by Angus Nicholson, IG

The “National Team” has answered the markets’ call, fixing the CNY’s mid-point slightly stronger and intervening heavily in Mainland Chinese equity markets. Chinese government intervention has brought some relief to risk assets, with many equity markets seeing a noticeable bounce in the wake of the CNY fix release. Although confidence in China’s ability to manage their capital markets has only been further damaged after they announced the removal of their “circuit breakers” after only being in place for four days (sending the market limit down 50% of the time) and rumours circulating that CSRC head Xiao Gang would be resigning tomorrow. Given confidence in China’s ability to manage its equity and FX market has been badly damaged it is not surprising to see a comparatively muted global reaction. Markets will be waiting to see the Chinese government’s determination to prop up the stock market and the currency into next week before any major recovery rally is likely to be seen.

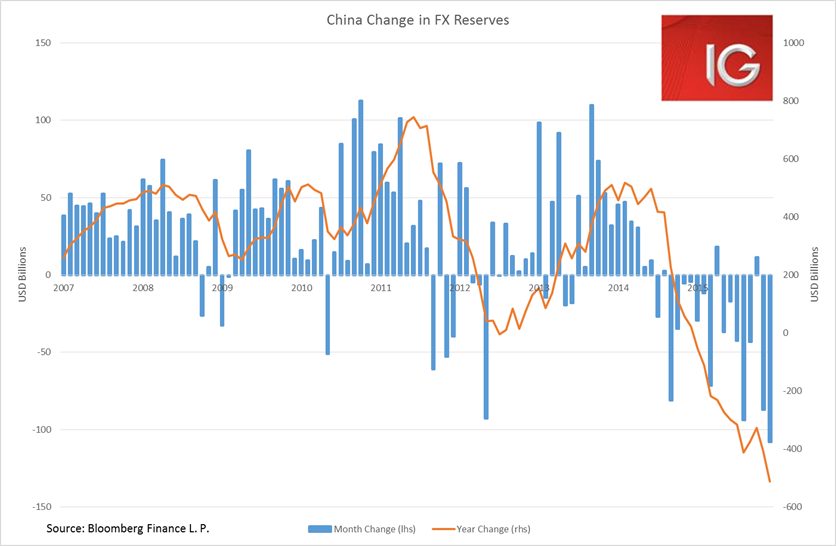

Despite the onshore CNY weakening a further 0.56% yesterday, which usually determines the fix for the following day, the authorities decided to ignore their new market based reforms today and keep the midpoint relatively unchanged. Overnight, China’s December FX reserves statistics were released showing a further US$108 billion decline in reserves to US$3.3 trillion. While China’s total reserves are still enormous at an aggregate level, they are unlikely to want to see those sorts of declines consistently on a month-to-month basis. Hence, why they may be pulling back from direct intervention in the onshore CNY to assure a close near where they want to set the midpoint the next day. If this turns out to be true, where China sets the fix each day could be anyone’s guess. Expect lots of FX volatility around 12 pm AEDT.

The other rumour causing a tizzy in the markets at the moment is the Reuters report stating that some PBOC advisors are calling for a one-off 10-15% devaluation in the CNY. This is far more than anyone in the markets was predicting, even by the end of 2016! A further 15% devaluation from its current valuation at the moment would have seen the CNY weaken by over 21% since its early-August levels – quite a move for a currency previously known as one of the most boring to trade in the world. I should add though that a 15% devaluation and a firm intervention to hold the currency there and probably prop up the equity markets is by far the best scenario for global markets than a protracted war of attrition in the CNY between authorities and speculators. These are the clear lessons from previous currency crises such the European Exchange Rate Mechanism (ERM) in 1992 and the Asian Financial Crisis in 1997-1998.

The bigger question some may be asking is how did we get to this point so quickly? A quick summary:

As recounted in Huang Yasheng’s “Capitalism with Chinese Characteristics”, the development of Shanghai’s Pudong area in the 1990s through the use of what later became known as local government financing vehicles (LGFVs) pioneered a way for local governments to avoid capital constraints and load up on debt to pursue development projects. Huang Qifan, a former member of the team that developed Pudong, moved to Chongqing where he led one of the most ambitious municipal developments in the whole country. In the space of a decade, he turned what was basically an enormous refugee camp for displaced former residents of areas flooded by the Three Gorges Dam into a bustling contemporary metropolis – with an enormous LGFV debt burden.

Henry Sanderson and Michael Forsythe’s “China’s Superbank” tells the other side of this story. In the 2000s, the China Development Bank (CDB) under the guidance of Chen Yuan (the son of one of China’s “Eight Immortals” party elders of the 1980s, Chen Yun) took these lessons from Pudong and Chongqing and replicated them on a mass scale across the country.

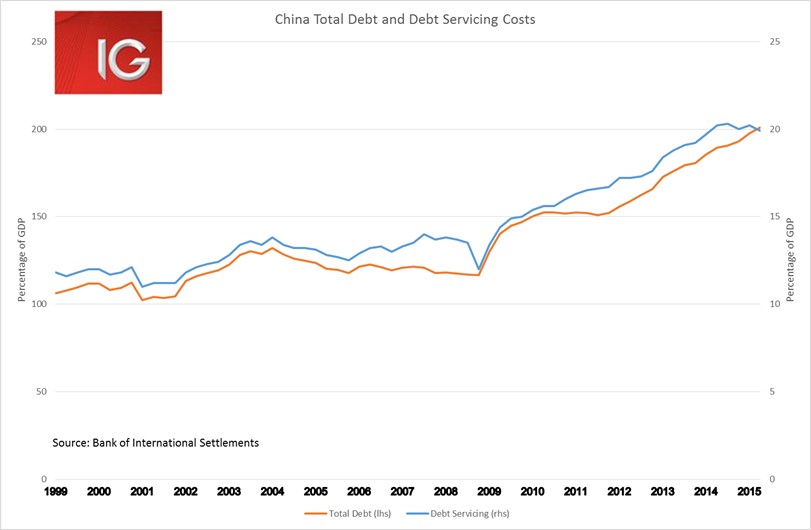

These historical precedents for the LGFV structure set the scene for an enormous debt binge in 2009-2010 when China unleashed the largest counter-cyclical stimulus ever seen. Add to this the weak central government control of the provinces under the Hu Jintao-Wen Jiabao regime and jockeying among provincial governors ahead of the leadership transition in 2012, and China was on course for an enormous expansion of debt. According to BIS statistics, the percentage of debt to GDP has increased by 76.3 percentage points from 2009 to 2014. As pointed out in Carmen Reinhart and Kenneth Rogoff’s seminal overview of financial crises over eight centuries, “This Time is Different”, this sort of short term run up in debt has almost always resulted in a financial crisis.

The Lou Jiwei led-Ministry of Finance has been undertaking the mammoth task of taking these previously accumulated off balance sheet LGFV liabilities and reissuing them through provincial government bonds. These provincial government bonds will eventually become the main source of funding for provincial development projects, the problem is old accumulated liabilities have to be issued first before fresh funding can be issued. The government has been forced to up the limit and issue roughly CNY 3.8 trillion provincial bonds in 2015. Provincial bond issuance in 2016 is likely to be over CNY 4 trillion. Banks have been forced to pick up this issuance at far higher prices than they would like, which has further hurt access to credit for small and medium enterprises – another reason for the decline in the (SME-dominate) Caixin PMIs this week.

So given China’s increasingly precarious domestic debt situation, credit has been drying up and adding to deflationary pressures in the economy. One fix to this predicament is to lower the nominal value of these debts by devaluing the currency. This, of course, comes at the cost of foreign currency denominated liabilities of which it has been estimated Chinese corporates have amassed roughly US$700 billion worth. But given the strained domestic credit situation, the benefits of lowering the nominal value of domestic debts clearly outweighs these foreign liability concerns. The important Chinese corporates with large foreign currency liabilities can be bailed out, and those of less importance can be left to default.

Of course, this scenario will only create more pain for already embattled emerging markets, particularly those strained with large debt burdens and current account deficits. The GFC is the wrong comparison to draw here. The potential global macro effects from a Chinese devaluation in conjunction with a US rate hiking cycle is far more akin to the AFC in 1997, but personally the correlation with the selloff in oil makes the emerging market selloff in the early-1980s (particularly associated with the “Southern Cone” countries of South America) the most apt. If this scenario does occur it would provide a major leg up in the US dollar (the DXY dollar index going above 110) and Japanese yen (below 105) and a furious initial selloff in global equities. This could see the Fed be forced to trim rates back to zero and a raft of further easing from other global central banks. But if China had enough fire power to support the currency at those weaker levels and prop up other aspects of the economy, global risk appetite could actually rebound quite quickly. A scenario far more preferable to a protracted period of global market losses and economic weakness. Hold onto your hats and stop losses, 2016 is likely to be a wild year.

Ahead of the European open we are calling the FTSE +1 , DAX -49 , CAC -22