Will negative gearing reform “smash” house prices, economy?

Will negative gearing reform smash house prices and the economy as Prime Minister Turnbott says it will? Let’s look to the evidence.

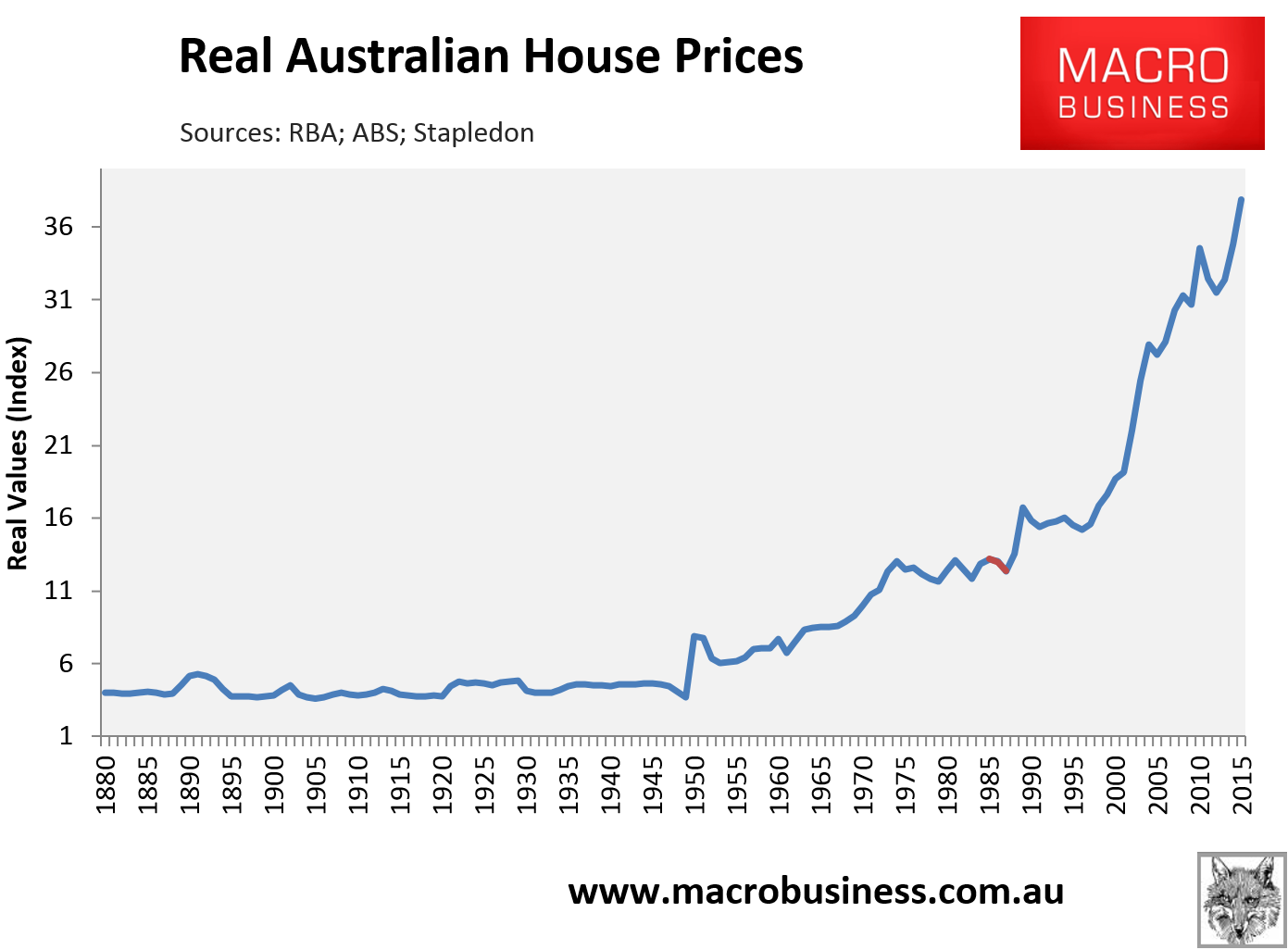

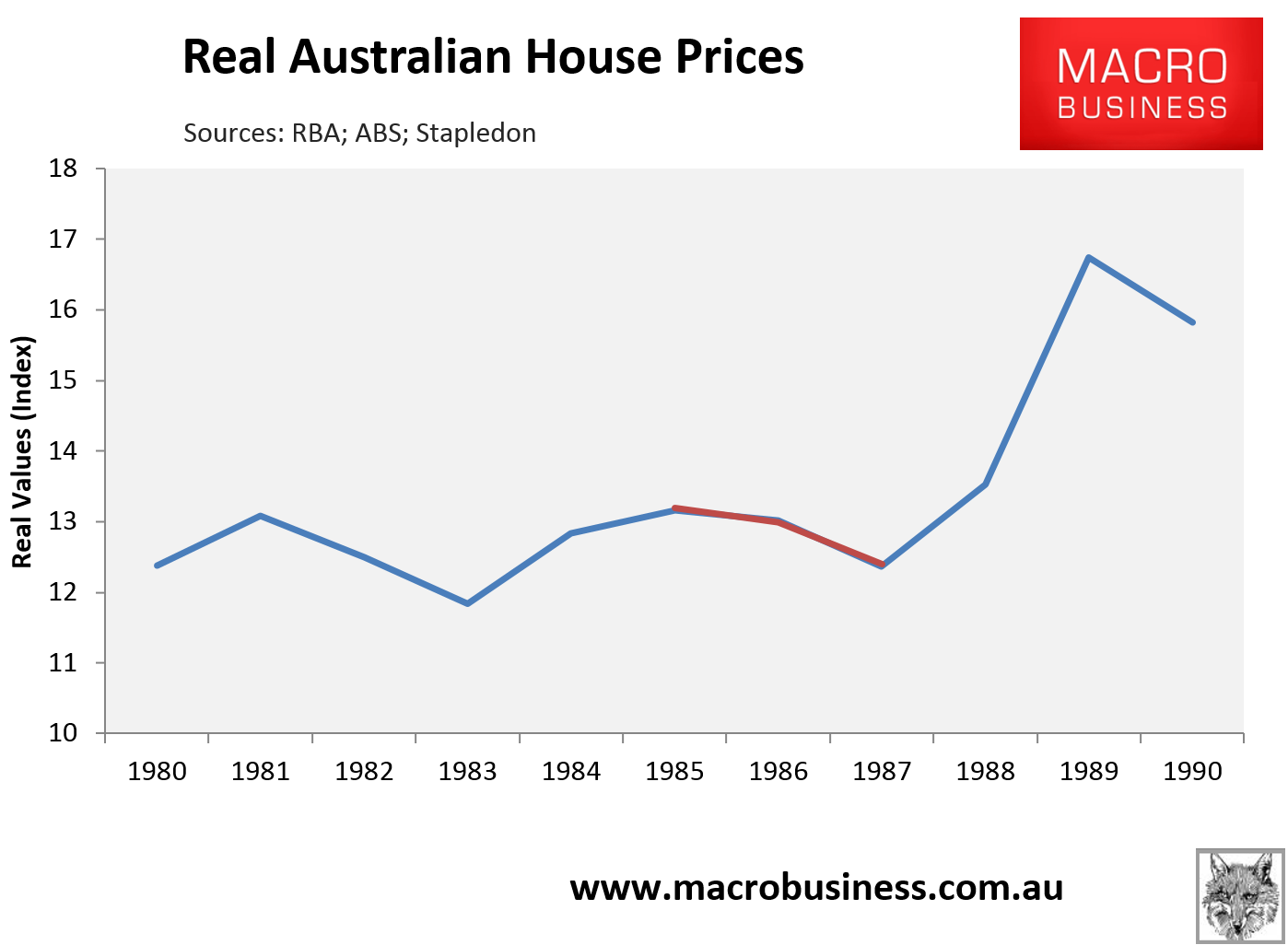

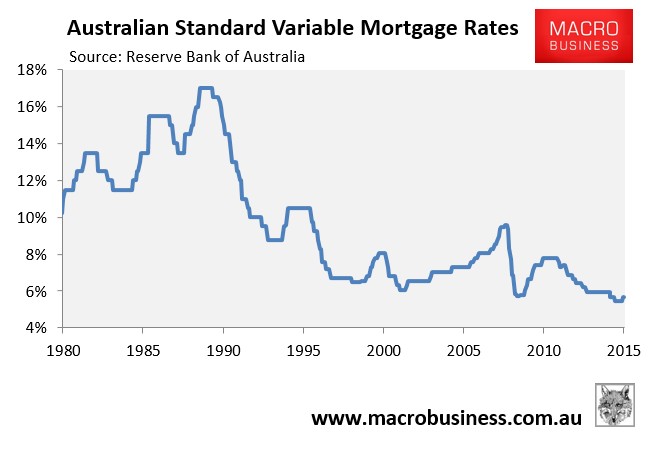

In the mid-1980s negative gearing was repealed for two years from June ’85 to Sep ’87, I’ve marked this period on the chart:

Prices did fall, yes, but you could hardly call it a crash. The correction was 6% over two years for real prices. Given how high inflation was at the time that means nominal prices kept rising.

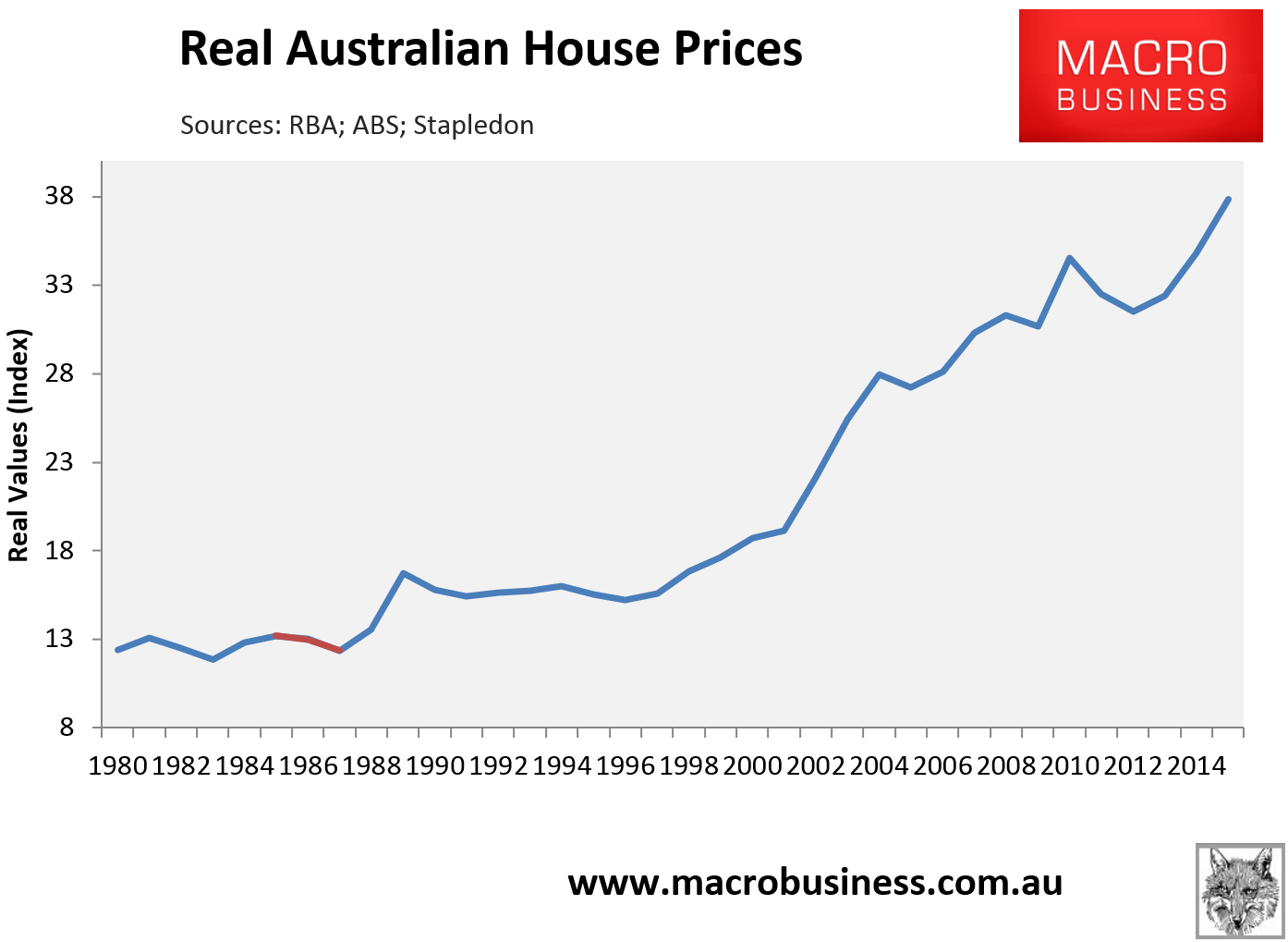

Here’s the same chart over the past four decades:

And just the 1980s:

One can clearly see that the removal of negative gearing is virtually indistinguishable from other trends though prices certainly took off again for a period when it was re-installed, which is really the kind of thing that NG reform is designed to prevent.

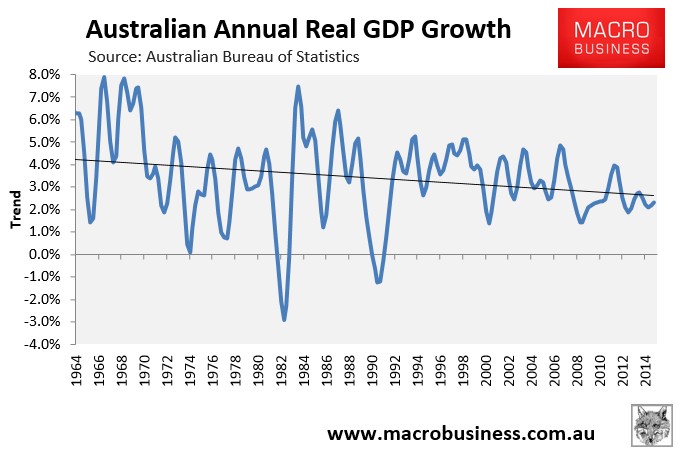

What about the broader economy of the day? Was that impacted? GDP was weak:

Unemployment was materially higher than today at 8% for much of the period as well.

There may be evidence to suggest the NG repeal delivered a short term shock to building approvals:

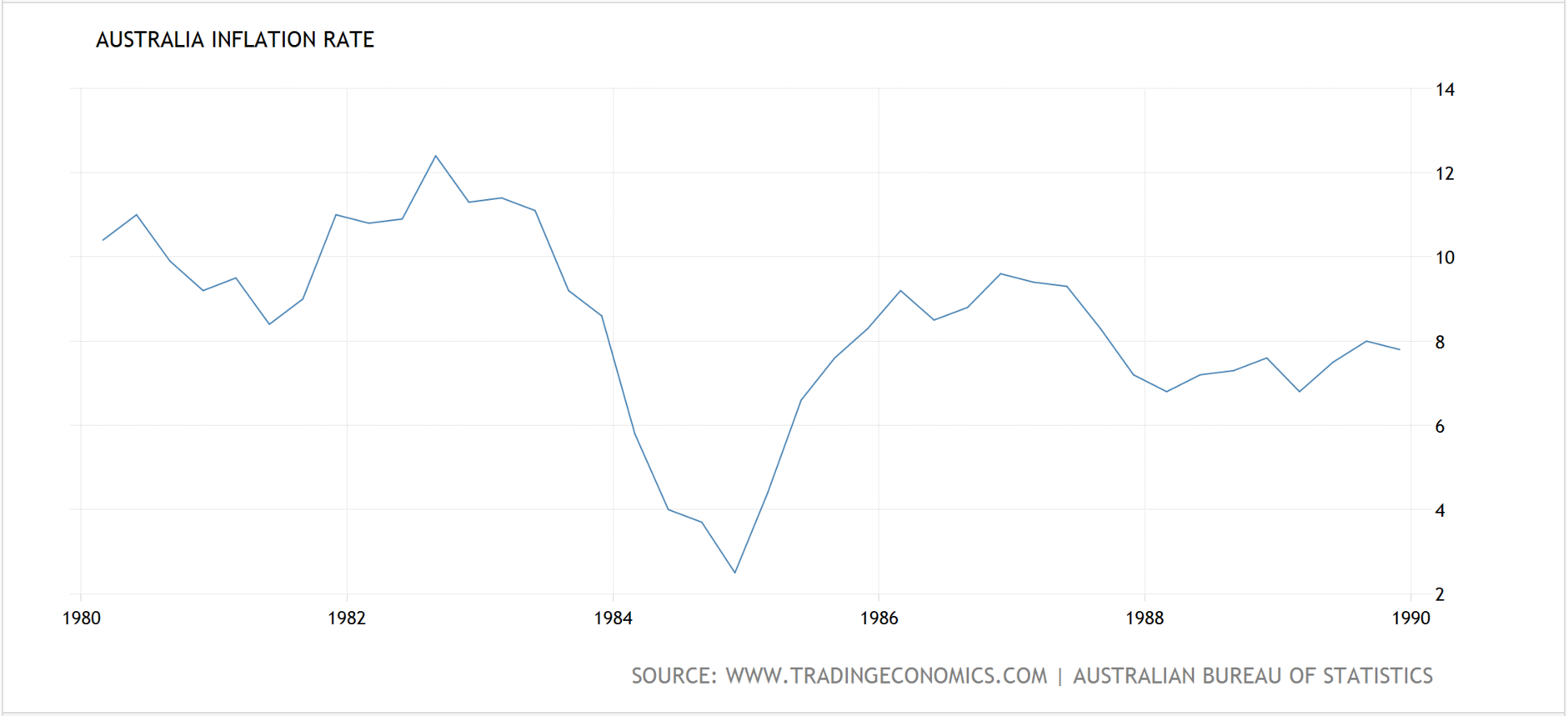

But, if we look deeper we find the the cause was much more likely to have been that it was raining rate hikes through early 1985:

To rein in rampant inflation:

Indeed, the 1987 Cabinet Submission to reinstate negative gearing explicitly acknowledged this factor:

“…throughout the latter half of 1985 and the first half of 1986, construction in the housing sector declined generally, following strong investment over the previous 18 months.

In addition to the negative gearing restrictions, investment in the residential property market over the past two years may have been heavily influenced by substantial tightening of monetary policy, and investor attention to local and offshore share market investments which have enjoyed very strong capital growth. It is not possible to estimate the relative importance of each of these factors…”

There was also a large terms of trade shock of -20% underway over the same period.

In short, stagflation was the economic context and very likely the cause of the slowing in the economy, building approvals and probably weak house prices as well.

On this evidence, we can’t say that the removal of negative gearing had much of an impact beyond (at worst) a marginal exacerbation of existing trends. Certainly one would be hard pressed to extrapolate Turnbott’s wildest claims from the 1980s experience.

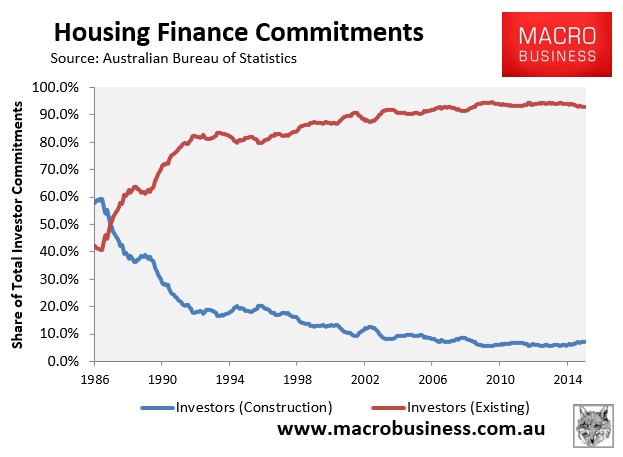

So what lessons does that leave us with for today? The main difference between negative gearing in 1985 and today is that the proportion of NG borrowing going into existing property is much higher now than it was in 1985:

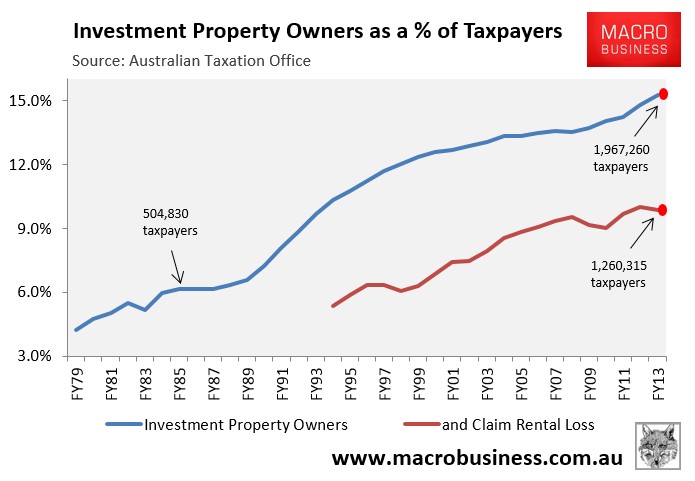

And the proportion of property investors is also much higher today:

So, it is fair to say that the price impacts would be greater. But we also have mitigating factors today:

- a better labour market:

- falling interest rates and low inflation;

- the structure of the economy is much more services oriented, more open and flexible, and

- a falling dollar that would get pushed lower much faster.

Negative gearing reform would interact with all of these variables so focusing on just house price impacts is classic “partial analysis”. To really gauge the usefulness of it we need to assess them all.

There are two ways to sum the variables to make that assessment. The first is using the conventional view of the economy that it is healthily rebalancing post-mining boom towards services demand. The RBA has been at pains to point out that increases in household equity have largely gone unspent through the previous house price boom given that it has not been cashed out as “equity mate”. So what house price impacts there are are likely to be contained. NG reform would stall house prices and probably trigger small falls but those would be offset economically by the benefits of a stronger for longer construction cycle (it is currently heading into a steep peak), as well as lower interest rates and falling dollar stimulating much more broad and swift growth in tradable sectors. Indeed, the reform would release the RBA from its current bind of having to set interest rates to manage the housing bubble instead of the economy.

The second way to view the implementation of the reform is through the MB outlook which sees things as less benign. We already see falling house prices and a high recession risk in 2017, so Labor’s negative gearing reform would certainly exacerbate the trend, though not take prices any more deep given we see Australia running out of tools to support house price growth anyway. Thus in the MB worldview NG reform is more likely to be a part of an adjustment that shifts economic growth more suddenly from housing and consumption to productivity and tradables. The timing may not be ideal but that’s the way Australian politics works and a desperately needed reform thirty years in the making is worth a few extra months of economic pain.

This is the key. There is no way to execute structural reform without pain. NG reform is a structural change that boosts the economy enormously over time as it shifts the allocation of capital away from unproductive uses like house price speculation towards more productive uses, thereby sustainably boosting prosperity for the long term for the entire economy.

That comes with a dividend of meritocracy that should be the goal of any prime minister working in the national interest.