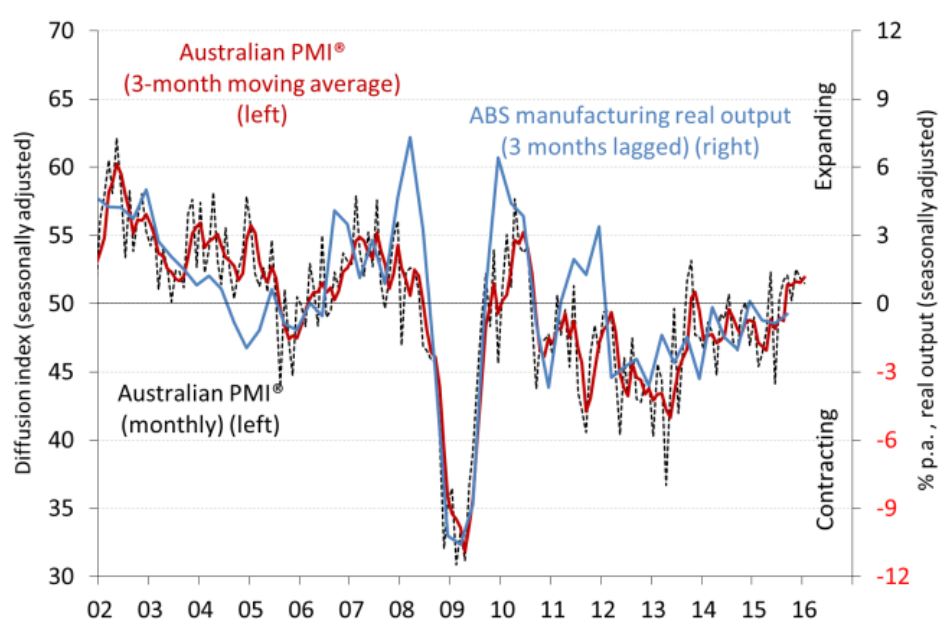

The Australian Industry Group Australian Performance of Manufacturing Index (Australian PMI® ) declined by a marginal 0.4 points to 51.5 points in January, indicating a net expansion across manufacturing (index results above 50 points indicate expansion).

January was the 7 th consecutive month in which the Australian PMI® has been above 50 points (net expansion). This is the longest unbroken run of expansion since 2010. Eight of the past nine months have had an Australian PMI® result above 50 points.

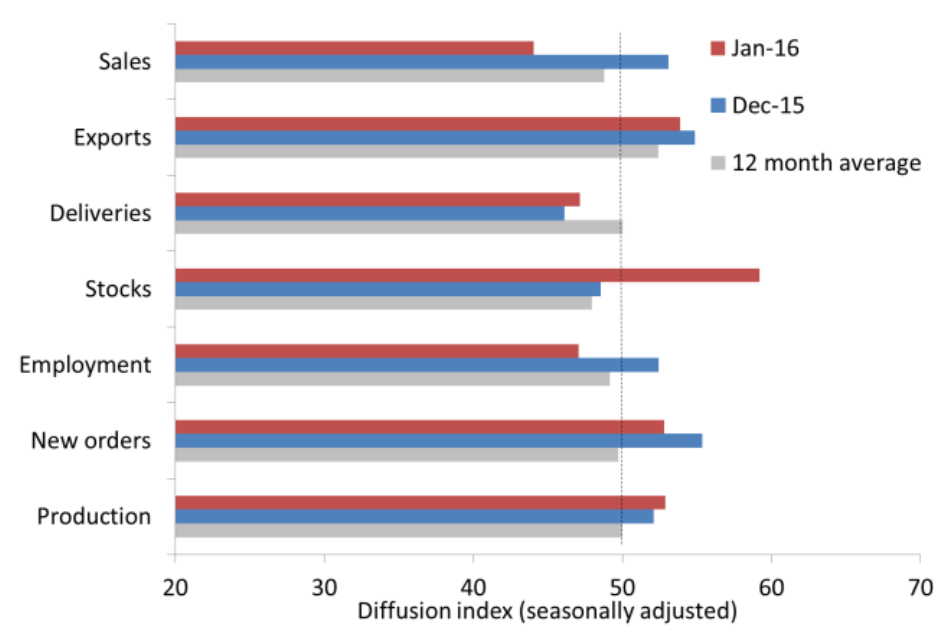

Of the seven activity sub-indexes in January, new orders (52.8 points), exports (53.9 points) and production (52.9 points) remained strongly positive, but employment, supplier deliveries and sales slipped back into contraction. Stocks (inventories) were replenished (59.2 points) after two months of contraction before the summer break.

Four of the eight manufacturing sub-sectors in the Australian PMI® expanded in January (in three month moving averages), down from five sub-sectors in December and November, with non-metallic mineral products (building materials) dropping under 50 points and into contraction. The best expansions continue to be in food & beverages, wood & paper and petroleum & chemicals. Machinery and equipment remains in contraction but is steadily moving towards stabilising, with its best Australian PMI® result since June 2014.

Positive trends identified by manufacturers in January included: the low dollar supporting exports to Asia and the Middle East and better local orders; improved local confidence; and stronger demand for local building materials, food, groceries and healthcare products.

These positive trends were offset by slowing automotive production, mining projects and Government infrastructure projects. Input cost increases are becoming more widespread as drought affects supplies for food and beverages producers. Energy costs are also rising.

The internals don’t look great on the month with sales hit hard and inventories through the roof but of most concern is employment:

Can’t make too much of it on one report. Trends are still solid.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.