Angus Nicholson for Chris Weston, IG

Remember how China was going to stimulate heavily in Q3 and Q4 to stabilise the economy and quell global investor concerns before the Chinese New Year economic data blackout in February 2016? Well turns out, that’s not going to happen. The Year of the Fire Monkey is shaping up to be less decisive and energetic, and more lost and abandoned in a Canadian Ikea…

Asian markets looked in for a rough session with futures pointing to a negative open for markets across the region. Nerves were also running high for the open of the Chinese markets and whether we would see another 7% limit down performance for the index. Chinese markets initially surprised with a move into positive territory, helping rally the Nikkei as well as European and US futures markets.

Moves are likely to be quite volatile until the Chinese close, with investors now facing even shorter time frames to get out of stock if they want to sell. Many of China’s newly introduced “circuit-breakers” look to have only compounded panic selling yesterday as investors rushed to get their sell order out the door before they got caught in a limit-down. This is no doubt present in Chinese traders’ minds today, with many prepared to shoot off a ton of sell orders at the drop of a hat if they want any hope of getting them executed.

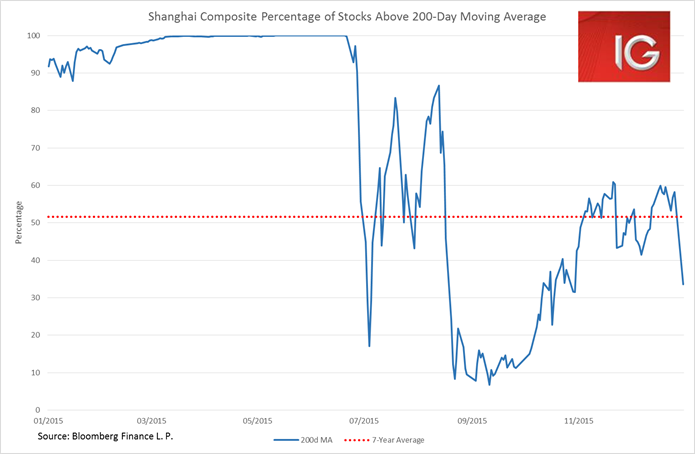

The moves seen in Chinese stock markets are quite concerning. Many market internals point to a likely renewed selloff and a revisit of the late-August lows. The percentage of companies trading above their 200-day moving average plunged to 33.5% – the lowest level since 3 November. These are very low levels; apart from 2015’s August and September selloff, this indicator has rarely dropped below 40%. Even though there had been somewhat of a recovery in Chinese equities in the fourth quarter of 2015, market breadth was greatly lacking with the market struggling to hold over 50% of companies above their 200-day moving average.

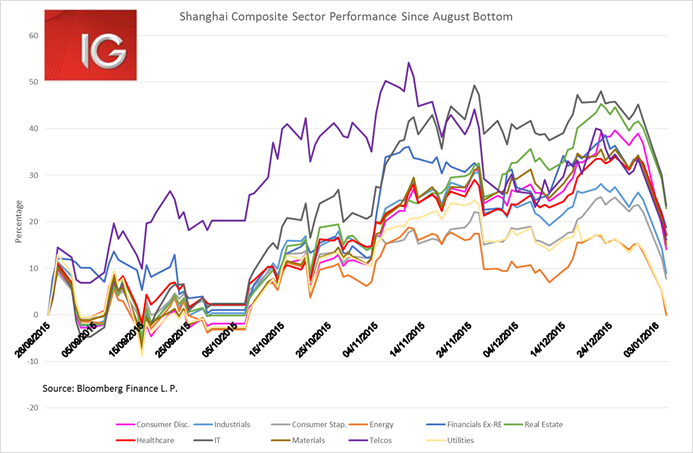

Looking at the sectoral performance, it is very clear that yesterday’s move was a broad-based perception of market risk, quite possibly escalated by the new circuit-breakers. What is most concerning in the sectoral view of the market is that energy and utility stocks have completely given up any gains since the Shanghai Composite bottomed on 26 August. Another major leg down for the Chinese markets would see industrial and consumer staple stocks also having entirely given up their gains from the latter half of 2015.

The other China concern of the moment is the renewed weakening of the renminbi with the mid-point fix weakening the currency by a further 0.21% today. The offshore USD/CNH rate has now weakened by 6.8% since early August, making my tongue-in-cheek call for an auspicious 8% weakening of the currency ahead of the Chinese New Year celebrations in early February look increasingly possible.

It was only in December that China announced they would be moving toward a basket of currencies to benchmark the CNY against, and the cynics among us believed it to be a good excuse for a more dramatic weakening of the currency than might be otherwise expected. Unfortunately, in the Chinese foreign exchange world, cynicism has a strong track record, and the currency really does look to be on track for a major weakening move over the coming months, irrespective of what the Fed does. Odds look likely that 2016 will see the CNY trading at the 6.83 level where it traded consistently for a two-year period from 2008-2010. This would entail about a further 3% easing in the CNH and a 4.7% easing in the CNY from where they are currently trading.

ASX

The ASX has had a pretty miserable day as it played catch up to yesterday’s major global selloff. Considering it managed to hold up far better than most markets yesterday, its underperformance compared to the rest of Asia today was not overly surprising. Today’s over 1% loss on the index was a textbook market risk move, with only 24 companies moving up on the day. The selling was wide-spread with all major sectors in the red.

The concerns China sparked yesterday with its PMI miss and market selloff hit commodities fairly hard overnight setting up a fairly poor performance for both the materials and energy sectors. The only exception to the rule were gold mining stocks, which rallied on safe-haven buying for gold.

But the real bellwether of the index, the banking sector, held no respite for the ASX today with major selling amongst the Big Five, and financials as a whole lost 1.5%.

Surprisingly though, bar the energy sector, the healthcare sector was the worst performing on the index, losing over 2%. Blackmores, Sirtex and Virtus all stood out, losing more than 4%.

And to cap off a bad day on the ASX, Dick Smith went into receivership. Conversely, this news was taken as a positive for its top competitors JBH, which gained 2.2%, and HVN , which still lost 0.2% but far less than most other stocks on the index today.