Bank funding costs launch on Western Sydney mortgage sting

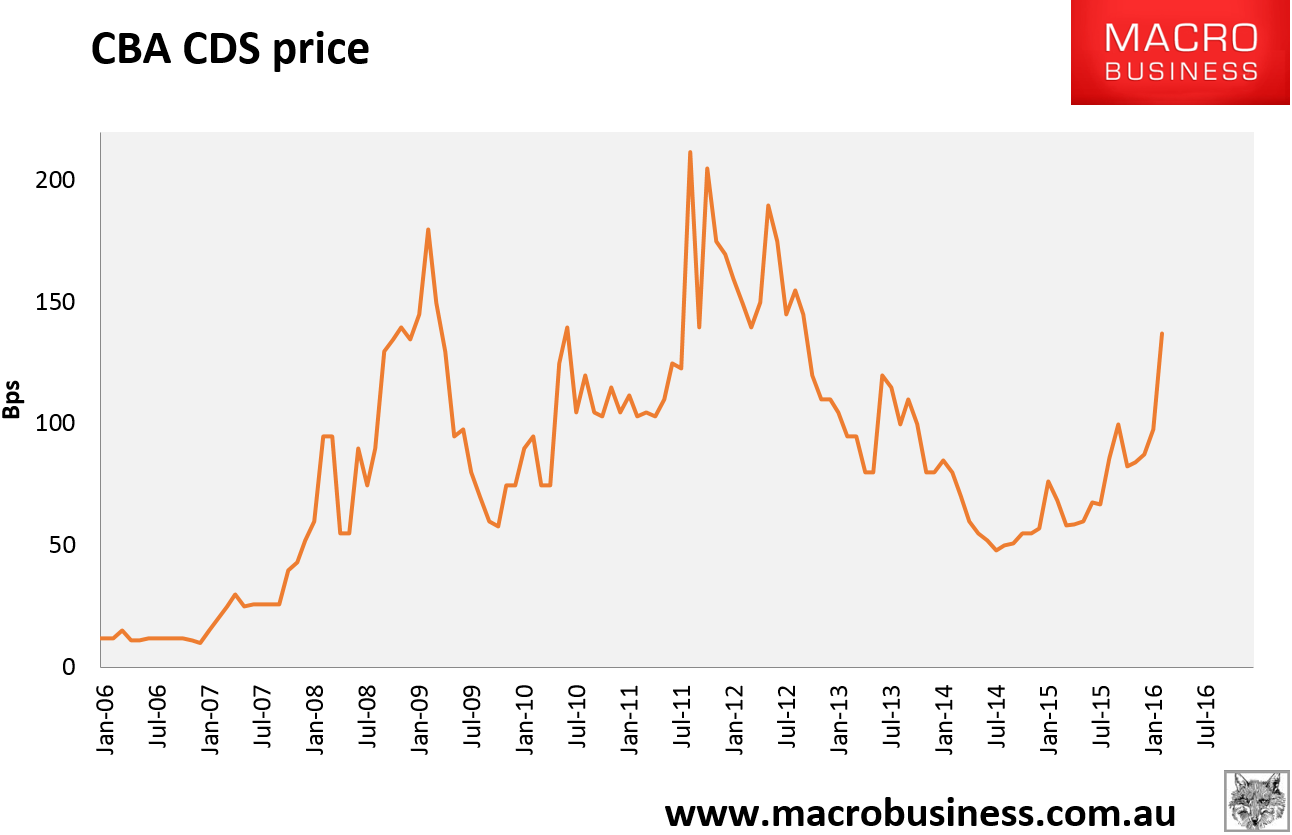

Well…that escalated quickly. CBA CDS prices launched on Friday as markets digested the news of the Jonathon Tepper and John Hempton Western Sydney mortgage sting. Climbing as high 142bps it settled at 137.34bps up 11.4% on the day:

CBA is out this morning with a rebuttal at The Australian:

Chief executives of the big four have been quiet on the 38-page report compiled by British economist Jonathan Tepper and local hedge fund manager John Hempton, who advise clients to take short positions on the Australian dollar, as well as local banking and mortgage insurance stocks.

Mr Narev said the country’s banking system had developed a rigorous approach to extending credit “through decades of practical experience”.

“We have also learned from experience in other parts of the world where this has not been the case to make our practices even stronger,” the CBA chief told The Australian.

“We never assume that any part of our economy is impervious to downturn.

“So even when we don’t believe such a downturn is on the horizon, we build those risks into our planning.”

And Chris Joye puts it all down to a rumourtage trade:

Sharp hedge fund researcher Jonathon Tepper, who used to work for Stevie Cohen’s SAC Capital Advisors, and his client, Bronte Capital’s long-short equities manager John Hempton, have vividly demonstrated how savvy media management can profitably transform part fiction into temporary fact.

…You see, Tepper’s clients had pre-positioned their portfolios weeks in advance of this publicity onslaught by short-selling bank stocks and lenders’ mortgage loss insurers like Genworth, and going “long” credit default swaps (CDS) that appreciate in value when investors think that bank repayment risks have increased.

Hempton told his Bronte Capital investors on February 9 that after a road trip with Tepper to check out “the real state of the Australian property market”, he had started initiating “mostly short” Australian positions. In this same letter he amusingly claimed that Tepper and he “wish to hold most of our [housing] research private”.

…Overnight a European investment bank told clients that there was “massive short-selling interest in the major banks [after the media coverage], and it all seemed to be based on misplaced views” of Aussie housing, which was triggering “mayhem”.

The next morning a domestic market-maker reported that there was “carnage here in [major bank] senior CDS, with Fast$ [hedge funds] jumping on the short trade after the Bronte Capital piece yesterday”. “The action in Bank CDS today would make one think there is a bank run going on in Australia,” he grimly surmised. By the end of the day, there had been dramatic 18 basis point and 35 basis point increases in the major banks’ senior and subordinated CDS spreads, moves that had not been seen since the global financial crisis.

…Another local investment bank advised clients that Bronte’s media was “getting traction in the US” and “the street decided today was as good a day as any to move in to full-blown panic on Bank CDS, which eventually dragged [the overall Australian CDS] index wider”.

A few points:

- the report was 40 pages long. I haven’t counted how many words were printed in the AFR but it was in the hundreds not thousands;

- when MB was permitted to publish an excerpt it was asked to keep the length to a minimum and to delay publication so that clients had time to execute trades.

Not that that means the report was not designed to impact markets. Appearing on 60 Minutes was quite a coup (though it did not release any of the report). But the report itself did remain mostly private.

Most importantly, Variant Perception did not create the trends in bank shares and CDS, they were long established before any of the recent price action. CBA shares were at current levels last August as the Mining GFC first took off and CDS prices were above 100bps already then as well. There are a number of clear macroeconomic reasons for this:

- we’re in the throes of perhaps the greatest commodity price bust in a century as China slows;

- US and emerging market high yield debt is under intense pressure;

- months ago that pressure spread into global bank CDS with particular spread widening around Aussie banks given their commodity economy exposure and offshore debt loads;

- the Australian economy is obviously at risk as the terms of trade collapse continues with the mining, car and resi capex cliffs, Budget problems, commitments to negative gearing reform and a chaotic election.

The Western Sydney mortgage sting did not create any of this. It has proven to be something a tipping point as all of these risks coalesce for markets. That is why Chris Joye is wrong to declare that Australian housing markets are safe and prices will keep rising, moreover, this:

The silver lining is that these dislocations are presenting investors with attractive opportunities. Some of the best trades done during the GFC domestically were sovereign wealth and super funds picking up super-cheap bank bonds and residential mortgage-backed securities.

Though I agree we may see spreads ease back for now, Mr Joye is looking in the wrong place for the “dislocation”. When the Australian housing bubble pops the pin will not come from within. The entire economy is now distorted around the bubble and policy-makers have no other goal than keeping it inflated. Local Australian exceptionalism is well intact.

The bubble will burst when one of two things happen:

- first, policy-makers will have to run out of ammunition. That point is closer than many realise with the RBA nearing exhaustion (one reason it does not want to cut again). Assuming we need to keep a spread to other nations of 50-75bps to fund the current account deficit, and banks will keep half of whatever cuts come from the RBA as offshore debt prices rise, households are left with only 50-75bps of potential relief if the Mining GFC (or some other shock) deteriorates. Fiscal policy is also limited and has scope for another stimulus perhaps half the size of the Rudd Government’s GFC effort before the AAA rating is lost. And if that happens then the first problem gets much worse.

- second, when global markets wake up to this growing precariousness they’ll simply ask for higher spreads on bank debt to offset the risks. Thus it will be a rupture in global Australian exceptionalism that will end the bubble with higher interest rates. That is the real damage done by the Variant Perception report.

But it is only the messenger. If you want to run an economic model based upon highly volatile income massively leveraged into unproductive assets using external debt then the tipping point is always going to come sooner or later.