by Chris Becker

Ho ho hum. Except for the unexpected early release of the November personal consumption expenditure (PCE) report in the US, which showed increasing consumer spending amid zero inflationary pressures, it was same old Santa rally into the last session of the week overnight as US and European stocks surged. Even a dour OPEC report couldn’t keep oil down, with a short covering near 5% rally overnight highlighted by a planned year end drop in inventories. Its a confused message of course – higher US domestic demand as the USD remains elevated – while production glut continues apace. Bonds were relatively quiet although credit markets are picking up in volatility coming into the year end.

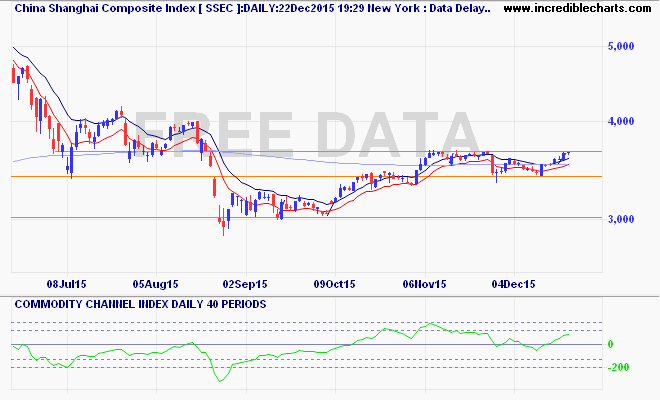

Recapping Asia’s session where the breakout in the Shanghai Composite with a slight selloff yesterday, down 0.4% to 3635 points, still below the former highs at 3670.