Total employment lifted 58.3k in October, it was originally estimated to have risen 58.6k pre the population benchmark revisions. In October, total employment has now grown 307.1k or 2.7%yr. The original estimate was 315k or 2.7%yr.

Either way this represents a significant acceleration from the 2.0%yr in September and does far too strong compared to other labour market indicators.

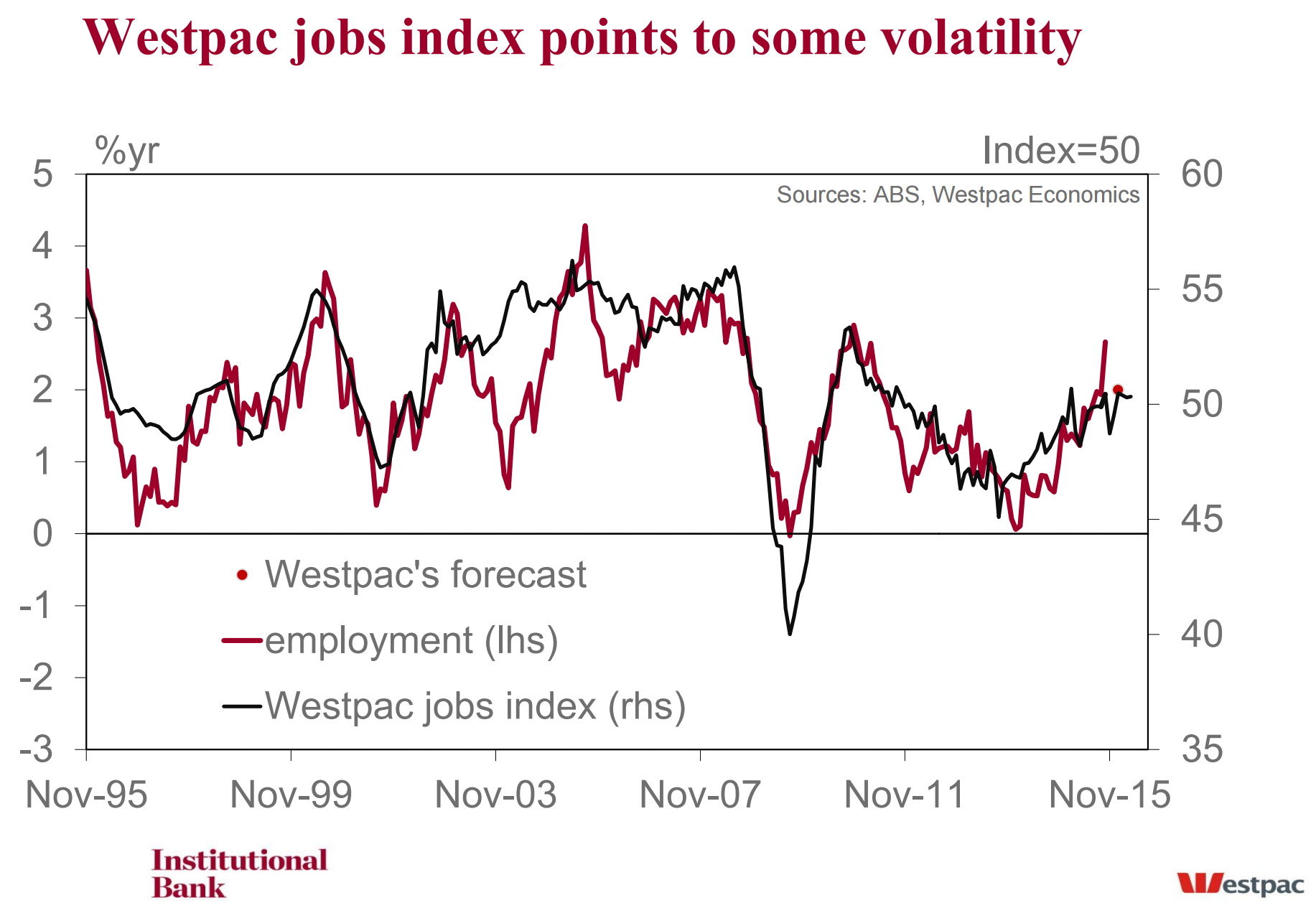

Westpac’s Jobs Index continues to point to annual employment growth of around 2%yr.

• We also note that the October survey reported a 92.7k rise in total employment in original terms when historically October printed significant negatives. You have to go back to 1979 to find a small positive for October. • Readers may remember that the ABS has changed the supplementary surveys in the February and August Labour Force surveys. These changes were behind the volatility in the August 2014 survey which has since been revised away.

• What has not been revised away is the volatility in the underlying original data. Prior to 2014 there was a significant August fall in original terms which was followed by a significant rebound in September then a meaningful negative in October. In 2014, with changes to the supplementary surveys, the original August data printed a modest rise while the September survey reported a modest fall and October printed a small rise. Something very odd is going on in the underlying original data 3

• This year, August returned to being a negative and September reverted to a positive though both are of a smaller magnitude than the past (particularly the September rise). More surprising was the 92.7k rise in original employment this October, something that is unprecedented in the data. In fact excluding 2014 you have to go all the way back to October 1979 to find a rise in original terms and even then it was a very modest +6.3k. Significant changes have occurred to the original data in October.

• You can also compare the monthly change in the seasonal factors and see that the ABS has modify the seasonal adjustment process to take the August & September changes into account. Historically the seasonal factors suggest a seasonal impact of around –1.0% in August, almost +1.5% in September and then –0.5% in October. However, in 2014 the seasonal factor was just +0.3% in August, then –0.3% in September. This year, the factors have been reversed with a –0.6% fall in August and a 0.6% rise in September

• This year there was something very odd about the October employment seasonal adjustment. In 2012 the change in the October seasonal factor was –0.4%, –0.3% in 2013 then +0.3% in 2014 and in 2015 it was again +0.3%. As such, the seasonal factor was a very modest offset for what was a very significant underlying bump. Our forecast is based on employment falling in line with our jobs indicator 4 • Normally you have to have to wait 3 to 5 years for the seasonal factors to settle down before you can estimate such significant changes to the seasonal adjustment process. Clearly the ABS is taking other factors (such as estimates of the impact of changing the supplementary surveys) into the seasonal adjustment process in August and September but has been less inclined to do so for October.

• As such, we have to take it on face value that the ABS will leave the October seasonal factor unrevised and so leave the November factor as is. In original terms we note the November printed –28.2k in 2012, –36.7k in 2013 then a surprise +30.3k in 2014.

• Given these survey issues Westpac is forecasting –20k in total employment in November as we are looking for something of a statistical. But we do not that using November 2014 seasonal factor this translated to –41.6k in original terms, the weakest November print since –50.1 in November 2008. Just as critical is that the –20k takes the annual pace down to 2.0%yr which is consistent with our jobs index.

• The 58.3k rise in total employment in October was associated with a solid 0.1ppt rise in participation. We expect participation to fall a bit in November which will limit the rise in the unemployment rate to 1ppt to 6.0%.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.