From the ANZ quarterly update today:

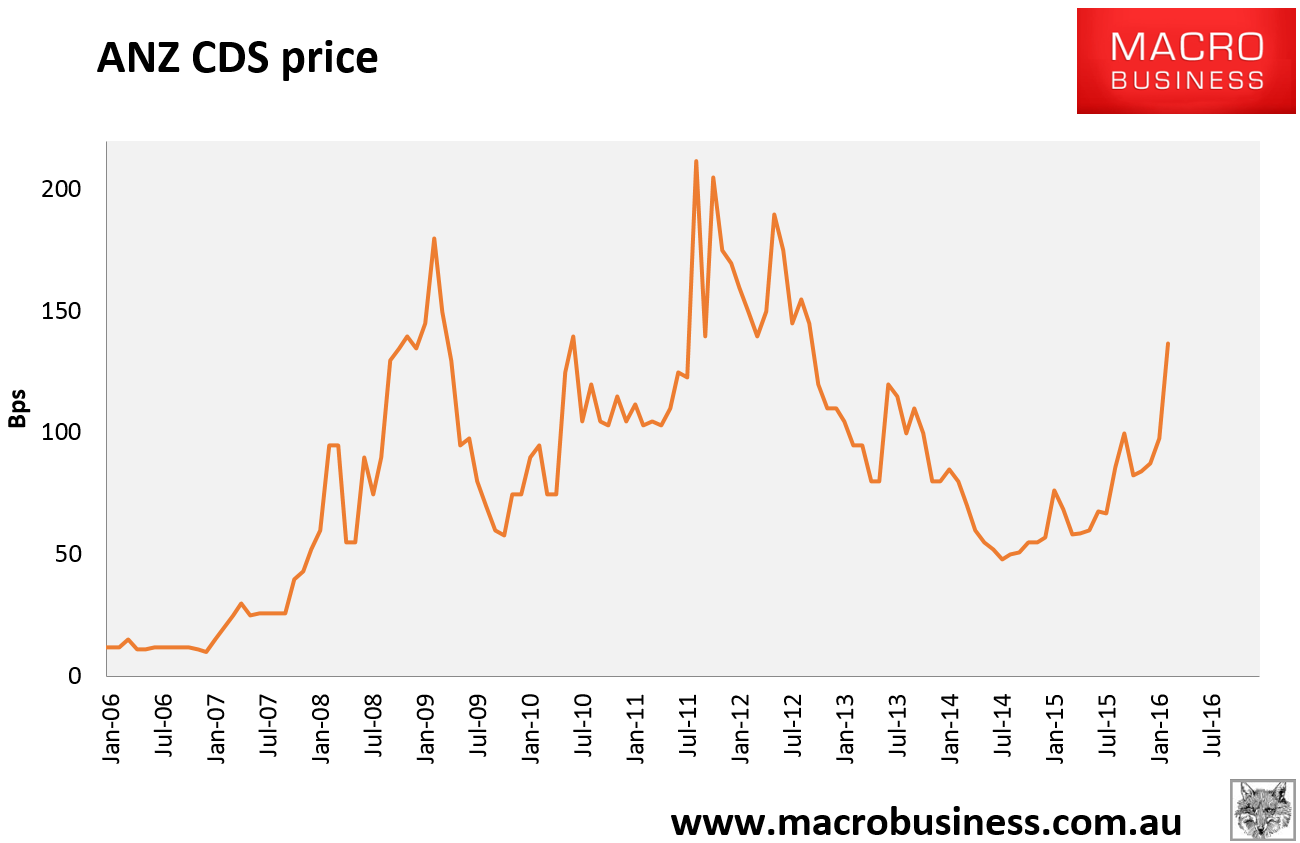

Bad debts up, largely in Asia. The other point of interest is the net interest margins remained stable only because the banks hiked rates in the quarter. Funding costs since then have ripped higher with ANZ sitting at 137bps today versus a third quarter average in the mid-80s range:

More rate hikes are coming. Here’s the Mac Bank take:

ANZ disclosed their 1Q16 trading update with the reported headline trends appearing reasonable, albeit the underlying result was slightly below market expectations. We are generally cautious in extrapolating too much from the quarterly trends, but in 1Q16 ANZ delivered positive Jaws (underpinned by expense management initiatives) and grew its markets income by 6% (vs 4Q15). Conversely, 1H16 guidance for BDD impairment charge of “little above $800m”, suggests that earnings in 2Q16 are likely to be below the first quarter, implying downside risk to consensus FY16 forecast (we are currently ~2% below consensus in FY16). Management hasn’t provided an update on the potential restructuring initiatives which remains a potential risk and is likely to continue to weigh on the market’s sentiment.

Impact

Cash profit of A$1.85bn came in broadly in line with our expectations and consensus – ANZ delivered an A$1.85bn cash profit for the quarter, broadly in line with MRE expectations of A$1.83bn and consensus of $1.88bn.

o Revenue growth exceeded cost growth – Whilst no exact guidance on the quantum of revenue and costs were provided, income grew at a faster rate than expenses. Costs were contained following a 2.5% reduction in staff numbers that largely offset wage inflation and investment in technology.

o Margin declined 2bps QoQ (flat ex Markets) – The margin was down 2bps for the quarter relative to the 2.04% reported at the 2H15 result and was flat excluding the impact of markets. Pleasingly the Institutional NIM improved, but the drag was likely funding costs and competition with the Retail and Commercial divisions.

o Markets income increased 6% (relative to 4Q15) to $553m in 1Q16. This is broadly in line with the quarterly FY15 average of $571m.

Asset quality broadly in line with our quarterly expectations, but a slight miss following 1H16 guidance – Impairment expenses were A$362m, broadly in line with our expectations of A$378m (26bps of GLAA). ANZ provided guidance for the 1H16 impairment charge of ‘a little above $800m’, which is above MRE ($760m) and consensus ($735m). Gross impaired assets were down ~10%, aided by the Esanda sale, with management expecting the 1H16 number will be ‘broadly similar to the second half of 2015’.

Capital generation reasonable with ~25bps of organic capital generation for the quarter– CET1 capital fell ~20bps to 9.4% driven by the payment of the full-year dividend. Excluding this impact, ANZ saw 45bps of CET1 improvement with ~20bps from the Esanda sale and the balance organically generated. We estimate ANZ’s proforma CET1 to be currently ~8.8% and should exceed 9% at 1H16.