Citi offers some interesting long cycle material today:

During the Cold War, and for the most part after it ended, the United States served as the direct and indirect guarantor of stability around the globe. Its national interests were globally defined, and by protecting them, it supported and promoted the interests of many other nations interested in regional stability, free markets, open trade routes, and unfettered access to global commodity markets.

The United States, through diplomatic activism backed up by unrivaled military power, kept many regional conflicts under control (or pacified them), such as between Pakistan and India, North and South Korea, Israel and its neighbors, and the states of the former Yugoslavia. It did not dominate world affairs in a hegemonic way (which would have been impossible even for the US), but it served as the arbiter of last resort and the world’s reserve power. After 1989, most nations buying into the post-Cold-War surge of economic globalization consumed US stability services around the world, even those who openly or clandestinely opposed America’s relative dominance.

But this fortunate power structure has changed significantly over at least the last decade. The US position in global affairs has weakened. Other powers have gotten stronger. Some military interventions, such as the Iraq war, have eroded both US credibility and resources, an outcome supported by a host of global public opinion data. Less political capital is available in Washington to underpin America’s global role, leading to a “leadership from behind” culture that is considered to be ineffective and widely perceived as US weakness. Inward-looking, isolationist leanings have gained political traction in America’s political mainstream. The threshold of what constitutes US national interest has narrowed markedly in comparison to previous decades.

…Competing institutions have been established or are in the process of being set up, such as the Asian Infrastructure Investment Bank (AIIB).The overall ability of the system to enforce the formal and informal rules of the established system of global order is critically compromised. Its effects can be observed around the globe, but perhaps most explicitly in and around Europe, the Middle East and Asia.

…As a net result of all of these trends and developments, local and regional crises around the world play out stronger and more intensively than they used to. Weaker cohesion and diminished disciplining power make escalations of small conflicts more likely and encourage rogue states and opponents of liberal order to assert themselves more self-confidently. Stability in the overall system is weakened and likely to further deteriorate incrementally. The assessment of political risk in and around Europe, and around the world, needs to be made against this backdrop.

Back in the nineties when the academic world was besotted with notions of the “end of history” and the triumph of liberal democracy, markets concocted their own version of US primacy in the rise of equity premiums. Known at the “peace dividend” it help stretch price earnings ratios to much higher than average levels given, so the argument ran, because US primacy guaranteed less political risk.

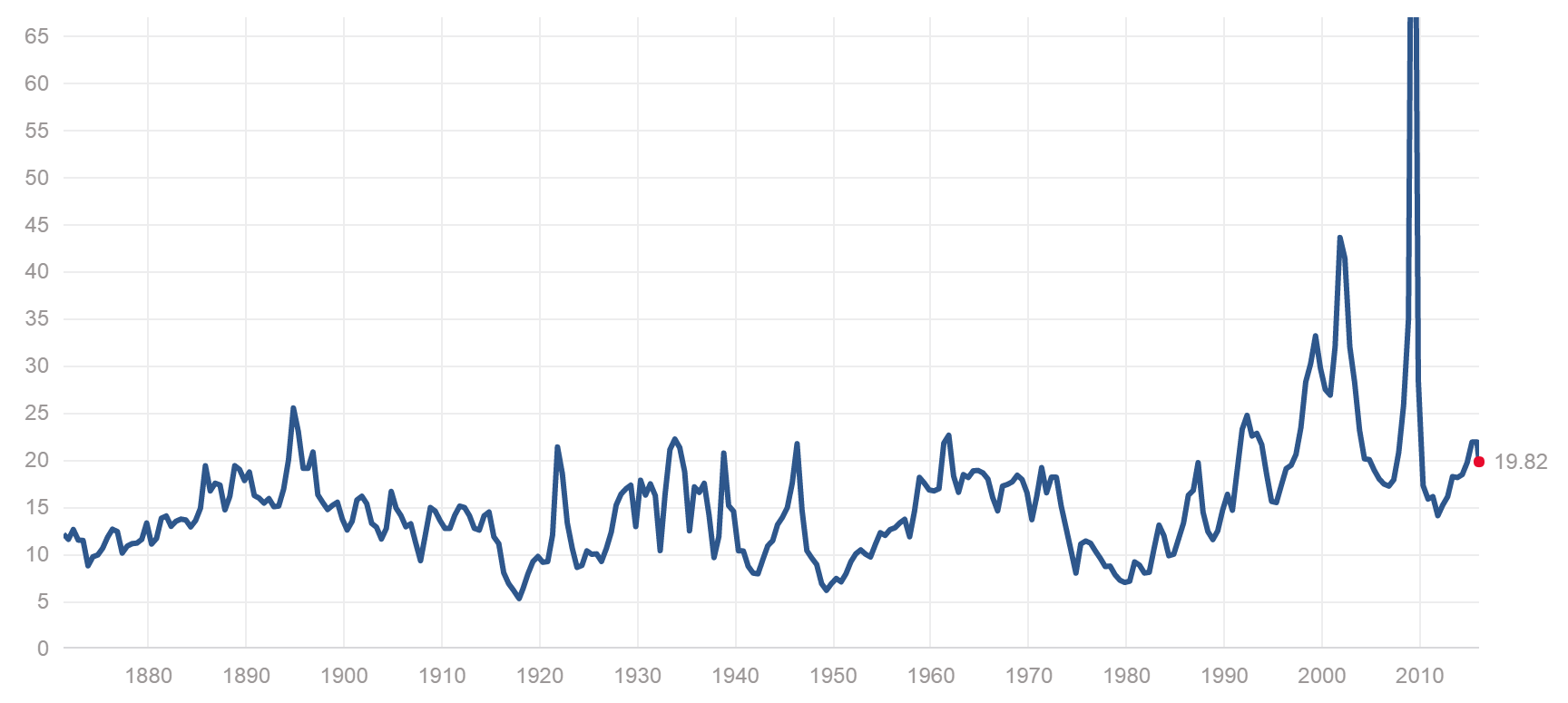

We can see this in the history of S&P500 PEs:

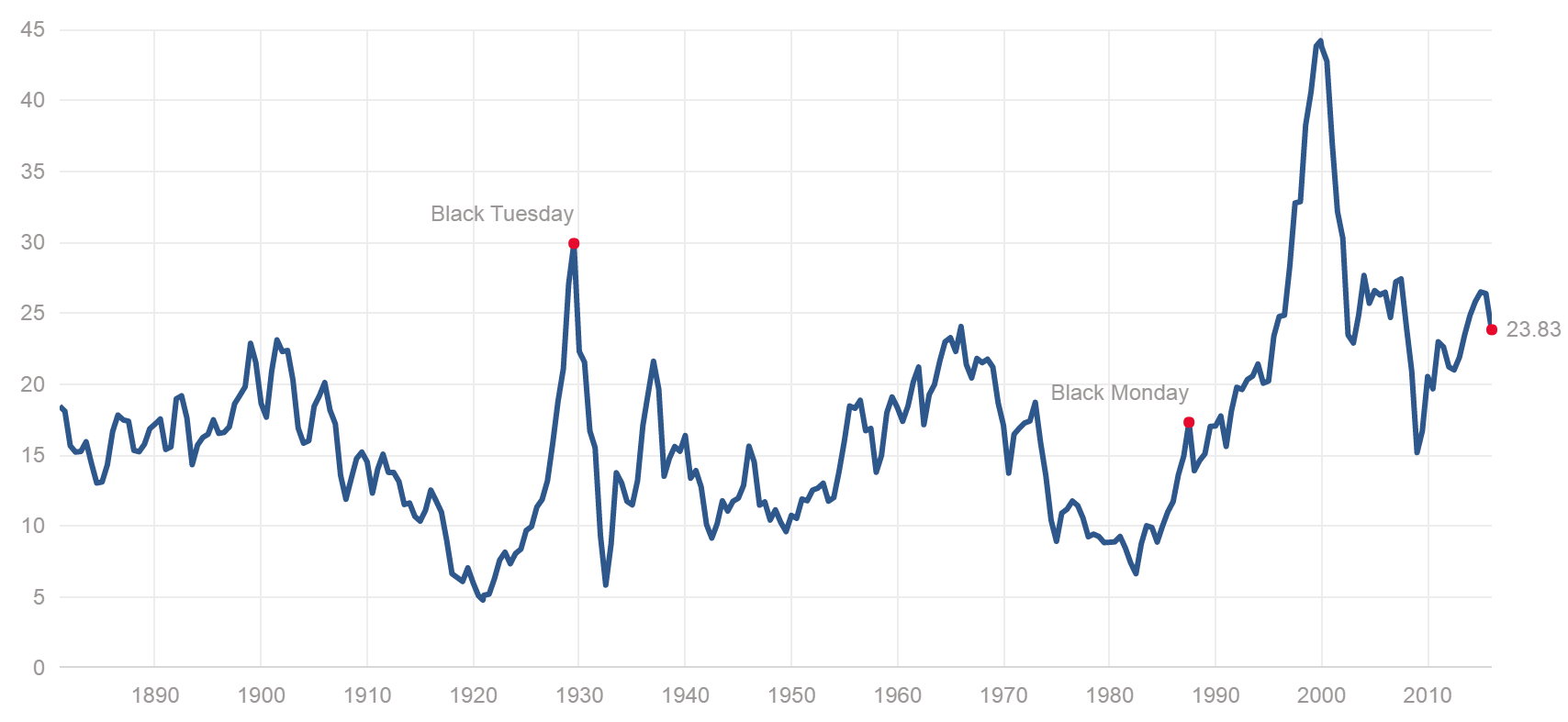

It is even more clear in the Shiller PE which uses ten year average earnings:

As you can see, current valuations remain very stretched relative to historical ranges.

This is not say that the “peace dividend” is to blame for all of the current overvaluation. Rather, it offers a higher baseline from which falls bounce and a higher ceiling to which rallies rise.

Or did. If Citi is right then not for much longer!

Of particular concern for this cycle is the manner in which the Sunni-Shia proxy wars of the Middle East are spilling over into Europe via the ISIS guerrilla campaign. If Europe is destabilised by further terrorist attacks driving the rise of separatist political parties, such as we are seeing in France now, then the sustainability of the euro will become a fundamental drag on global markets.