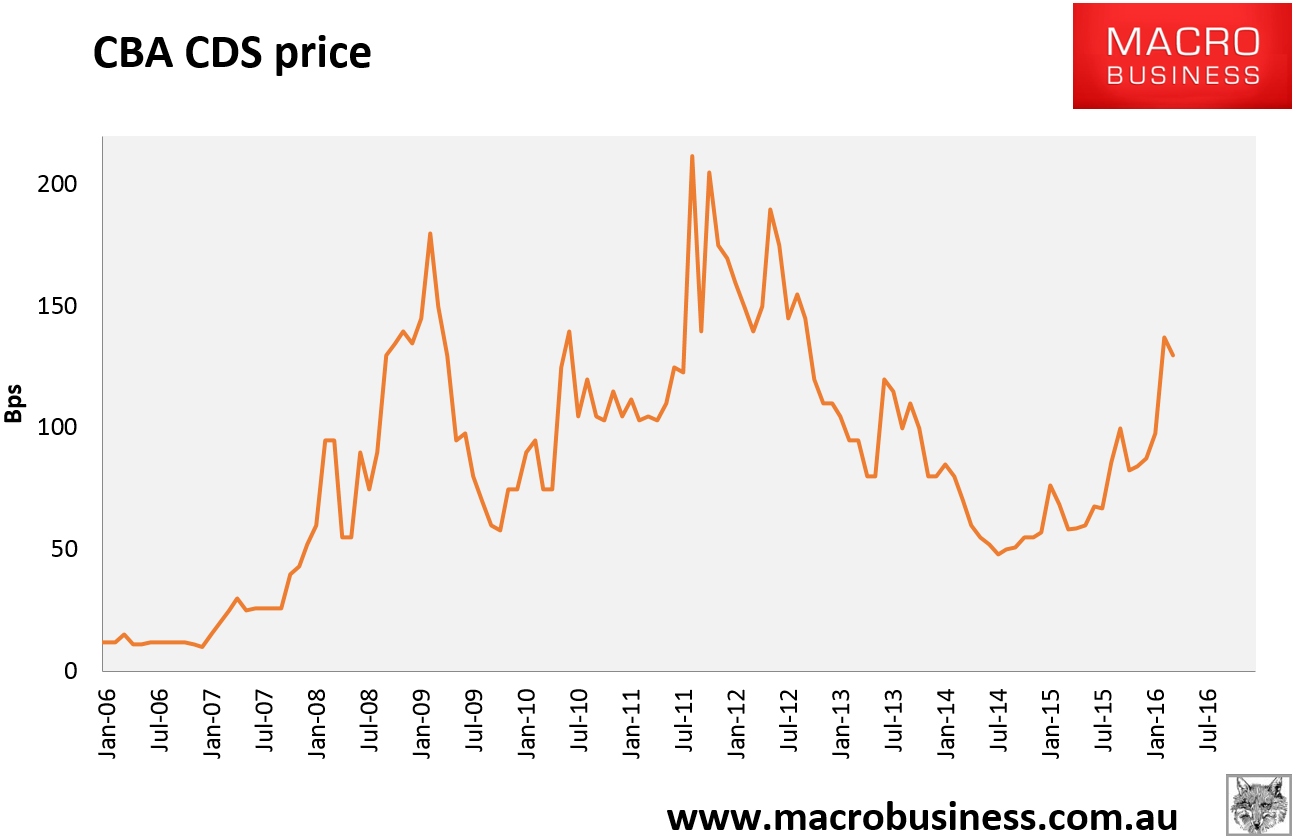

He is also negative on CBA, where the CDS price was unchanged overnight at 130bps: