While Captain Glenn is still plumping for a smooth retirement, recently telling parliament that the banks have no reason to raise interest rates as funding costs rise, Deutsche has more clear-eyed view:

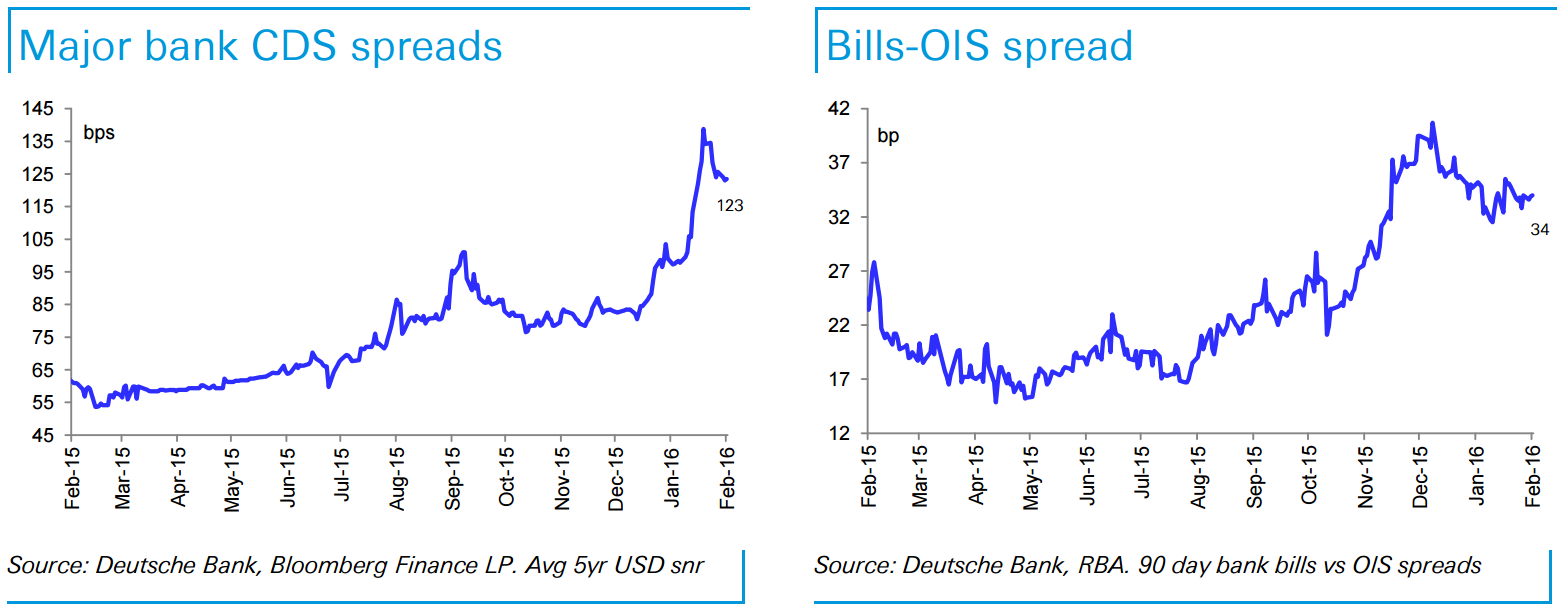

Inside the Bank Vault this week, we take a look at indicators of wholesale funding costs. Over the past month we have seen ongoing deterioration in major bank CDS spreads (26bps wider), while bank bill-OIS spreads have improved a little over the past month (-1bp), albeit off relatively high levels. Meanwhile the AUD/USD cross currency basis swap spread is close to its low point of the last few years. Overall we think wholesale funding costs have gone from being a tailwind for bank margins to a headwind, as evidenced by the recent reporting season. Further asset repricing looks increasingly likely to us.

To date we have been more concerned about rising short term funding costs rather than long term wholesale funding costs, given: i) front book pricing on LT wholesale funding still appeared to be at or below back book spreads on average; and ii) it takes time for increases in LT wholesale funding costs to work its way through the margin. That said recent widening of term funding spreads suggests to us that front book term funding costs are now above the back book. While this will still take time to work its way through bank margins, it does present downside risk to earnings and we think the likelihood of further repricing of housing and business loans is increasing.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.