A flood of money out of China in the last six months means that it may be too early to call the top of the property market.

That’s the view of Goldman Sachs chief economist Tim Toohey, who believes policymakers may still be constrained by a build-up of financial stability risks as a result of rising property prices.

“One of the surprises is that we haven’t actually slain the dragon,” Toohey told clients at the investment bank’s annual macroeconomic conference.

“Private sector capital outflows actually accelerated late last year. We’re just not sure what impact it has had on house prices, commercial property and other asset classes, or what happens next.”

Mr Toohey pointed to a decline in employment growth and migration that has been identified by the central bank as an impediment to future growth, but a factor that will turn an undersupply of housing to an oversupply by next year.

…But he is reluctant to forecast a near-term cut in the Reserve Bank cash rate, partly because capital outflows may elevate already high asset prices.

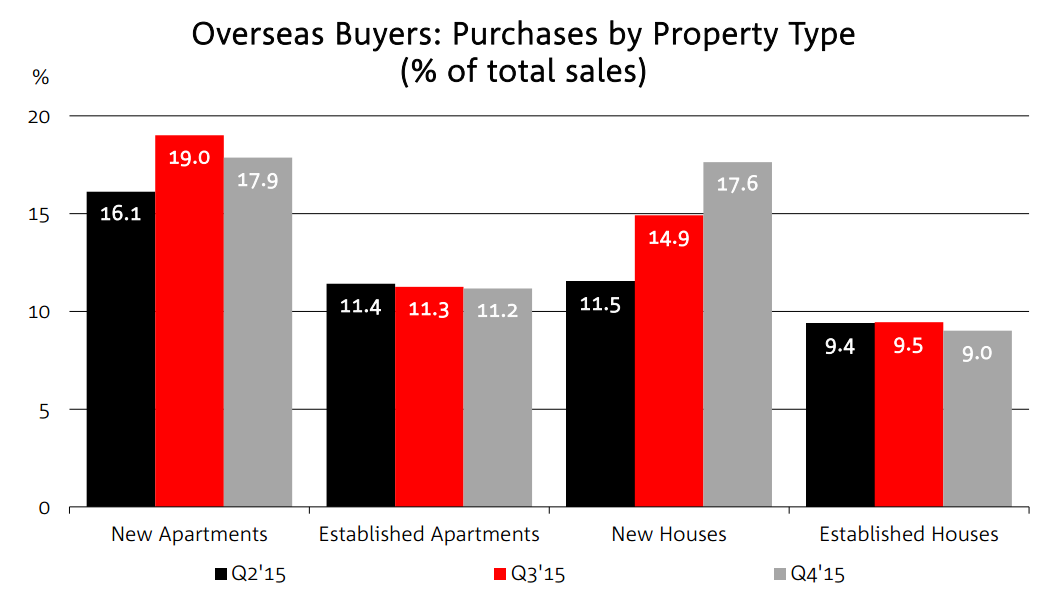

We don’t have any decent data but yesterday’s NAB property industry survey provided hope that Chinese capital controls and our own enforcement measures will work to an as yet unknown extent:

The fall in foreign buyers in Q4 coincided with the accelerated capital flight and China has since added a number of other measures to tighten pipelines. As well, the local restrictions did not come in until December first so we will have to wait a little longer to see how they effect volumes and prices.