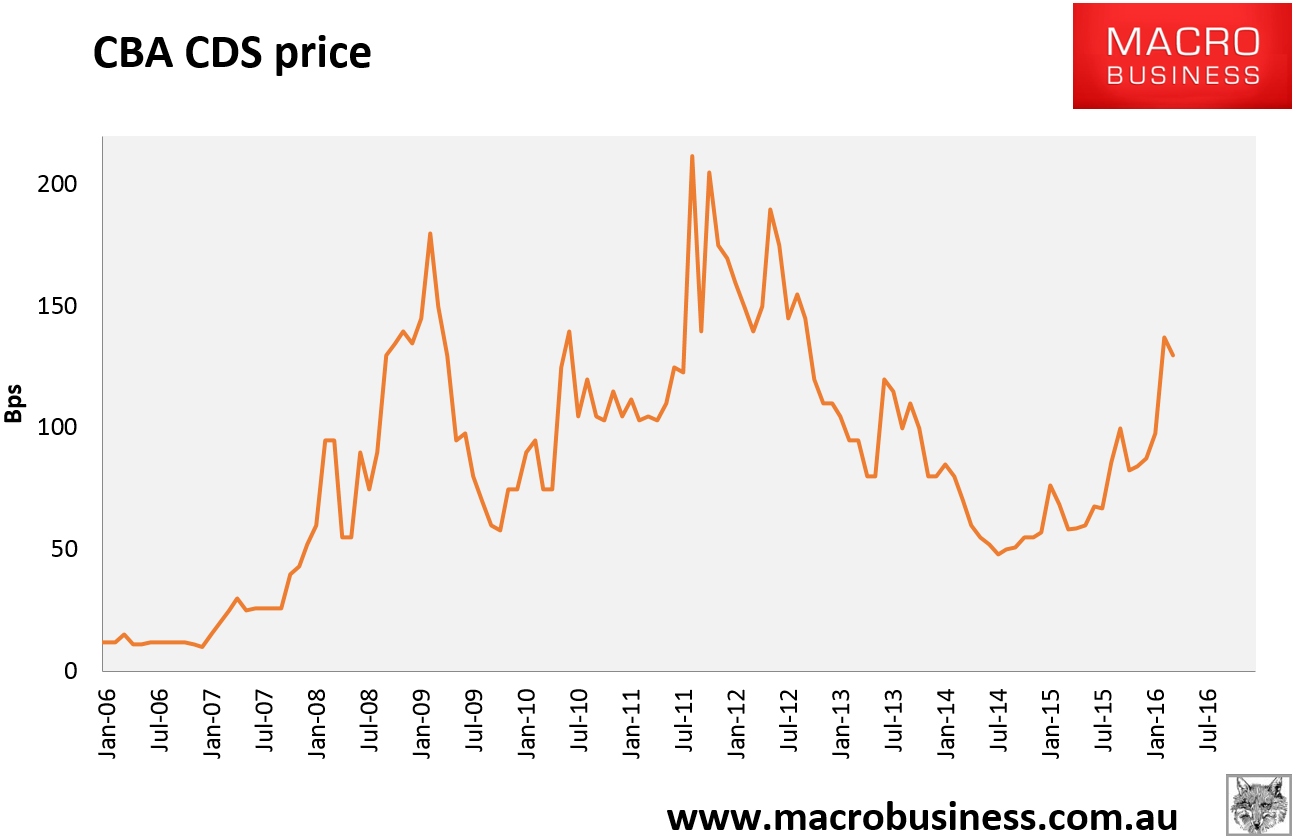

Amid the now wild bear market rally in everything commodities, one price is proving to be surprisingly resilient to the downside. It is the CDS spreads for Australia’s major banks with CBA CDS widening on Friday 3% to 130bps:

The major bank CDS price has so far missed out on the entire spread compression transpiring in wider markets and has, in fact, widened since the bear market rally began.

CBA did manage to get away an RMBS on Friday but, as Banking Day reports, it’s not a good look:

Margins in the residential mortgage-backed securities market, which had its first issue of the year last week, have risen sharply from last year’s levels.

Commonwealth Bank raised A$1.6 billion with an issue of mortgage-backed securities, paying 140 basis points over the one-month bank bill swap rate on the senior notes. Pricing on the B and C notes was not disclosed.

CBA’s last RMBS issue was in September last year, when it raised $2 billion and paid 90 bps over one-month BBSW on the senior notes.

And in February last year it raised $2 billion through an RMBS issue, paying 80 bps on the senior notes.

In both of last year’s issues the senior notes had a weighted average life of 2.8 years, compared with 3.5 years in the latest issue. However, a longer term would not account for much, if any, of the higher margin.

Small lenders will have to pay a premium above CBA’s margin to get their RMBS issues away. This is likely to put pressure on mortgage rates.

Oh yes.