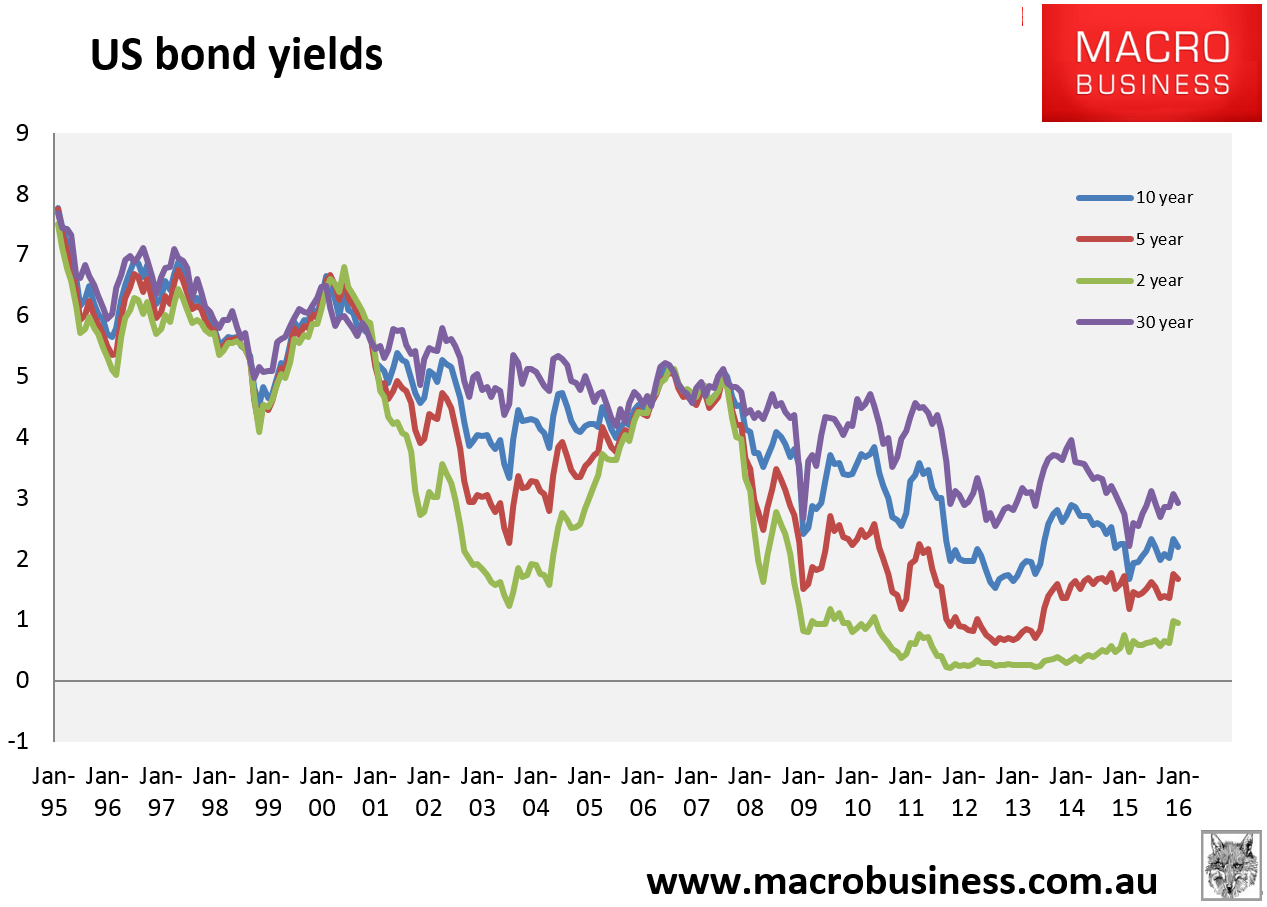

I’ve noted recently, the increasing divergence in the US bond markets between short end and long end yields. Basically, while the 2 year yield is rising on FOMC rate hikes and hopes for rebounding growth and inflation, the 10 year and 30 year yields are still caught in large downtrends, suggesting the opposite:

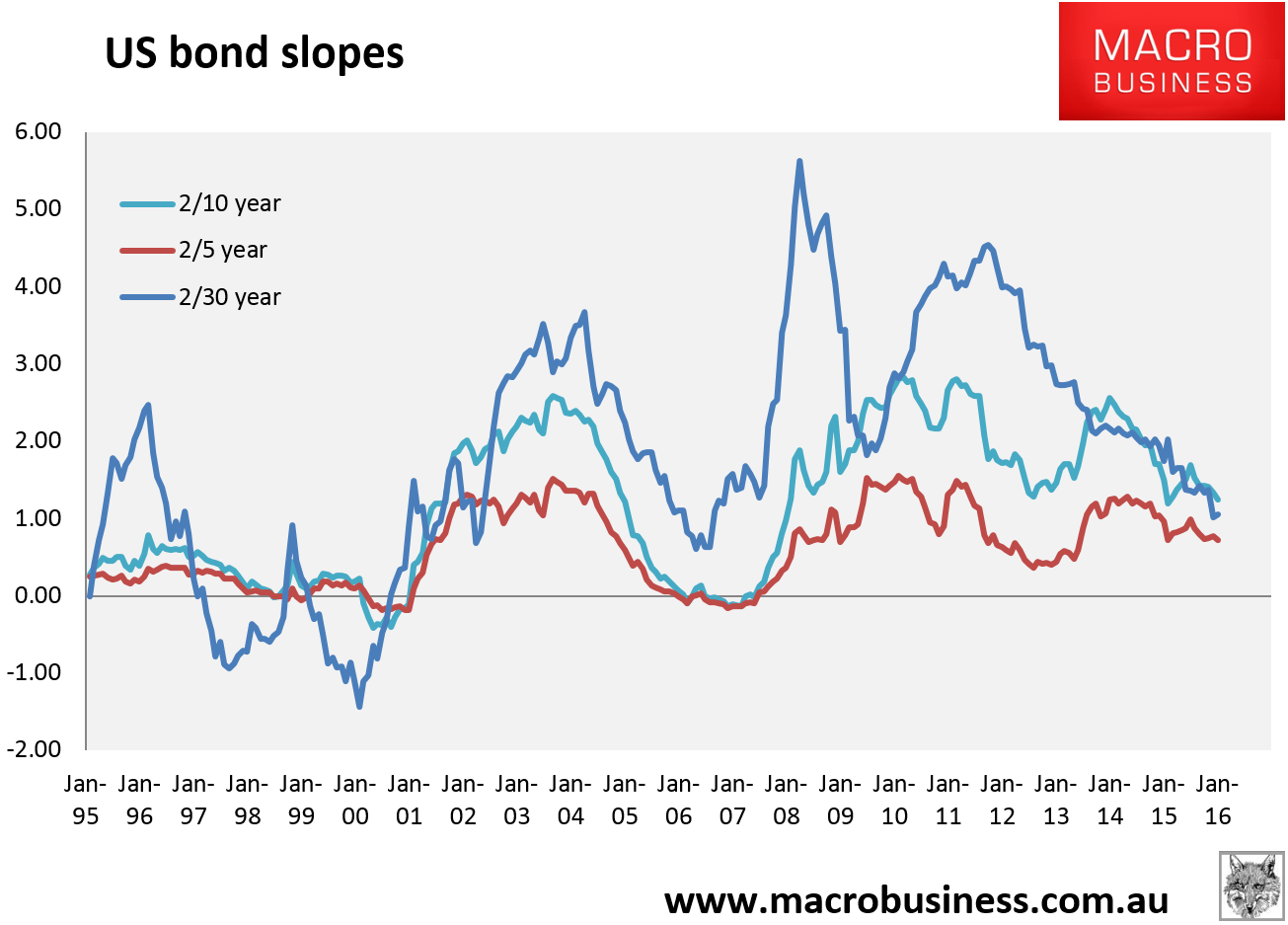

That is showing up in what is called “curve flattening”, which is a signal for weakening growth:

Advertisement

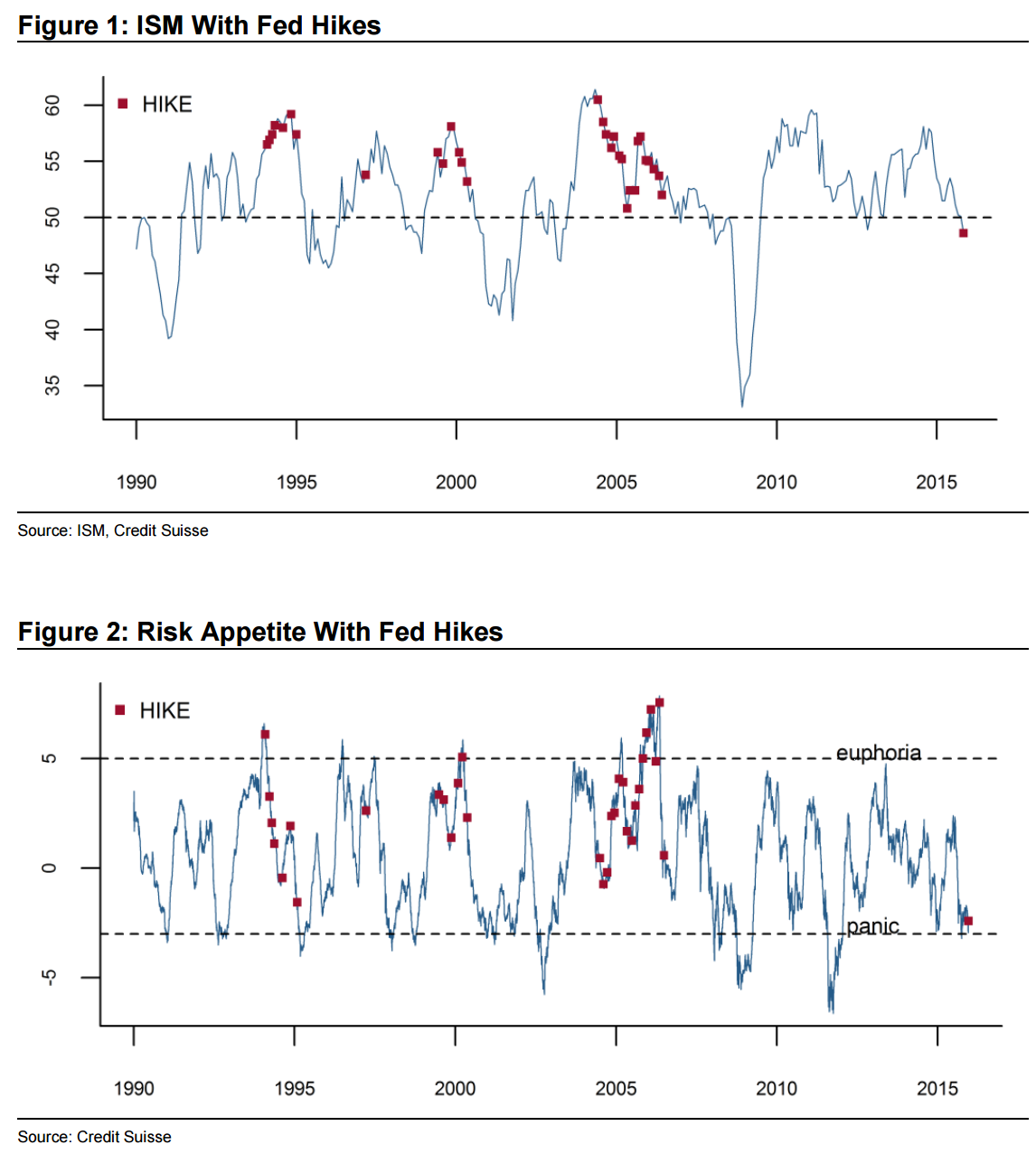

I’ve often described why MB sees the commodity and emerging markets crash as key fallout in the FOMC tightening but Credit Suisse has a nice chart showing why markets might also find US conditions concerning versus previous cycles: