Around 18 months ago, the SMSF Owners’ Alliance displayed extraordinary self-interest when it slammed calls to tighten tax concessions around superannuation, arguing that the rich were entitled to their tax breaks:

The $1.8 trillion superannuation industry has defended its generous tax breaks, saying it should not be used as a cash cow to rescue the budget deficit at the cost of healthy retirement savings.

…an alliance of self-managed funds said that the rich were just as entitled to benefits…

“People who work harder and save more are going to have larger superannuation balances – it doesn’t mean you’re rorting the system.”

Today, the SMSF Owners’ Alliance has displayed more shameless self-interest, throwing support behind cutting superannuation concessions for the wealthy provided the tax on super earnings is eliminated and the top marginal tax threshold is raised. From The AFR:

Under SMSFOA’s plan, money paid into super would be taxed at a discount of 15 per cent to the individual’s applicable marginal income tax rate, a suggestion made in a proposal unveiled by accounting and advisory firm Deloitte in October.

“However, the Deloitte proposal did not include dropping the tax on earnings in the accumulation phase so would actually help raise more money for the government, which we don’t think should be the focus of super tax reforms,” SMSFOA head of research Malcolm Clyde said.

“Our plan would be revenue neutral for the government..

SMSFOA’s support for a progressive tax on super contributions… is conditional on it being done in combination with abolishing all tax on investment earnings on super…

Another caveat on SMSFOA’s support for a progressive contributions tax is that the threshold at which income earners enter the top marginal income tax rate of 45 per cent must be lifted…

So let’s get this straight. With the costs from the Aged Pension and superannuation concessions growing inexorably, the Federal Budget will be bled dry.

But instead of curbing this drain, the SMSF Owners’ Alliance insists that any super reform must be “revenue neutral”, whilst also demanding that the top marginal tax rate threshold be increased?

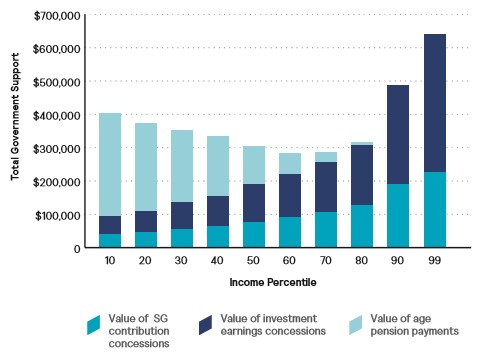

Sure, making contribution taxes on superannuation concessions more progressive is a hugely positive move and would unquestionably help assist lower income earners, to the detriment of higher earners. However, what the SMSF Owners’ Alliance has conveniently failed to mention is that it is the wealthy that derive most benefit from concessions on superannuation earnings, and that eliminating the earnings tax would likely benefit them the most (given they have the highest super balances).

Therefore, the SMSF Owners’ Alliance’s proposal is largely an example of giving with one hand (via less concessions on contributions) but taking with the other (via greater concessions on superannuation earnings, plus an increase in the top marginal tax threshold).

Ultimately, the only way to both improve equity in the super system and help balance the Budget is to do the following:

- Tax superannuation contributions at a progressive but concessional rate (e.g. marginal tax rate less 15%);

- Tax superannuation earnings in both the accumulation and retirement phases, thus extending the 15% tax rate to fund earnings in the retirement stage (perhaps with an offset for people earning below the tax-free threshold);

- Placing a lifetime cap on superannuation nest eggs;

- Curbing the generous “transition-to-retirement” superannuation rules, which enable those approaching retirement to avoid paying tax; and

- Limiting lump-sum withdrawals, thus preventing people from blowing their funds and falling back on the Aged Pension.

Just don’t expect the rent seekers in the super industry to champion such comprehensive reforms.

unconventionaleconomist@hotmail.com