Deutsche Bank has a very good take on CBA today (and a Hold rating):

Defensive qualities on show but PE rel vs peers very elevated

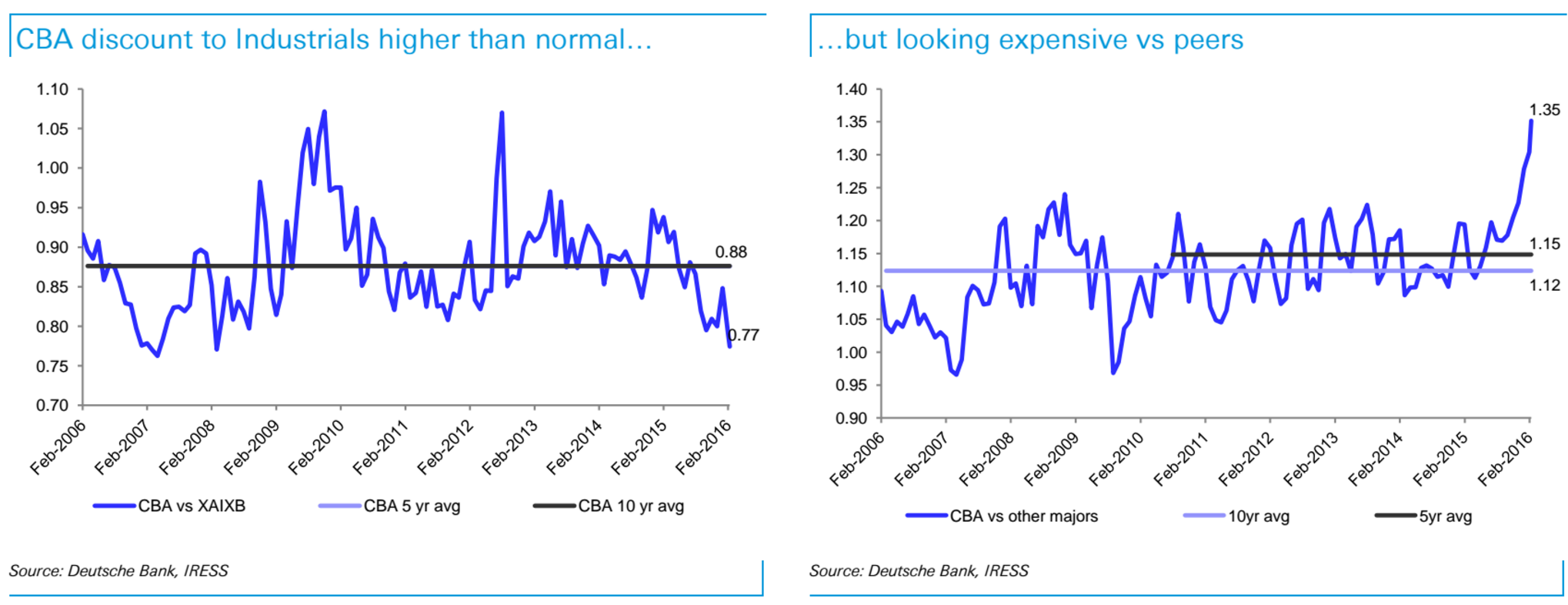

CBA’s 1H16 result was somewhat of a mixed bag. While its net interest margin disappointed due to weakness in Insto & NZ, cost growth was stubbornly high and impairment expense increased, this was offset by better than expected loan growth and non-interest income which delivered a result in line with the market. In the current environment, an in-line result should be seen as a creditable outcome. That said the outlook for both margins and costs does look testing, reflected in our earnings downgrades, and with CBA already trading at a 35% premium to the major bank peers (vs 5yr avg of 15%), we think the market is already fully valuing CBA’s defensive qualities. Retain HOLD.

Margin outlook challenging but growth has made up for this

CBA’s 1H16 margin disappointed (flat hoh vs DBf of +2bps), with mortgage repricing benefits evaporating. This largely reflected ongoing Insto pressures, which are likely to be replicated by other banks (particularly ANZ which is overweight Insto). The retail margin expanded, with repricing benefits largely sticking. While headline NIM looked soft, strength in Aus & NZ lending made up for this. The NIM outlook is fluid at present, however if conditions remain as they are funding pressures are likely to impact margins in the ST. However CBA has flexibility given it is pre-funded on its wholesale funding program, and prolonged funding cost pressure is likely to see further asset repricing.

Higher bad debts but still healthy conditions ex mining/oil & gas

CBA’s impairment expense rose more than we were expecting, but at 17bps of GLA the charge remains near cyclical lows. While impaired assets in the mining/oil & gas book rose from 0.8% to 1.9% of mining/oil & gas exposures, the $350m of impaired assets is small in the scheme of group GLA and conditions outside the mining sector continued to improve for CBA.

That premium is monstrous. CBA has the biggest exposure to WA of any bank, which is ground zero if the bust really gets going.

CBA has a certain protective gloss about because it was once government owned and as such is a little less exposed to wholesale debt because deposit funding is higher. Nonetheless, if Megabank comes under real stress, where one goes all will follow.

Advertisement

It looks like the last redoubt of the yield desperate to me.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.