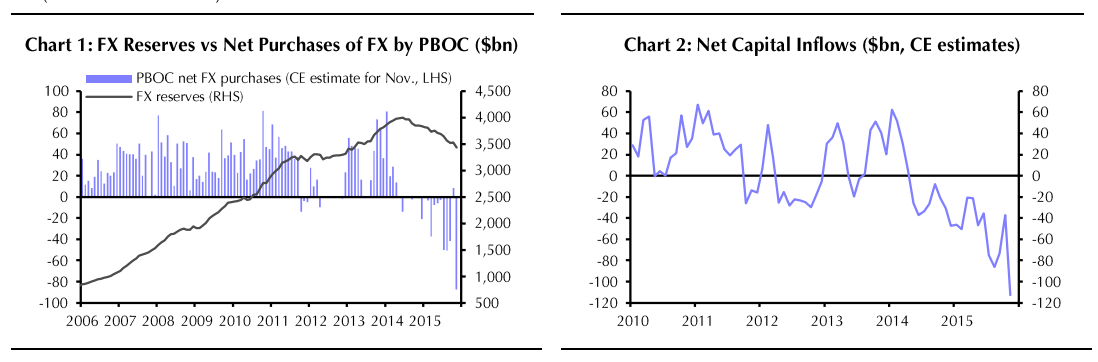

Today’s FX reserves data suggest that capital outflows picked up sharply last month, leading the People’s Bank (PBOC) to resume selling FX in order to prop up the value of the renminbi.

The value of China’s FX reserves stood at $3.438tn at the end of November (the Bloomberg median was $3.493tn, our forecast was $3.475tn), a decrease of $87bn from a month earlier. Our calculations suggest that exchange rate fluctuations will have reduced the dollar value of the portion of the reserves held in other currencies by around $30bn. This points to PBOC FX sales of $57bn last month. Since we expect the combined goods and services trade surplus to have been around $55bn last month, this would imply record net capital outflows of $113bn, up from outflows of $37bn in October.

The pick-up in capital outflows appears to have been predominately driven by increased expectations for renminbi depreciation.

And Nomura:

Overall, we continue to forecast an extremely challenging flow backdrop for China into 2016, where the risk is for more periods of net capital outflows. This is based on a number of factors, from Nomura Economics’ view of a substantial slowdown in China growth (5.8% versus Bloomberg consensus of 6.5%) and the risk of further rate cuts (versus Fed hikes), to questions over multi-market intervention and the government’s anti-corruption push. Medium-term structural capital outflows from the private sector as reflected in the significant gap between China’s net international investment position (IIP) and that of the public sector (FX reserves) should also sustain upward pressure on USD/RMB … This compares with our view of limited capital inflows, where the trade surplus-related USD selling flow could be smaller than expected due to the hoarding of USD by corporates. In addition, we believe global diversification into RMB assets should be moderate as investors may exercise caution due to concerns over China’s economy and financial market valuations.

Correct! I do believe that the tipping point is passed…

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.