The ECB disappointed markets last night after its latest easing proved more bark than bite:

At today’s meeting the Governing Council of the ECB decided that the interest rate on the deposit facility will be decreased by 10 basis points to -0.30%, with effect from 9 December 2015.

The interest rate on the main refinancing operations and the interest rate on the marginal lending facility will remain unchanged at 0.05% and 0.30% respectively.

Further monetary policy measures will be communicated by the President of the ECB at a press conference starting at 14:30 CET today.

Wall St was not impressed. From Deutsche Bank:

Our premise of continued bearishness on EUR/USD through the end of the year was a “full” delivery from both the Fed and the ECB. The latter leg was a significant disappointment today versus our expectation and we therefore close out the EUR/USD shorts we initiated in our September FX Blueprint. We are keeping all our official 2015-2017 year-end forecasts unchanged.

RBS:

The ECB’s credibility to reach CPI target at risk after today. ECB has missed CPI target by more than 1% for 25 mos. in a row and nothing Draghi has done today convinces investors that the central bank is getting ahead of the curve, RBS strategist Michael Michaelides says in a Bloomberg interview. ECB is showing its clear deflationary bias. Consequences from today’s major disappointment may lead to a tightening in euro-area financial conditions. Market may reassess ECB’s willingness to do more soon compared with previous expectations.

BofA:

ECB President Draghi’s argument that more will be done if needed, is not enough given mkt’s high expectations and his past pattern of over-delivering, Athanasios Vamvakidis, strategist at BofAML, says in e-mailed comments. Expectations for today were just too high. ECB easing package is underwhelming, not aggressive enough and below expectations

And Citibank:

ECB’s package of easing measures is disappointing so far, as expectations had built up high in recent weeks, especially after Draghi’s speech on Nov. 20, Josh O’Byrne, FX strategist at Citigroup, says in e-mailed comments.

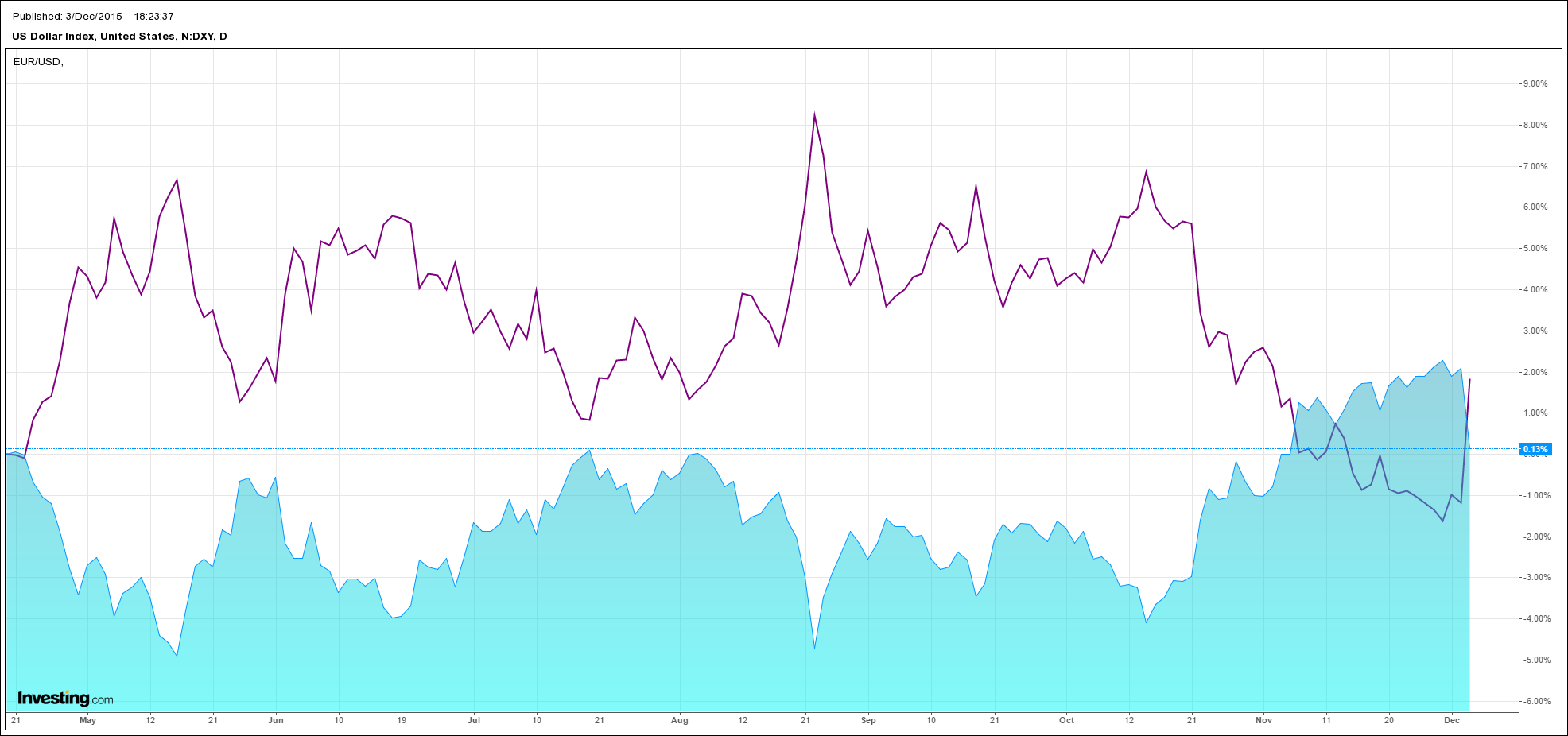

Markets were expecting more so the reaction was fierce. The US dollar index was hammered 2% as the euro surged:

That sent oil through the roof 4.7% though base metals lagged:

More importantly, an easing US dollar liberated bonds to fully embrace Fed tightening and everything was sold hard and yields surged across the curve:

Which did not impress stocks!

The Australian dollar took off as local bonds were also hammered.

This is not a trend break of any kind to my mind. Markets were simply overweight a perfect outcome (for them) of European easing and US tightening. The US dollar longs will be cleared and then we’ll begin again. Europe is still easing and the US is tightening even more as a result.