Catching up to yesterday, from Citi on its 65% probability call for recession next year in the US:

In the US our chief concern is margin sustainability. Corporate profits as a share of GDP have been at all-time highs, which is just another way of saying the rewards to labour have been at all-time lows. But change may be afoot in the form of modest labour market tightening in the US. It is too soon to see this show up in core (ex Fins, Energy and Materials) margins in the US (Figure 13, LHS) but that may be where things go. Modest nominal wage acceleration combined with global disinflation (price taking by US firms) and lack of productivity growth may mean margins come under pressure from labour costs.

US business surveys increasingly seem to be highlighting labour costs as a factor affecting future prices (Figure 14, LHS). Non-labour related costs don’t seem problem for businesses, which stands to reason given commodity price trends. It is also true that 2014/15 optimism regarding sales and margins seems to have waned (Figure 14, RHS), quite materially so in the case of sales.

Given the surge back towards the all-time highs in the S&P 500, we think that the best might be over for US equities and that indices might range trade more in 2016.We have downgraded US equities to neutral. This takes our overall equity weighting down to neutral, in many respects an extension of what we’ve been doing for most of this year as richer and richer asset markets, against a global background of economic risks, have made us more cautious.

If this were a typical policy cycle after a typical economic cycle, the Fed would have already raised rates 2-3 years ago. Instead, the US recovery is set to enter its seventh year while the European recovery is still embryonic. So in addition to China sneezing, FI markets need to price the longevity of the cycle. There are two approaches.

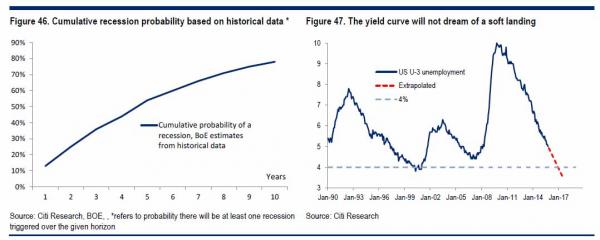

1. Cycle probabilities

Firstly, a statistical approach is shown in Figure 46 and highlights the cumulative probability of a recession based on data from 1970-14 across US, UK, Germany and Japan. As the U.S. economy enters year seven, the cumulative probability of a recession in the next year rises to 65%.

2. The economy continues to expand

That would take the US U-3 unemployment below 4% by end 2016. Unless, there is a soft landing, the market will price both front end hikes but also a major flattening of the curve, to augur higher recession risk. Watch for flat forwards initially and then some inversion quicker than consensus prices.

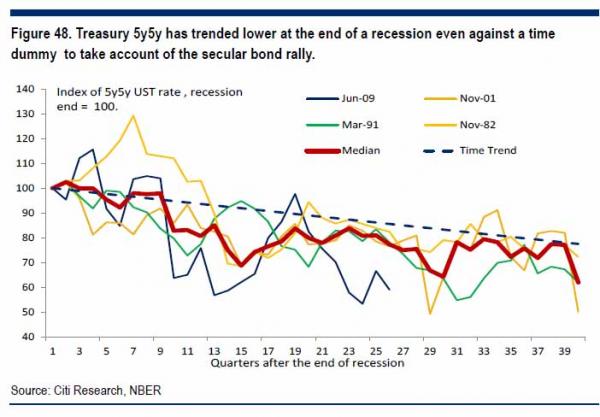

The median line shows that even against a time trend to account for the secular bond market rally that 5y5y Treasury yields move lower.

So, the Citi position appears to be a more traditional assessment of the business cycle as more income is seized by labour over capital and rates as margins fall then stocks get routed.

Fair enough but my view is that the global commodities and emerging markets crash will derail the cycle first!

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.