By Martin North, cross-posted from the Digital Finance Analytics Blog:

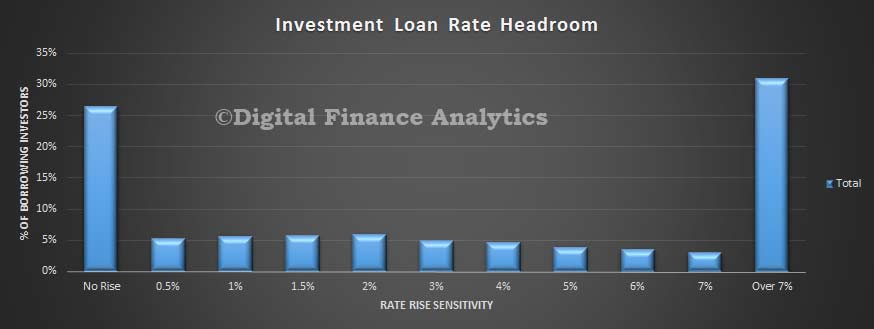

Continuing our series on potential material risks within investment loans, today we reveal some of the analysis we have undertaken on the potential impact on investors of prospective rate rises using data from our household surveys. We framed the questions here around how large a rise could an individual household cope with before getting into financial discomfort. We considered scenarios between zero and 7%. The overall results are startling. We found that about a quarter of property investors said they would have difficulty meeting any additional interest rises – even 0.5% – implying that they are already under financial pressure. Others could cope with various rises, though more than 50% of investors would be in potential difficulties should rates rise by 3%. On the other hand, more than 30% of investors were able to cope with a significant rise, even above 7% from current levels.

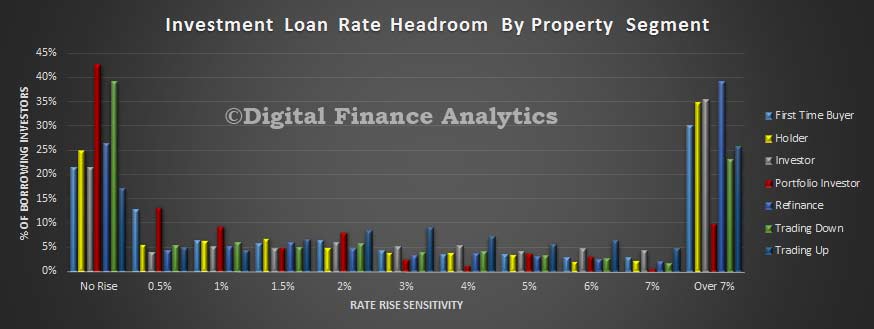

So which households are most exposed? We start by looking across the DFA property segments. We found that 20% of first time buyer investors would be concerned by any rise, whereas more than 40% for portfolio investors (who are more highly geared) and a considerable proportion of people who traded down and geared into an investment property recently would be caught out. Others, such as those refinancing, or holding property appear to be more able to swallow potential rises.

So which households are most exposed? We start by looking across the DFA property segments. We found that 20% of first time buyer investors would be concerned by any rise, whereas more than 40% for portfolio investors (who are more highly geared) and a considerable proportion of people who traded down and geared into an investment property recently would be caught out. Others, such as those refinancing, or holding property appear to be more able to swallow potential rises.

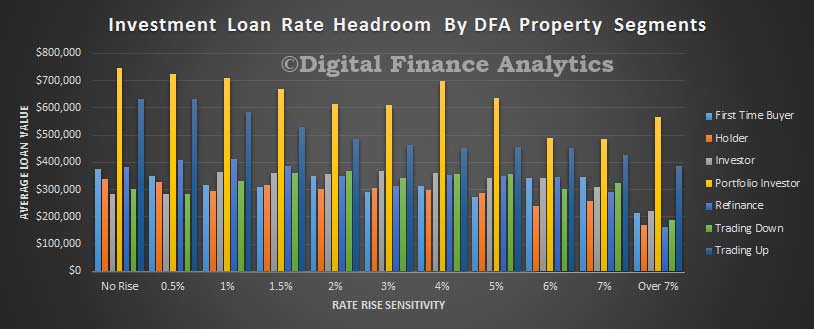

The size of the loan portfolio has a bearing on households, with the average portfolio investor having a balance of over $750,000 in investment property (some much more) so would be more sensitive to rate rises.. We conclude that generally households with smaller investment loans are (perhaps obviously) a little more able to cope with potential rises.

The size of the loan portfolio has a bearing on households, with the average portfolio investor having a balance of over $750,000 in investment property (some much more) so would be more sensitive to rate rises.. We conclude that generally households with smaller investment loans are (perhaps obviously) a little more able to cope with potential rises.

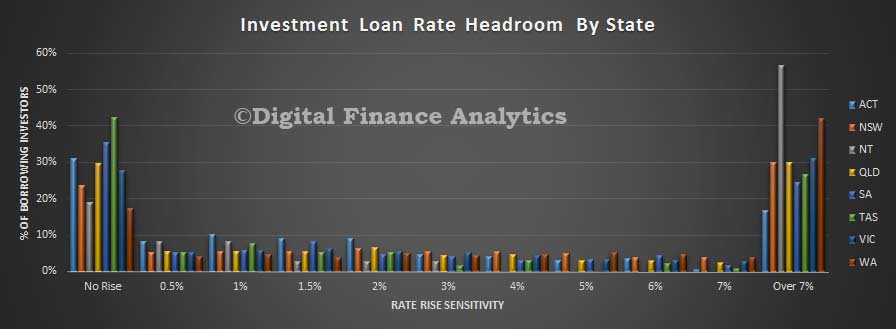

Next we cut the data by states. Here we found that investors in TAS were most concerned about potential rate rises, followed by SA and ACT. These are states were income growth (and property appreciation) is slowest. On the other hand, investors in WA and NT appeared more able to cope with significant rises

Next we cut the data by states. Here we found that investors in TAS were most concerned about potential rate rises, followed by SA and ACT. These are states were income growth (and property appreciation) is slowest. On the other hand, investors in WA and NT appeared more able to cope with significant rises

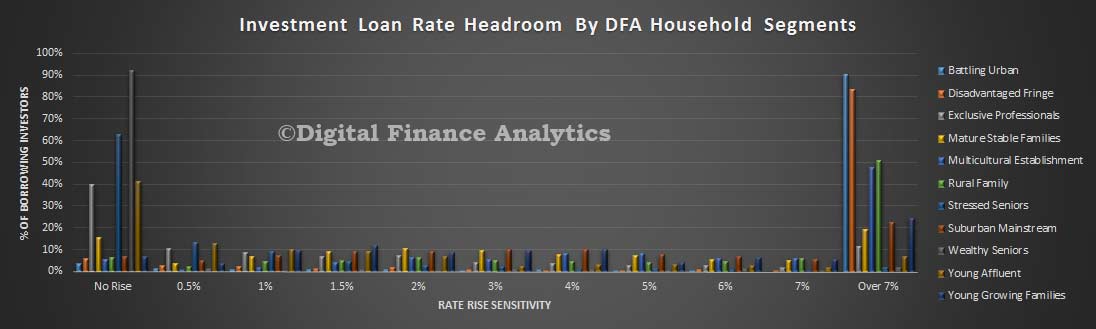

Finally, we examine the data by our core household segments. Here we found that wealthy seniors were the most exposed (incomes relatively flat compared with their investment portfolios), followed by stressed seniors and young affluent.

Finally, we examine the data by our core household segments. Here we found that wealthy seniors were the most exposed (incomes relatively flat compared with their investment portfolios), followed by stressed seniors and young affluent.

Of course, if rates were to rise – perhaps this is not likely in the near term – investors have the option of selling up, but the analysis shows that some would need to act quite fast in a rising rate environment. It also raises the question as to whether the banks underwriting criteria are working – because they should be assuming borrowers could cope with a rise to above 7.5%, which is 2-3% higher than most are currently paying. Our research suggests that some households are geared up to the hilt, and have no spare cash for unexpected raises down the track.

Of course, if rates were to rise – perhaps this is not likely in the near term – investors have the option of selling up, but the analysis shows that some would need to act quite fast in a rising rate environment. It also raises the question as to whether the banks underwriting criteria are working – because they should be assuming borrowers could cope with a rise to above 7.5%, which is 2-3% higher than most are currently paying. Our research suggests that some households are geared up to the hilt, and have no spare cash for unexpected raises down the track.

Next time we will add in the impact of owner occupied borrowing also.