In this note, Ord Minnett analyses how the Australian market might react to the US Federal Reserve’s first step in tightening monetary policy and which stocks, sectors and themes investors should be focusing on. In addition, we have contemplated the impact a tightening cycle might have on commodities and whether it will go to script this time.

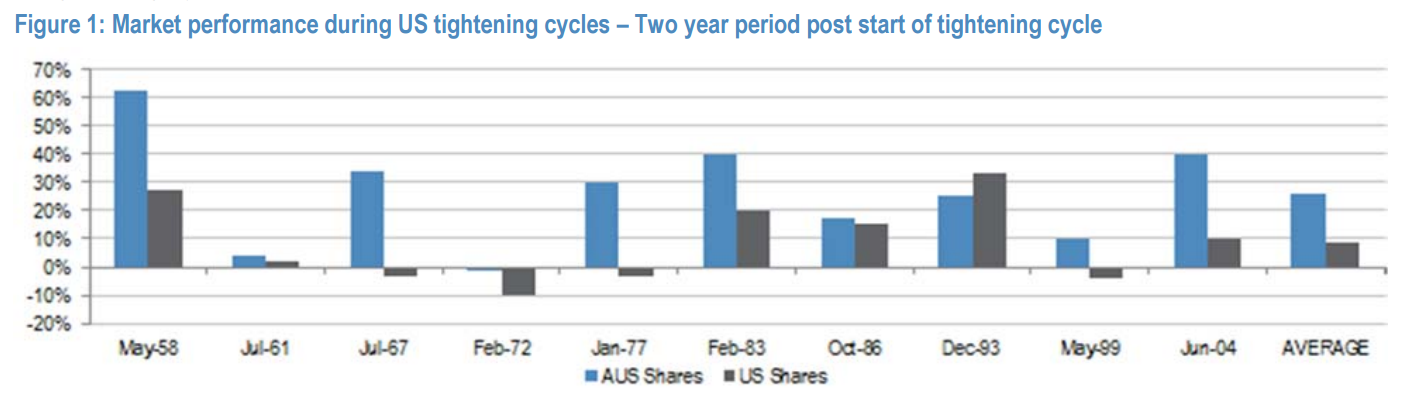

Australian market performance in US tightening cycles – Over the past 10 tightening cycles in the US, the Australian market has outperformed over the subsequent two years in all but one (see Figure 1).

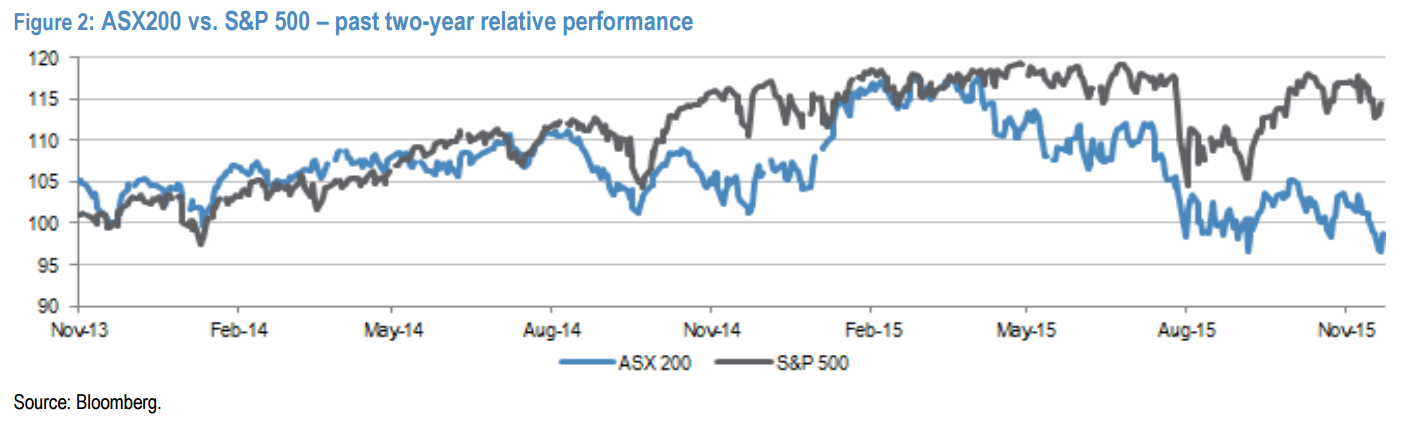

Relative performance – Over the past two years, the S&P/ASX 200 Index has been a dismal performer on the global stage. The underperformance against the US currently stands at 18 percentage points (see Figure 2). With our market trading on a one-year forward P/E that is 2.2 times lower than the S&P 500 and offering a yield that is 310 basis points higher at 5.1%, the argument for the S&P/ASX 200 Index to deliver a period of relative outperformance is compelling.

Well jeez, it is if you’re a quant with no wider frame of reference. But given Australian company earnings are much more attached to a fading Chinese business cycle these days perhaps the world of numbers is a little way behind reality. As for the dividend yield, it’s only as good as the earnings. Over the next few years yields will come under a lot pressure as banks follow miners with cuts.

Credit Suisse is similar to ORD:

Compelling relative valuation is now the main driver after underperformance throughout 2015. Although we are not positive on commodities we do believe they could be closer to stabilizing and this would provide a boost for Australia. During ongoing world economic growth US equities tend to lag and since they rose relative to global averages during recent volatility, we now move them down to Underperform.

CS also observes that SMSFs are long and getting longer:

Advertisement

“Selfies [SMSFs] have had a horrid time in Aussie equities this year and have endured a capital loss of a combined $40 billion in the June and September quarters,” Credit Suisse equity strategist Hasan Tevfik wrote in a research note.

However SMSFs by nature are very concentrated in their investments, concentrated in just three assets, shares, cash and property. Low yields in both cash and property mean equities are still favoured for their relatively higher yields, and reinforcing the local sharemarket as a play on yield. Around 39 per cent of a SMSF portfolio is weighted in equities, Credit Suisse estimates.

If SMSFs are targeting yield then they’re in for a bad few years ahead.

Advertisement

UBS does a better job but only half:

2015 Looked A Lot Like 2014 – What Chance Another Macro Repeat in 2016?

While 2015 was not an exact carbon copy of 2014, many of the key drivers and broad sector performance were remarkably similar. Weak commodity prices, a falling A$, low and relatively stable interest rates, lacklustre market earnings growth and lacklustre headline market performance were all once again key elements for 2015, as they were in 2014. With the Fed tightening cycle having now kicked off we may well see some new drivers at play. Higher bond yields are arguably the most obvious tail risk, though the UBS central case is for the rise in yields to be relatively constrained.

No EPS Growth At Headline Level – Better Ex Resources, Better Still ex-Banks Aggregate market EPS growth is currently -4.3% for FY15 and -0.9% for FY16.

The weaker earnings growth picture is being driven heavily by falling earnings in the resource sector and to a lesser extent by sluggish EPS growth in the bank sector. The market ex banks and ex resources EPS growth is a more respectable 8.9% for FY15 and 5.9% for FY16. The median stock EPS growth for FY15 is 10% and for FY16 is 5%.

Sector Preferences Going Into 2016

We remain underweight mining and overweight banks and overweight US$ earners. We are overweight domestic cyclicals (the market is too bearish on the economy in our view). We are attracted to a short list of GARP stocks (often with a US$ earning angle) and we are underweight consumer staples and telcos.

Spot on for avoiding miners and being long US-dollar earners though I would still be selling rallies in the latter based upon the notion that the Mining GFC is advancing and looking ominous for an end of cycle event within twelve months and that will hit US shares (and therefore all others) hard when the penny drops presenting a great entry opportunity. The market is not too bearish on the local economy. It is too bullish given the position of rate hikes priced into bond markets. Authorities are clearly going to aim to keep the consumer spending into the bust but when adjusted for risk, cyclical stocks are a big, fat sell, or short on the rallies.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.