The Minerals Council of Australia (MCA) has backed a cut in the company tax rate to 20% arguing that it would benefit workers and consumers, as well as businesses. From The AFR:

…the Minerals Council of Australia sought to make the case for lower company taxes with the release of a study by Canadian public policy academic and expert in international corporate tax regimes, Dr Jack Mintz.

Dr Mintz’s study, commissioned by the MCA, argues the beneficiaries of a corporate tax cut are more widespread than just business and he recommends Australia lowers its corporate tax rate to 25 per cent in the short term and considers an eventual reduction to 20 per cent, in line with the United Kingdom.

Dr Mintz says Australia’s 30 per cent rate is uncompetitive, having gone from the 14th highest rate in the OECD in 2005 to the sixth highest rate in 2015. Over the same period, the OECD average has fallen from 28.5 per cent to 25.3 per cent…

It concludes that at least two-thirds of the company tax burden is passed on as higher prices, lower wages and lay-offs.

However, the MCA’s commissioned study has been rubbished by progressive think tank The Australia Institute (TAI), which has released a report of its own arguing that “international and Australian data on tax rates and macroeconomic indicators provides no support to corporate Australia’s ‘instinctive’ claims that lower company tax rates bring wider economic benefits”:

The report analyses data from Australia and OECD countries and finds no support for claims that reduced company tax leads to improved economic performance. Specifically it shows that:

There is no correlation between corporate tax rates and economic growth in OECD countries.

Countries with lower company tax rates have lower standards of living, measured as purchasing power of GDP per capita.

“Claims are often made that uncompetitive rates of corporate and individual income tax are a recipe for lower economic growth and lower incomes, but these claims rely on assertions, rather than data and analysis,” Ben Oquist, Executive Director of The Australia Institute, said.

“The economic case for company tax cuts is weak, and furthermore, it is obvious that many companies are involved in widespread tax avoidance and the federal budget has a revenue problem. It is simply not the time for tax cuts.”

The report also reviewed the claim that corporate tax cuts will lead to higher wages, more jobs and more foreign investment. Australia’s historical data shows:

Wages and mixed income has declined as a share of GDP as corporate taxes have been lowered.

Average unemployment rates have risen as company tax rates have lowered.

Growth in foreign investment as a share of GDP was strongest when Australia’s company taxes were highest.

Polling conducted in blue-ribbon Coalition seats of New England, Dickson and Page revealed more support for an increase than a cut to the company tax rate – while the majority of respondents said it should stay the same.

“There is very low public support for cutting the company tax rate, and this new research shows that voters are right to be sceptical about claims that cuts will trickle-down into tangible benefits for the wider economy,” Mr Oquist said…

Advertisement

The TAI report produces several international comparisons to support its contention. These include:

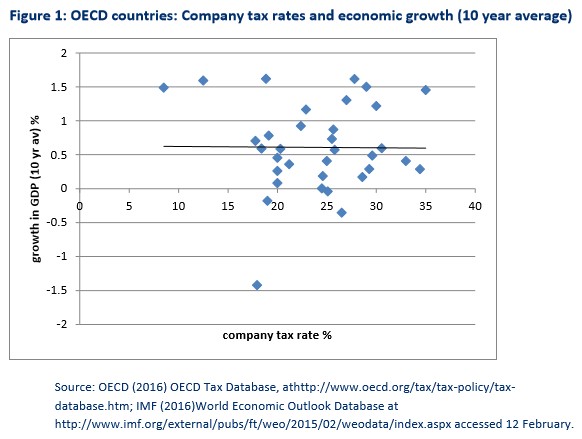

Figure 1 compares average annual real economic growth with average company tax rates over the past 10 years. Each point on the graph represents one of the OECD countries. We see that despite the variation in corporate tax rates, from less than 10% (in Switzerland) to 35% (in the US at the Federal level); the trend line is flat. This data gives no support to the claim that lowering company taxes increases economic growth.

And:

Advertisement

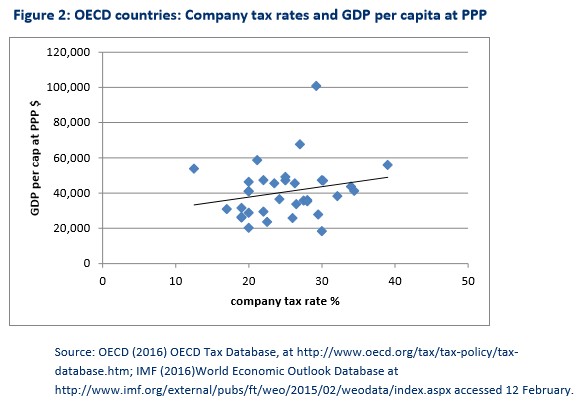

Figure 2 shows that the relationship between company tax rates and living standards is positive – the higher the corporate tax rate, the higher the standard of living. If the proponents of company tax cuts were correct, then we would expect to see countries with lower company tax rates experiencing higher living standards – the trend in Figure 2 should be downward.

The TAI also presents Australian data arguing against a cut to the corporate tax rate:

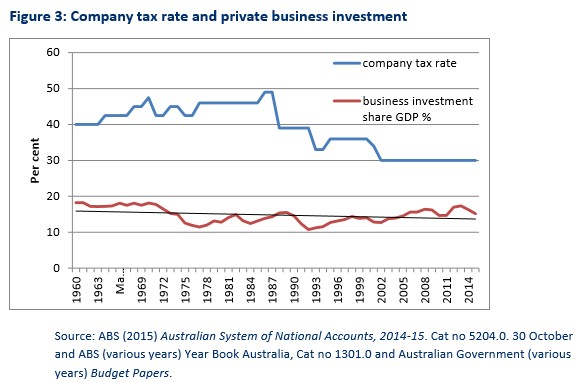

Figure 3 shows that company tax rates increased between the 1960s and 1988 and then gradually fell to the present rate of 30 per cent. Proponents insist that investment will increase with a cut in the corporate tax rate. Yet the other series in Figure 3 shows that, despite the lower tax rate, business investment as a share of GDP has fallen over the period. Business investment accounted for a higher share of GDP in the decade beginning 1959-60 than it has been ever since the trend line clearly slopes downward from 1960 to 1988 when company tax rates peaked. This is inconsistent with the ‘taxcuts-are-good’ thesis…

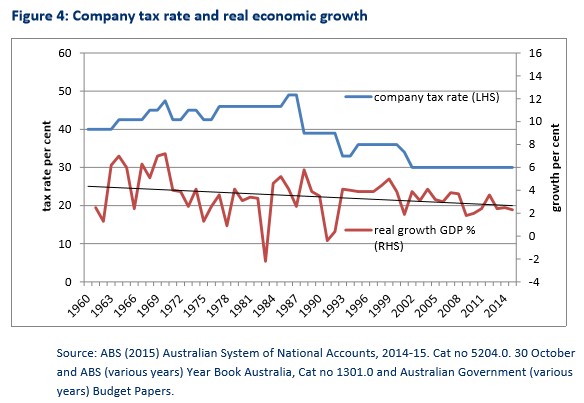

Figure 4‘s message is not immediately clear. However, the trend line suggests that growth has declined over the period summarised in the graph. Our analysis of this data shows that economic growth averaged 3.8 per cent in the period to 1988 when corporate tax rates were relatively high, but fell to just 3.0 per cent in the period from 2001-02 when they were significantly lower. Economic growth was almost a full percent higher when company tax rates were 10 per cent higher…

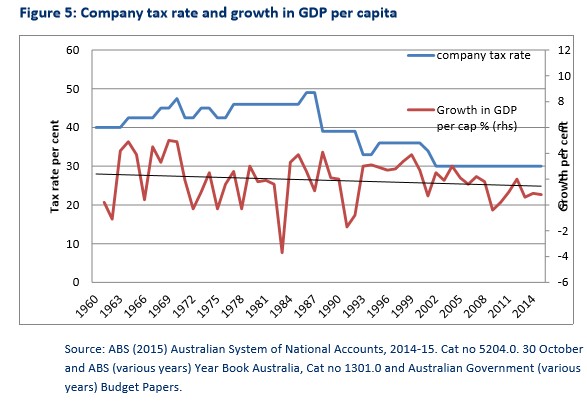

Figure 5 again shows erratic growth in GDP per capita, and appears to suggest a slightly downward trend. This of course is inconsistent with the proposition that lower company tax rates produce higher living standards. GDP per capital/living standard has/have gradually slowed as the company tax rate has fallen…

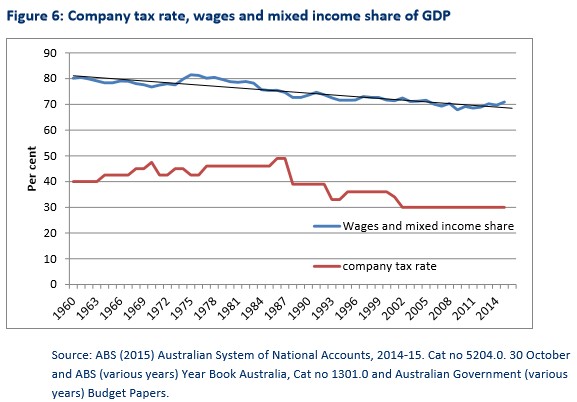

Figure 6 shows that, despite the steady reduction in company tax rates over the period since the 1980s, wages share of GDP has steadily fallen -, by approximately 13 per cent. That evidence suggests the opposite of the thesis that it is workers who would benefit from the reduction in the corporate tax rate. Indeed one might wonder why the business sector would be so concerned about reducing company tax rates if it is workers that would primarily benefit…

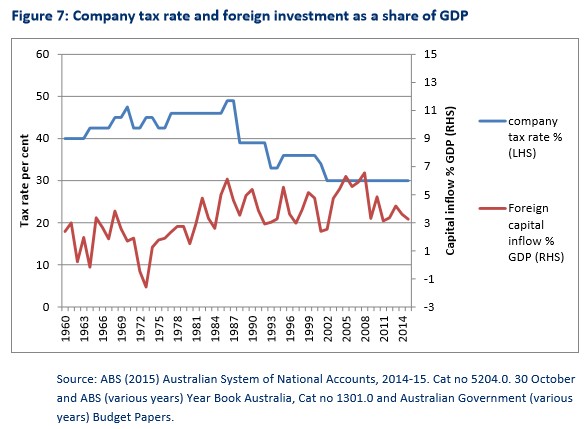

Another regular argument of the ‘tax-cuts-are-good’ thesis is that foreign investment will increase. That claim can be tested by examining the record of foreign capital inflow as has been done in Figure 7.

The results presented in Figure 7 appear to show that foreign investment increased as a share of GDP in the period to the late 1980s when company tax rates were relatively high. After that, the level of foreign investment remains steady, even as the company tax rate was gradually reduced. This is despite the mining boom, which should have increased the level of foreign investment.

In a nutshell, I only support cutting company taxes if it is part of a broader reform program that shifts the entire tax base away from productive effort (both workers and companies) onto more efficient sources, such as land and resources, along with the closure of generous taxation concessions that favour the old and the asset rich.

Cutting company taxes in isolation would be a retrograde move, in my opinion, as it would further shift the tax burden onto workers at a time when the population is aging, the share of workers in the economy is shrinking, and other tax bases are in structural decline.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.