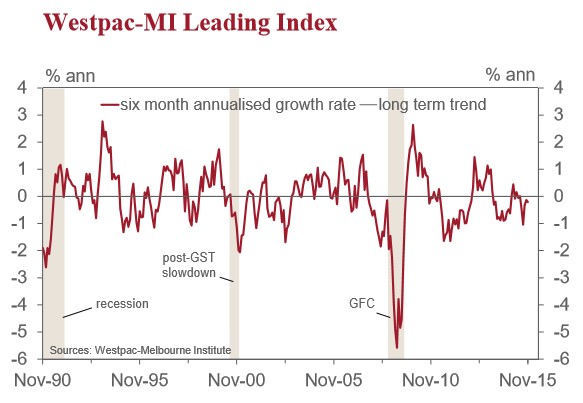

The Westpac-Melbourne Institute today released its Leading Index for November, which indicates the likely pace of economic activity three to nine months into the future.

The Index retraced from minus 0.13% in October to minus 0.21% in November, with growth in the index running below trend for the last five months.

Bill Evans is disappointed, and believes that real GDP growth could undershoot trend (2.75%) in 1H 2016, with the leading index more bearish that both Westpac’s and the RBA’s forecasts:

This result is a little disappointing. In the two previous months we had seen some modest improvement in the growth rate raising hopes that growth in the Leading Index might exceed trend by year’s end. Unfortunately, the set-back in this result leads us to the more general conclusion that growth in the Leading Index remains stuck below trend. The growth rate has now been below trend for the last five months. That is indicating that growth in the Australian economy in the first half of 2016 will be below trend.

Recall that both Treasury and the Reserve Bank are now assessing trend (or potential) growth at 2.75%. Westpac’s current forecast for 2016 entails an annual growth pace in the first half of 2016 of 2.75% (trend). The signal from the Leading Index indicates that our forecast may be somewhat optimistic.

It is not possible to exactly assess the 2016 (H1) growth forecast implied in the government’s MYEFO Statement which was released yesterday but we can confirm that the government’s near term growth forecasts (2015/16 and 2016/17) are slightly weaker than our own forecasts after the government’s forecasts were revised down from the May Budget.

In the Budget the government forecast growth of 2.75% in 2015/16 and 3.25% in 2016/17. These forecasts have now been revised back to 2.5% and 2.75% respectively.

Westpac is expecting growth of 2.8% in 2015/16 and 2.7% in 2016/17.

The Reserve Bank has slightly different forecasts of 2.25% for 2015/16 and 2.5%–3.5% in 2016/17. Using the mid-point of the Bank’s forecast range we can see a slightly more cautious outlook in the near term but more optimistic outlook further out than the Westpac and Government forecasts. The Reserve Bank does provide sufficient information to impute their forecast for the first half of 2016 with a trend pace of around 2.75% implied – the same as Westpac.

In summary it appears that the signal from the Leading Index is slightly more down beat on growth in the first half of next year than the RBA and Westpac. This signal will warrant further scrutiny over the next few months.

Over the last six months growth in the Index has slowed from 0.01% above trend to 0.21% below trend.

Components of the Index which have contributed to the slowdown are: ASX 200 (–0.38 percentage points); dwelling approvals (–0.13 ppt’s); yield spread (–0.37 ppt’s); and aggregate monthly hours worked (–0.17 ppt’s).

Partly offsetting these negatives have been: Westpac-MI Consumer Sentiment (Expectations) (0.20 ppt’s); US Industrial Production (0.36 ppt’s); RBA Commodity Price Index (0.14 ppt’s) and Westpac MI Unemployment Expectations Index (0.15 ppt’s).

Recall that the yield spread is capturing the shape of the yield curve. A larger increase in short rates relative to long rates indicates that bond markets are anticipating a slowdown.

The Reserve Bank board meets next on February 2. Since the last rate cut in May this year Westpac has assessed that rates will be on hold throughout 2015 and 2016. We have seen no reason to change that view but do recognise that risks to the view are to the downside. The key dynamic that would be responsible for a need for lower rates would be the impact of falling terms of trade on incomes and spending.

With further falls in the household savings rate; an expected sub USD 0.70 Australian dollar; and ongoing solid employment growth that prospect seems unlikely

With the triple shocks of falling mining investment, falling housing (both and construction and prices), and the car industry’s closure very likely to hit the economy in tandem in 2016-17, along with the ongoing slide in commodity prices (terms-of-trade), the next movement in interest rates is very likely to be down.