From Paul Mackel and Ju Wang at HSBC comes the view that 2016 will see the Chinese Renminbi (RMB) weaken appreciably:

The combination of weak cyclical and structural forces is seen working against the currency. We see USD-CNY finishing 2016 at 6.70. HSBC’s forecast for the EUR and JPY to strengthen against the USD reinforces our view that the broad CNY effective exchange rate should moderate further.

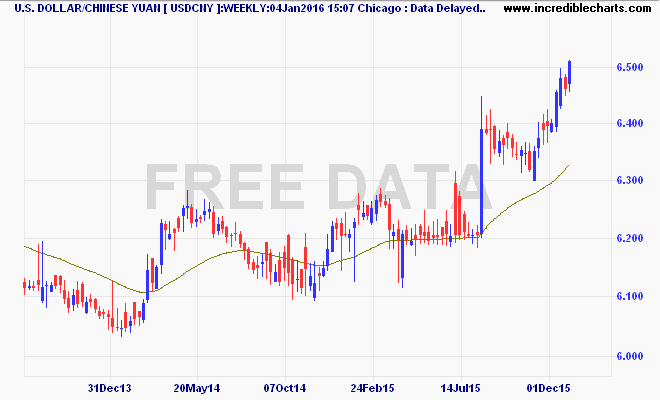

What happened in December?

The RMB traded very weak in December, losing nearly 2% against the USD. In our view, its weakness was a function of a few things, including:

1) A relatively hands off approach: The USD-CNY fixing was at times more accommodating and there was seemingly less spot intervention by the PBoC following the RMB’s inclusion in to the IMF’s Special Drawing Rights (SDR) and before the December FOMC meeting2) An introduction of a RMB index by CFETS which highlights the policy preference for a more independent currency, as China gradually moves towards a “clean floating” FX regime

3) The reported tightening of cross border yuan business (Bloomberg, 30 December 2015), which could slow down corporates’ capabilities to converge the onshore and offshore RMB basis.

So far the RMB is already on the back foot at the beginning of 2016. The USD-CNY fixing came at 6.5032, higher than the onshore spot closing on 31 December 2015, which we feel confirms the central bank’s slightly more permissive bias.

Over the coming months, we will be watching the interplay of FX policy with the structure of China’s corporate net FX liabilities, the economy’s trajectory, and how the RMB behaves heading into the coming Fed meetings. .

And its not just against the USD:

Although a weaker RMB is likely to be a dominant theme for 2016, the focus should also be on its expected rise in volatility. On the broad picture, HSBC’s David Bloom believes the USD will weaken against EUR and JPY over time given the latter two face constraints on additional monetary easing, largely because their central banks are running out of bonds to buy. Considering the significant weight of the RMB in the Fed’s trade-weighted USD basket, significant weakness of the former would likely increase concern over excessive USD strength by US policy makers. The upcoming US election in 2H could also add to uncertainty in USD-RMB exchange rate, and it tends to be a political topic during elections historically.

On the domestic side, there will also be important events to watch out for the RMB this year. These include the 13th Five-Year Plan for 2016-20, which is likely to be approved at the National People’s Congress in March, MSCI’s assessment of China’s A-share, and China’s G20 leadership.

The RMB should weaken further and trade with greater two-way volatility. We see USD-CNY at 6.70 at end 2016. Our framework incorporates HSBC’s view that the EUR and JPY will strengthen against the USD, as well as cyclical headwinds from China’s growth slowdown. We have recommended selling CNH-JPY as one of the top 2016 trade ideas to position for this.

Although higher RMB volatility could trigger some concerns for EM FX initially, that reaction should eventually moderate over time. The market will need to accept that this is part of China’s macro adjustment and comes at a time when the country is becoming more of a capital exporter.

Emerging market volatility is set to go even higher on this weakness train that everyone but the US has stepped aboard.