Mr Howard said he was not “convinced” that changing the tax breaks for negatively gearing property investments was a good idea…

…Mr Howard said he remembered how the Labor government that restricted negative gearing in 1986 “retreated very quickly, and my recollection is that had quite an impact on rents particularly in Sydney”.

Leaving aside the myth that rents rose after the temporary restriction of negative gearing between 1985 and 1987, which has been thoroughly debunked by MB, we should not be surprised by John Howard’s position against reforming property tax breaks.

It was the Howard Government, after all, that made the fateful decision to halve the rate of capital gains tax (CGT) in 1999, which lead to an explosion of negatively geared investment.

Advertisement

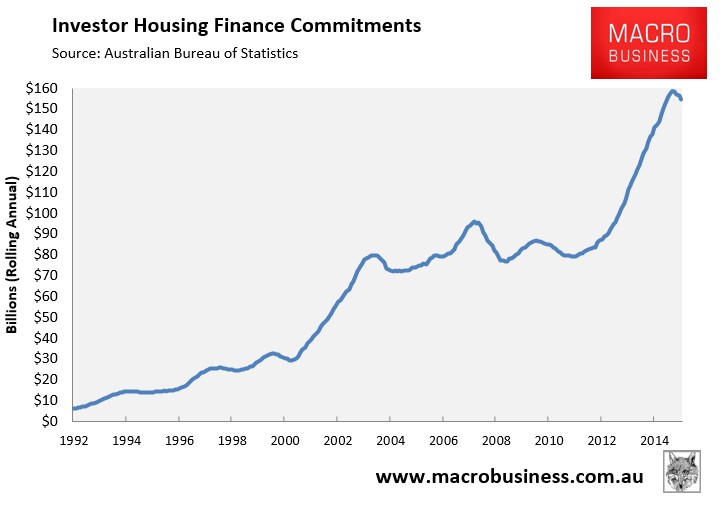

Shortly after CGT was halved, loans to investors surged, growing almost exponentially over subsequent years (see below chart).

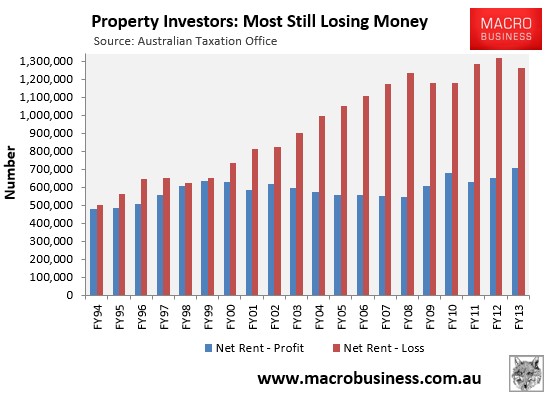

This growth was driven by a massive increase in the number of negatively geared investors, whose numbers have roughly doubled since 1999 at the same time as the number of positively geared investors has remained roughly stable (see next chart).

Advertisement

Indeed, the slashing of CGT made negative gearing a much more effective tax shelter – for reasons explained in the Hawke Government’s 1987 Cabinet Submission to re-instate negative gearing (viewable via searching here):

The negative gearing measure was introduced [in 1985] to partially close-off a generally recognised tax shelter, a rationale which remains broadly valid…

The three basic features of a typical tax shelter are the absence of a full nominal capital gains tax, the deductibility of full nominal interest expenses, and the mis-match in the timing of the deductions and the recognition of taxable income (for example, because capital tax is payable on a realisations rather than accrual basis).

Rental property investment clearly exhibits each of these features, as do some other activities, and so effectively obtains tax benefits under the current tax system.

Advertisement

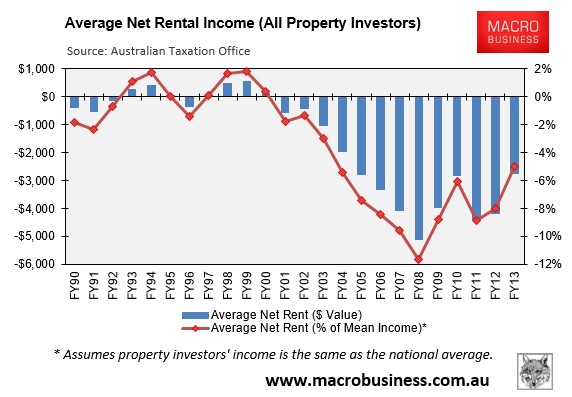

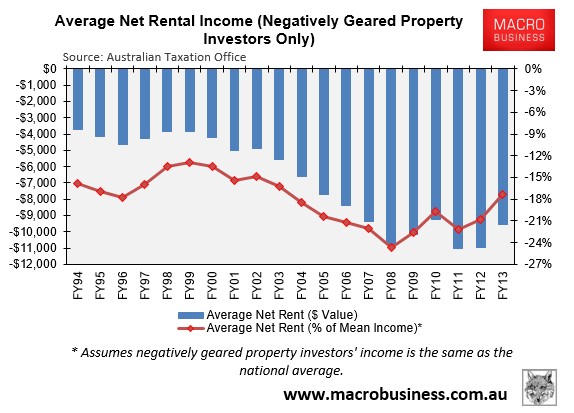

It is also a key reason why the value of rental losses exploded after the CGT discount’s introduction (see below charts).

As noted by Deloitte’s “Mythbusting Tax Reform”report, released in October, Howard’s CGT discount has also had adverse equity and efficiency impacts:

Advertisement

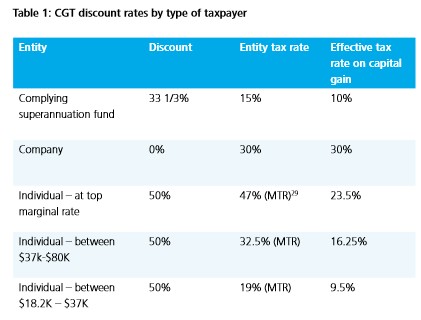

Table 1 shows there are really big incentives for some taxpayers (such as high income earners) to earn capital gains, versus little incentive for others (such as companies)

The discounts Australia adopted back in 1999 assumed inflation would be higher than it has been – and so they’ve been too generous.

By the way, ‘overdoing it’ on the CGT discount doesn’t just come at a cost to taxpayers. It hurts the economy too. As the discount does not target particular sectors or types of assets, it provides stimulus to invest in both productive and unproductive assets…

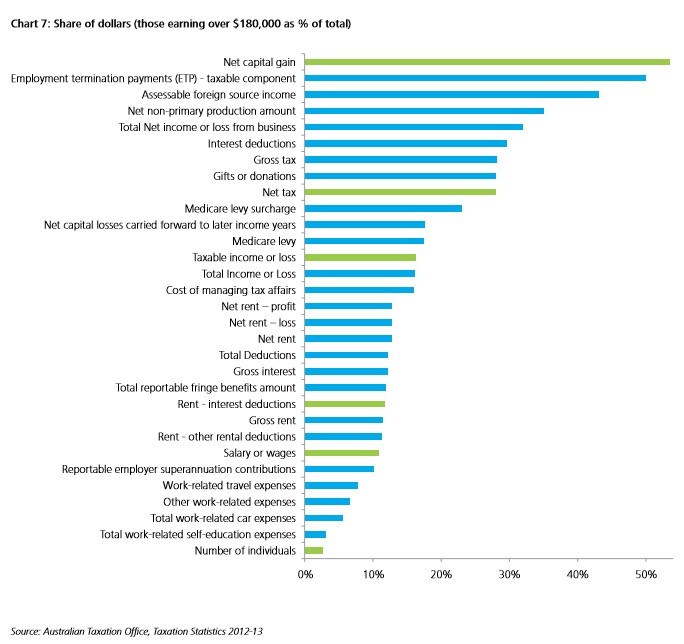

It is also part of the reason why Chart 7 shows that those who earn more than $180,000 a year account for a much bigger share of net capital gains…

Our conclusion? The current CGT discount is too generous, to the extent that it undermines the very principles of this nation’s progressive personal income tax system. It’s time for a change. Reform of the concession is long overdue.

It’s fair to say that John Howard shares some of the blame for Australia’s housing bubble, so we should not be surprised that he continues to defend it.

It was the Howard Government’s halving of CGT that first put a rocket under negatively geared investment which continues to plague the housing market today, to the detriment of first home buyers. It was also his government that allowed self-managed superannuation funds to leverage into property, ramped-up immigration, and implemented a raft of first home buyer subsidies.

Of course there are other important contributing factors, including financial deregulation (reduced bank capital requirements), falling nominal interest rates, foreign investors, and the states’ increasingly restrictive land-use policies. But it was the Howard Government that first kicked this bubble off.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.