Bank of America is spooking the analyst world with a near airtight case for financial instability in the Middle Kingdom in its most recent note.

As strategist David Cui explains

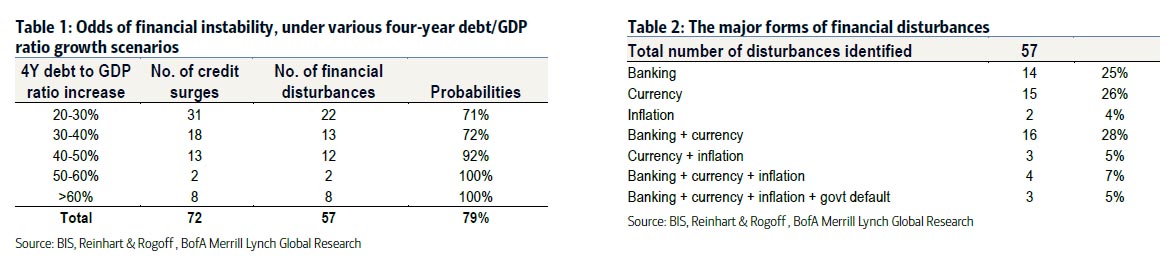

It’s widely accepted that the best leading indicator of financial instability is rapid debt to GDP growth over a period of several years as it’s a strong sign of significant malinvestment. Based on Bank of International Settlement’s (BIS) private debt data and the financial instability episodes identified in “This time is different”, a book by Reinhart & Rogoff, we estimate that once a country grows its private debt to GDP ratio by over 40% within a period of four years, there is a 90% chance that it may run into financial system trouble (Table 1). The disturbance can be in the form of banking sector re-cap (with or without a credit crunch), sharp currency devaluation, high inflation, sovereign debt default or a combination of a few of these (Table 2).

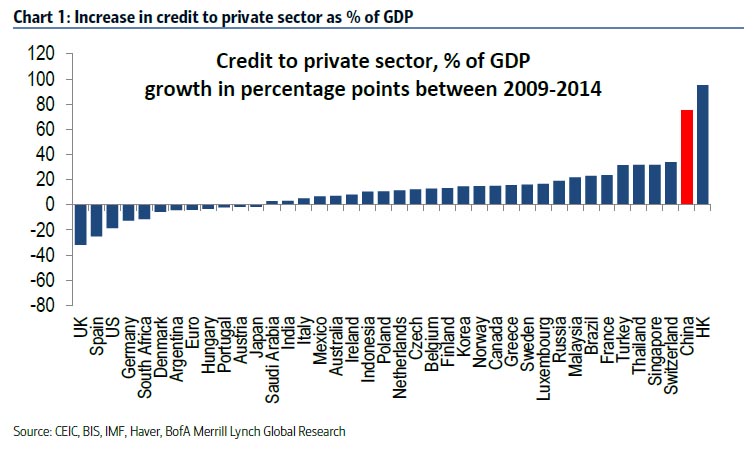

As Chart 1 demonstrates, China’s private debt to GDP ratio rose by 75% between 2009 and 2014 (i.e., since the Rmb4tr stimulus), by far the highest in the world (we suspect a significant portion of the debt growth in HK went to China). At the peak speed, over four years from 2009 to 2012, the ratio in China rose by 49%.

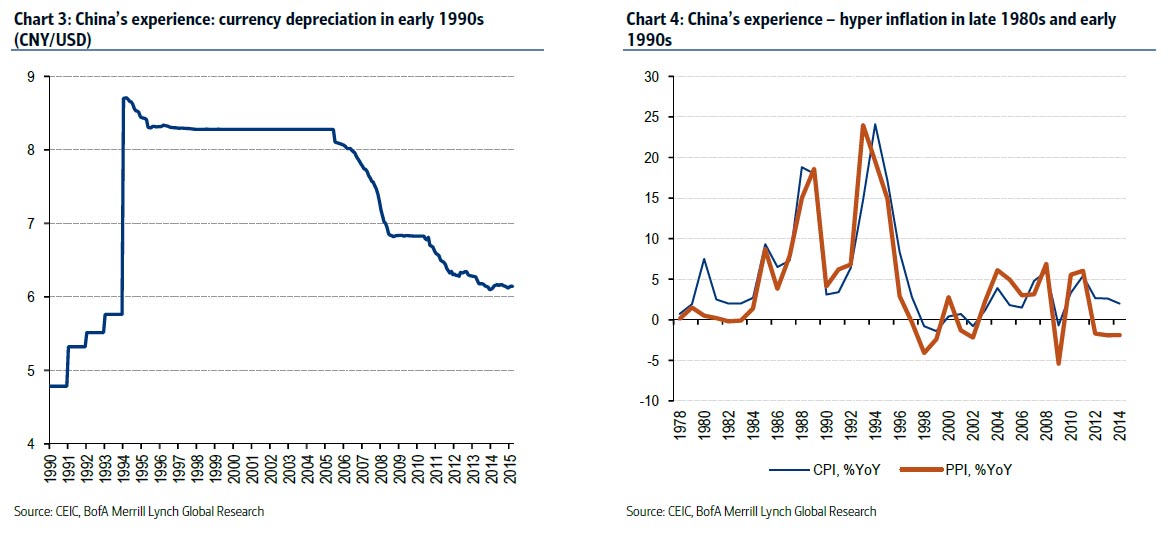

Other than sovereign debt default, China has experienced all the other forms of financial instability since the open-door reform started in late 1970s, including a sharp currency devaluation in the early 1990s (Chart 3) and hyper-inflation in the late 1980s and early 1990s (Chart 4). China also needed to write-off bad debt and recap its banks every decade or so. Banking sector NPL reached some 40% in the late 1990s and early 2000s and the government had to strip off some 20% of GDP equivalent of bad debt from the banking system between 1999 and 2005.

When debt problem gets too severe, a country can only solve it by devaluation (via the export channel), inflation (to make local currency debt worth less in real terms), writeoff/re-cap or default. We judge that China’s debt situation has probably passed the point of no-return and it will be difficult to grow out of the problem, particularly if the growth continues to be driven by debt-fueled investment in a weak-demand environment. We consider the most likely forms of financial instability that China may experience will be a combination of RMB devaluation, debt write-off and banking sector re-cap and possibly high inflation. Given the sizeable and unstable shadow banking sector in China and the potential of capital flight, we also think the risk of a credit crunch developing in China is high.

In our mind, the only uncertainty is timing and potential triggers of such instabilities.

To put things into perspective from an Australia viewpoint over the medium to long term, China can manage a bad cold, but the Chief Mine and Dodgy Money Laundry center to the Middle Kingdom will fall over on a sneeze. Fiscal stimulus is no longer an option as it increases the risk of instability and malinvestment, and material demand for goods from Australia will dwindle as the RMB depreciates.