The Mid-Year Economic and Fiscal Outlook (MYEFO) has been released, and as expected it stinks.

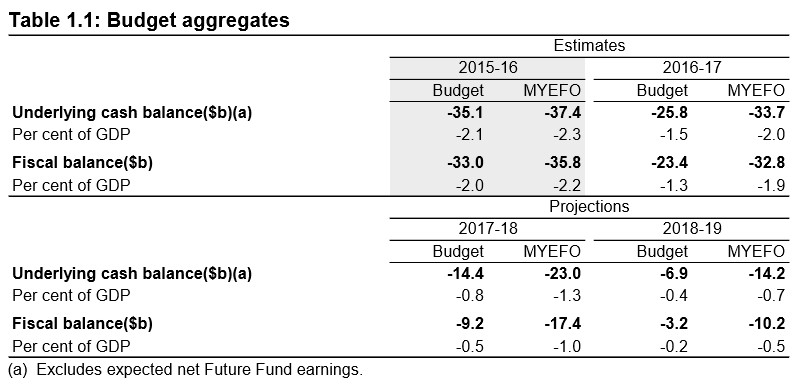

The key Budget outcomes are shown in the below table, which shows the aggregates against the May Budget. As you can see, there has been a sharp deterioration in the Budget over the forward estimates:

As shown above, the forecast federal budget deficit has deteriorated by $2.3 billion since the May Budget, with deficits also forecast to be $23.8 billion worse over the three years from 2016-17.

Advertisement