Given the unprecedented shift towards Negative Interest Rate Policy (NIRP) around the world, it is time we ask the question what will this do our assumptions about the Australian dollar? The spread between interest rates in different nations is one key determining factor for forex value though certainly not the only one. Regular readers will recall that MB has a “five drivers” model for the currency:

- interest rate differentials;

- global and Australian growth (more recently this has become more nuanced for the Aussie to be more about Chinese growth best captured in the terms of trade);

- investor sentiment and technicals; and

- the US dollar.

To determine whether the first is set to become a dominant force let’s make some comparisons to jurisdictions that are already running NIRP. The first is Japan where the evidence is promising that NIRP may, in fact, help the Aussie to fall. Since it has installed NIRP, Japan has seen the precise opposite of its intended effects, that is share markets have fallen and the currency has risen:

The first arrow is the election of Abe and the beginning of QE. The second arrow is the arrival of NIRP.

While the present “risk off” environment is forcing some yen repatriation which may be confusing things a little, Japanese NIRP appears in no small measure to have exacerbated the shift. This appears to be the result of banks being hit hard by NIRP owing to its unknown affects on their net interest margins, that is:

- will they cut deposit rates below zero, hitting consumption, or

- will they raise interest rates (the opposite of the intended impact), and

- how much attrition will their be with punters pulling money from the bank?

It’s no wonder bank shares are being pounded!

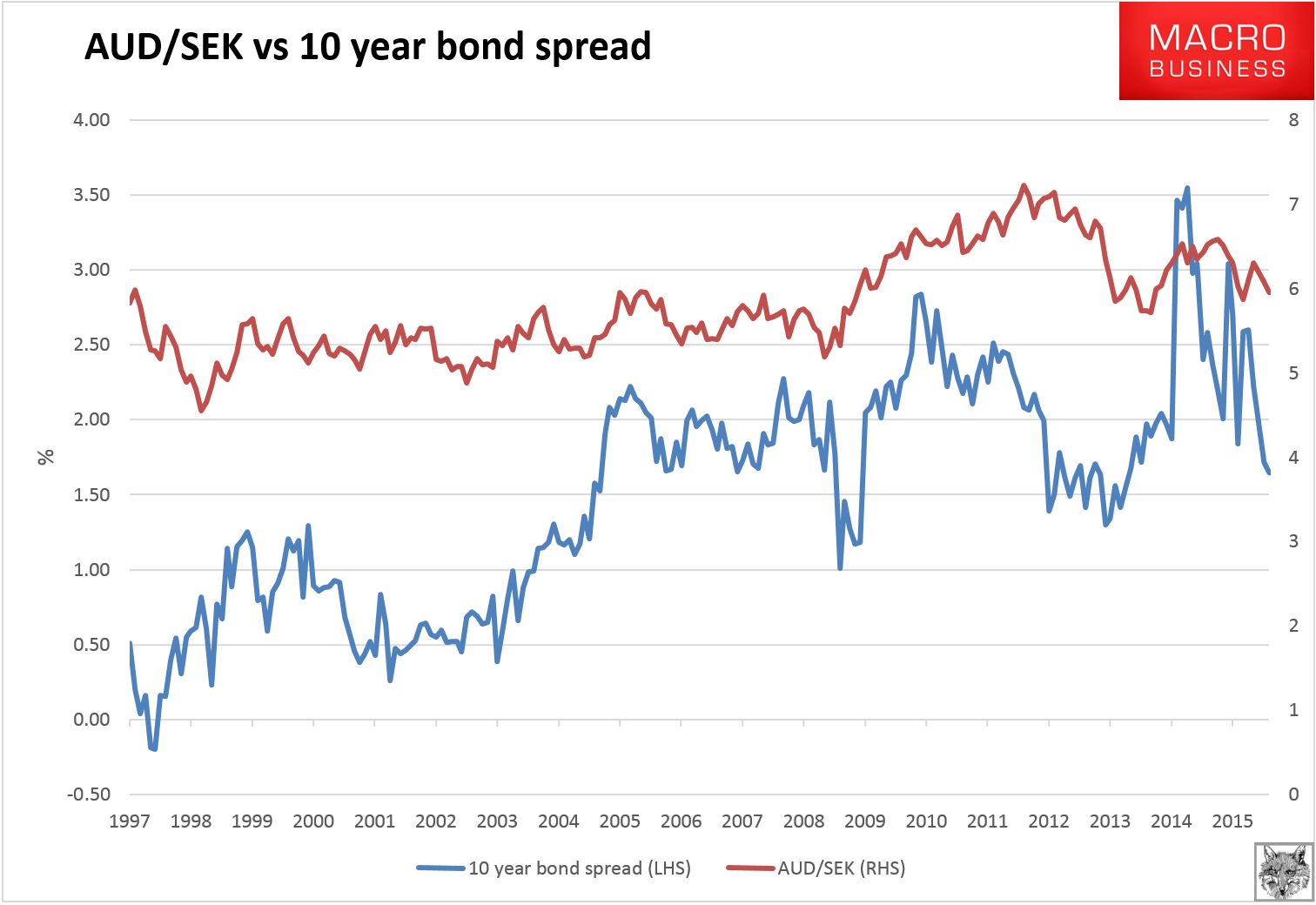

Back to our forex discussion, another country that has used NIRP for longer than Japan is Sweden and there the evidence is less encouraging for the Australian dollar though not decisively so:

When Sweden cut interest rates below zero it’s bond market yields collapsed and the spread to Australian yields soared. AUD/SEK followed suit though not so extremely as bond yields. As well, after yesterday’s even deeper cut into NIRP by the Riksbank we haven’t seen much reaction in the spread at all.

This is the key point, I think, it is still the spread that matters not the NIRP, which seems to lose its impact over time (all shock and no awe). And with Australian interest rates still with a lot more downside ahead than other jurisdictions, the evidence suggests that despite the uncertainties we should still see the Aussie falling as growth, the terms of trade, sentiment and technicals turn against us.