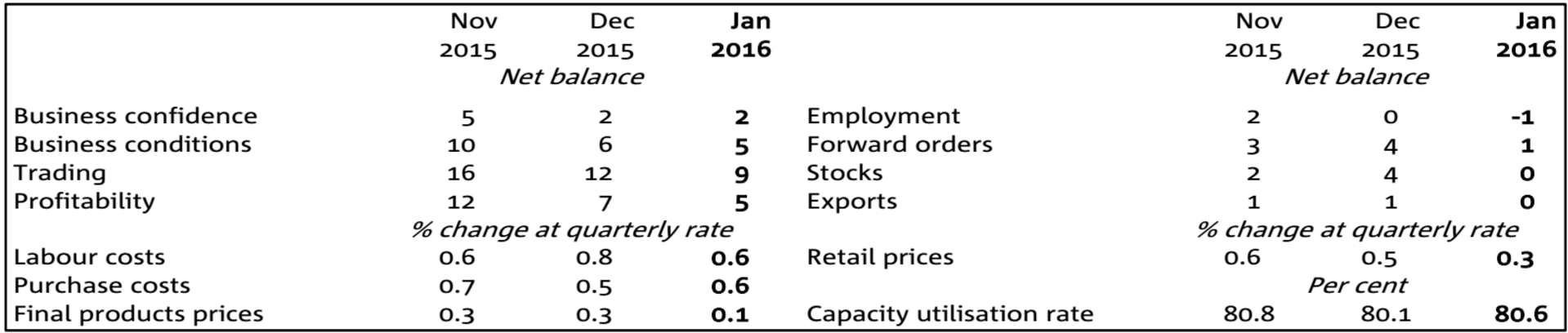

The NAB Business Survey softened slightly in January, although the deterioration was to a large extent driven by a sharp decline in mining and wholesale – conditions were generally mixed elsewhere – and was largely concentrated in Western and South Australia where the flow on effects from the mining slowdown (conditions -47) are clearly spreading. This suggests that fundamental conditions in the non-mining economy remain resilient. Business conditions eased back to +5 points in January (from +6), consistent with the long-run average, with all 3 major components (trade, profit and employment) edging back in the month. Employment conditions were the most disappointing, dropping back into negative territory, which is a continuation of the stark divergence from very strong employment outcomes reported by the ABS. This may also help to explain further deterioration in retail conditions, although the other major service sectors are consistently outperforming.

• Capacity utilisation – a useful measure of the underlying health of the economy – regained a good deal of the lost ground from last month, but remains below long run averages, hindered by a large drop in wholesale. Forward orders weakened in January, and despite remaining positive, suggest a moderation in growth momentum in the near term. Capex was also lower. Business confidence continued to hold up in the face of turmoil in financial markets, despite the effects it appears to be having on sentiment globally. Although confidence is subdued, it held steady in positive territory (+2), likely bolstered by the buoyant business conditions within Australia. Across industries confidence is mixed, although mining is the only industry where the confidence index is negative. Construction firms remain most confident, in keeping with the record pipeline of residential construction.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.