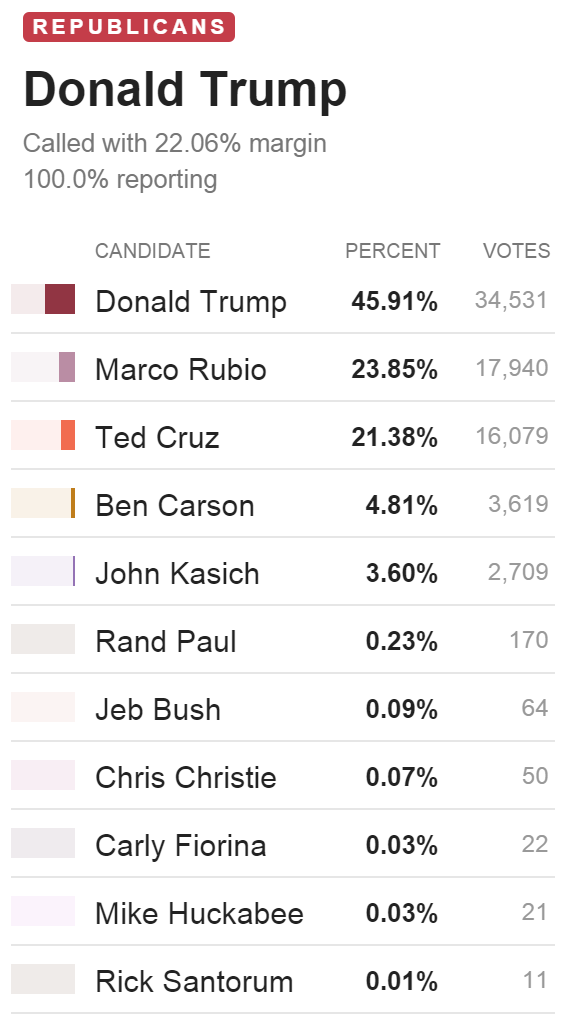

Donald Trump didn’t just win the Nevada primary, he destroyed it:

Good to see Rick Santorum where he belongs. Angus Nicholson from IG has more:

What will the US elections mean for markets?

While the US elections have been getting a lot of media attention, they have not as yet begun to have a major impact on the markets. This could be set to change over the next few weeks as over half the Democratic and Republican primaries are wound up and it becomes clearer who the eventual nominees will be. The possible outcomes of the primaries in the first half of March could have quite a bearing on the US dollar and equity markets, likely with a general downward bias. The need for vote-winning policies could also herald a particularly harsh focus on the financials and healthcare sectors.

At the current juncture

The Democratic race is largely a question as to whether Hilary Clinton can fend off the surge seen in Bernie Sanders’ popularity. Two recent developments indicate that Clinton is likely to consolidate her lead from here on out. One is the death of Supreme Court justice Antonin Scalia now guarantees at least one Supreme Court appointment for whoever is elected president. This could significantly change the balance of power in the Supreme Court if the Democrats were able to replace Scalia with a more liberal justice. This development is likely to rally more support towards Clinton as she is seen as more electable in a general election and hence more likely to appoint someone successfully to the Supreme Court. Clinton also won decisively over Sanders in Nevada on Sunday. While she only won 52.6% to 47.3%, importantly Sanders was not able to eat into her popularity among black voters and only made minor inroads with Latino voters, showing he has not been able to convert his strong popularity among white males into other demographics. Recent polls for Saturday’s South Carolina primary are giving Clinton a 20-point lead, and with a strong performance on 1 March’s “Super Tuesday” where eleven states will vote, Clinton may well have largely locked up the nomination by next week.

The Republican nomination is far less certain, but the two most likely candidates are either Donald Trump or Marco Rubio. Historically, Trump’s position at this point in the race has usually indicated the successful nominee. Trump has won both New Hampshire and South Carolina, and no Republican has ever won both those primaries and failed to win the nomination. The big question is whether the Republican Party establishment can rally behind Marco Rubio now that Jeb Bush has dropped out of the race and eat into Trump’s popularity.

This scenario that many in the Party establishment are hoping for largely depends on Ted Cruz’s (who has consistently placed behind Trump in many of the primaries) supporters all accruing to Marco Rubio on the logic that Cruz’s predominantly evangelical supporters are unlikely to support Trump. However, Trump has increasingly been picking up evangelical support. On 20 February’s South Carolina primary, Trump won 43% of the evangelical vote, a larger share than even Ted Cruz did. There is a very good chance that Trump does a better job of eating into Cruz’s supporters than Rubio does. And a strong performance by Trump on 1 March’s Super Tuesday, particularly in key demographics that Trump has struggled to pick up, could see Trump begin to pull away noticeably from the pack.

The trade?

Given this set up, a Clinton-Trump election does seem the most likely outcome, followed closely by a Clinton-Rubio election.

In a Clinton-Trump scenario, Clinton would have a good chance of successfully reuniting the “Obama coalition” of minorities, the young, and middle-class professionals, particularly given Trump’s anti-immigrant rhetoric. Because the contest would be easier for Clinton, there may be less demand for her to bow to the Sanders-driven demands of the Left and follow through on her on her harsh rhetoric against Wall Street and the healthcare industry. Given this, a Clinton-Trump match up may well be a positive for both the USD and equities. There may be less demand for her to tighten up financial and banking regulations, however, her policies towards healthcare costs may still weigh on the sector.

Clinton-Rubio would be a much tougher fight, with a vicious battle over the Latino vote. In such a scenario, Clinton may well be forced to really rile up the base of the Democratic Party in the way Sanders has done. This would likely lead to policy announcements that would excite the Left, harsher regulations on the banks and the healthcare industry would be the obvious announcements, even if ultimately getting such legislation passed would be quite difficult. These concerns are likely to weigh more on equities than the US dollar, unless the proposed funding commitments could lead to a major blow out in the US fiscal deficit, in which case the US dollar would also be weighed down.