The Fed minutes were out last night and were dovish within the hawkish trend:

After assessing the outlook for economic activity, the labor market, and inflation and weighing the uncertainties associated with the outlook, members agreed to raise the target range for the federal funds rate to 1/4 to 1/2 percent at this meeting. A number of members commented that it was appropriate to begin policy normalization in response to the substantial progress in the labor market toward achieving the Committee’s objective of maximum employment and their reasonable confidence that inflation would move to 2 percent over the medium term. Members agreed that the postmeeting statement should report that the Committee’s decision reflected both the economic outlook and the time it takes for policy actions to affect future economic outcomes. If the Committee waited to begin removing accommodation until it was closer to achieving its dual-mandate objectives, it might need to tighten policy abruptly, which could risk disrupting economic activity. Members observed that after this initial increase in the federal funds rate, the stance of monetary policy would remain accommodative. However, some members said that their decision to raise the target range was a close call, particularly given the uncertainty about inflation dynamics, and emphasized the need to monitor the progress of inflation closely.

Members also discussed their expectations for the size and timing of adjustments in the target range for the federal funds rate going forward. Based on their current forecasts for economic activity, the labor market, and inflation, as well as their expectation that the neutral short-term real interest rate will rise slowly over the next few years, members expected economic conditions would evolve in a manner that would warrant only gradual increases in the federal funds rate. However, they also recognized that the appropriate path for the federal funds rate would depend on the economic outlook as informed by incoming data. Members stressed the potential need to accelerate or slow the pace of normalization as the economic outlook evolved. In the current situation, because of their significant concern about still-low readings on actual inflation and the uncertainty and risks present in the inflation outlook, they agreed to indicate that the Committee would carefully monitor actual and expected progress toward its inflation goal. In determining the size and timing of further adjustments to monetary policy, some members emphasized the importance of confirming that inflation would rise as projected and of maintaining the credibility of the Committee’s inflation objective. Based on their current economic outlook, they continued to anticipate that the federal funds rate was likely to remain, for some time, below levels that the Committee expected to prevail in the longer run.

ADP labour data was also out and was bullish though is not usually a good lead on the Friday’s BLS report:

Private sector employment increased by 257,000 jobs from November to December according to the December ADP National Employment Report® … The report, which is derived from ADP’s actual payroll data, measures the change in total nonfarm private employment each month on a seasonally-adjusted basis.

…Goods-producing employment rose by 23,000 jobs in December, well up from a downwardly revised -2,000 the previous month. The construction industry added 24,000 jobs, which was roughly in line with the 21,000 average monthly jobs gained for the year. Meanwhile, manufacturing stayed in positive territory for the second straight month adding 2,000 jobs.

Service-providing employment rose by 234,000 jobs in December, up from an upwardly revised 213,000 in November. …

Mark Zandi, chief economist of Moody’s Analytics, said, “Strong job growth shows no signs of abating. The only industry shedding jobs is energy. If this pace of job growth is sustained, which seems likely, the economy will be back to full employment by mid-year. This is a significant achievement, given that the last time the economy was at full employment was nearly a decade ago.”

Advertisement

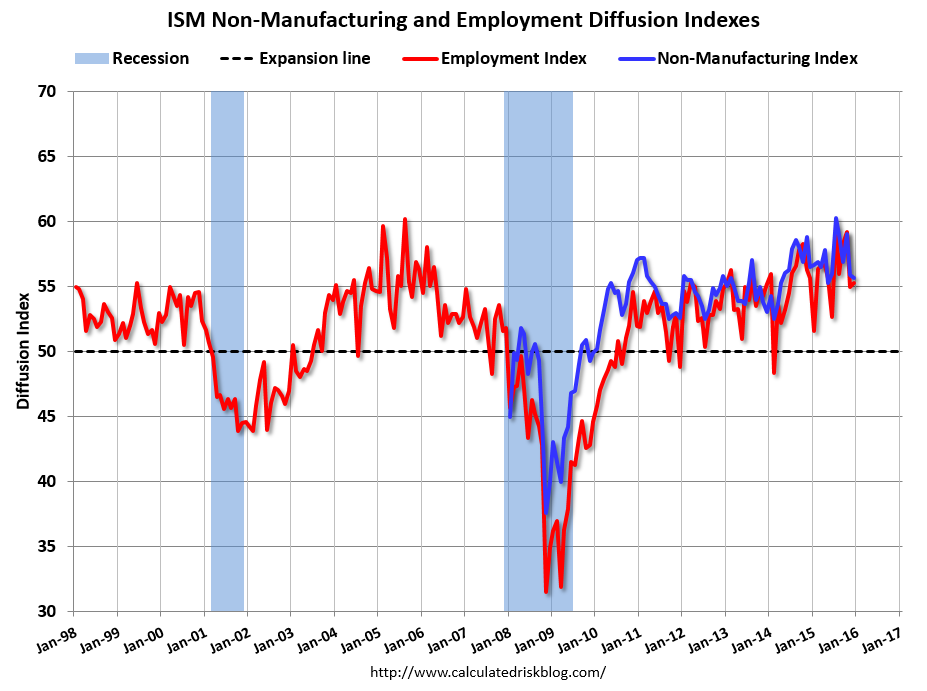

The services ISM was also decent (charts from Calculated Risk):

Economic activity in the non-manufacturing sector grew in December for the 71st consecutive month, say the nation’s purchasing and supply executives in the latest Non-Manufacturing ISM® Report On Business®.

The report was issued today by Anthony Nieves, CPSM, C.P.M., CFPM, chair of the Institute for Supply Management® (ISM®) Non-Manufacturing Business Survey Committee. “The NMI® registered 55.3 percent in December, 0.6 percentage point lower than the November reading of 55.9 percent. This represents continued growth in the non-manufacturing sector at a slightly slower rate. The Non-Manufacturing Business Activity Index increased to 58.7 percent, which is 0.5 percentage point higher than the November reading of 58.2 percent, reflecting growth for the 77th consecutive month at a slightly faster rate. The New Orders Index registered 58.2 percent, 0.7 percentage point higher than the reading of 57.5 percent in November. The Employment Index increased 0.7 percentage point to 55.7 percent from the November reading of 55 percent and indicates growth for the 22nd consecutive month. The Prices Index decreased 0.6 percentage point from the November reading of 50.3 percent to 49.7 percent, indicating prices decreased in December for the third time in the last four months. According to the NMI®, 11 non-manufacturing industries reported growth in December. Faster deliveries in December contributed to the overall slight slowing in the rate of growth according to the NMI® composite index. All of the other component indexes increased in the month of December. The majority of respondents’ comments remain positive about business conditions and the overall economy.”

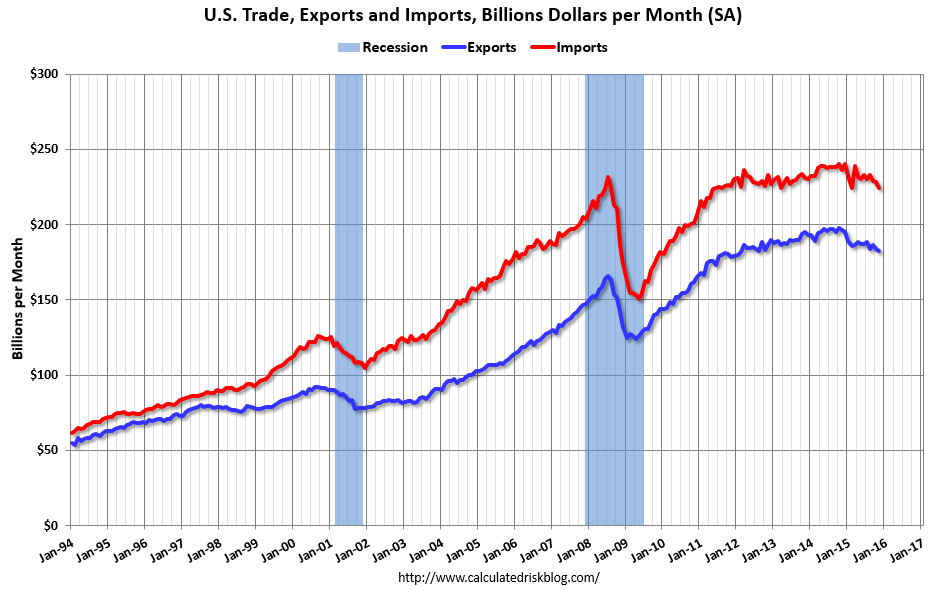

And the trade deficit narrowed:

The U.S. Census Bureau and the U.S. Bureau of Economic Analysis, through the Department of Commerce, announced today that the goods and services deficit was $42.4 billion in November, down $2.2 billion from $44.6 billion in October, revised. November exports were $182.2 billion, $1.6 billion less than October exports. November imports were $224.6 billion, $3.8 billion less than October imports.

However, exports falling less fast than imports is not really the path to a closing trade gap that you want to see for a strengthening cycle. Expect a very slow moving Fed.