According to the bank, “the updated output is consistent with near-term liftoff of the fed funds rate, with a risk toward a later liftoff should further softness in inflation manifest. The model now shows much less assumed cyclical slack in the economy and has a softer path of inflation, highlighting the FOMC’s current dilemma as the two parts of their objective move in opposite directions.”

Barclays ran the FRB/IS model using the most recent data, and had the following additional take-aways:

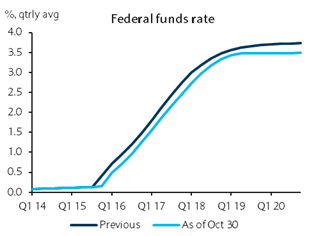

Figure 1: The fed funds rate: FRB/US now assumes that the FOMC increases the fed funds rate in late 2015. We see this lift off as consistent with a December rate hike. Of note, FRB/US, like all other state space or DSGE models of the economy, calls for an immediate and rapid liftoff of policy rates. This immediate lift off has been a feature of FRB/US output since late 2014. The models see most variables as close to their long-run levels and hence the model calls for a return of interest rates to their long-run level (in other words, models do not take into account latent headwinds such as financial frictions or credit constraints in the economy).

Of note, all variables in the model must converge to long-run levels imposed by staff. At least in the assumptions used for this public version of FRB/US, the staff sees the long-run level of the funds rate at 3.5%, down 25bp from their previous release. This estimate is still higher than our belief (3.0 to 3.25%) but has gradually converged toward our estimate. The staff’s current assumption is down from the 4% level assumed by the Board as recently as late last year.

Figure 1: Funds path consistent with December

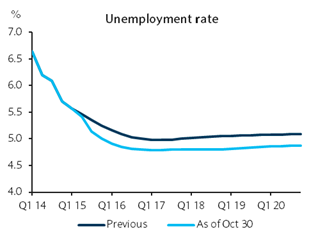

Figure 2: The unemployment rate: The staff moved the long-run level of the unemployment rate (NAIRU) lower in the October 30 release of the model. At 4.9%, NAIRU is two-tenths lower than in the previous version of the model. The lower level of NAIRU is consistent with the views of the committee as expressed in the SEP. The SEP shows the long-run level of the unemployment rate at 4.9%. With unemployment currently at 5.1%, FRB/US assumes very little change in the unemployment rate over time. This view is quite different than ours. We forecast ongoing declines in the unemployment rate and see it reaching 4.3% by end 2016.

Not shown in the output of the model, the stability of the unemployment rate implies either an increase in the LFPR (labor force participation rate) or a sharp slowing in employment growth. According to our estimates holding LFPR constant, the level of employment growth that keeps the unemployment rate constant is 76k per month. Alternatively, an increase in LFPR of about 0.7pp would allow NAIRU to stabilize with employment growth near its recent average.

Figure 2: NAIRU pushed down to 4.9%

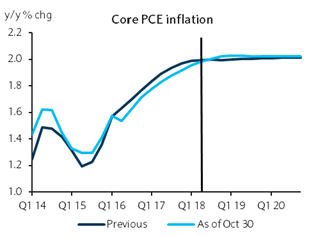

Figure 3: Core PCE inflation: The updated path for core PCE inflation closely matches our current forecast. In our forecast, the stabilization in oil prices should lead headline inflation to rebound early next year, but we look for recent dollar appreciation and ongoing declines in Chinese producer prices to lead to a moderation in tradable goods inflation through mid-2016. The release of September PCE inflation this morning is consistent with this view, as the sharp drag from goods prices (-3.2% y/y) led to an unchanged year-on-year rate of core inflation at 1.3%. The FRB/US model agrees and shows the firming in core inflation as giving way to a modest softening through mid-2016. As shown in Figure 3, the October 30 path shows a shallower path from Q1 16 through Q4 17 than the previous FRB/US update.

Figure 3: PCE inflation slightly lower

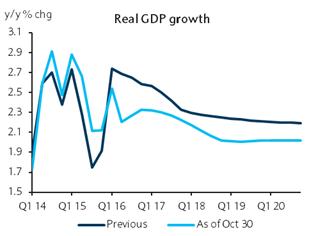

Figure 4: Real GDP growth: The October 30 update for FRBUS also shows a slower growth profile after this year and a lower long-run potential growth rate. As shown in Figure 4, the updated path has y/y rates of economic growth gradually slowing from 2.5% in Q1 16 to 2.1% in 2020. Based on FOMC communications, including minutes to recent FOMC meetings, we believe the shallower growth path likely reflects greater assumed dollar appreciation. In addition, the long-run growth rate is two-tenths lower than the previous FRB/US update (2.1% now versus 2.3% previously). Since this growth rate at the end of the horizon is imposed by staff, we interpret this as suggesting staff has likely reduced its estimate of potential growth, as did FOMC participants in the September forecast round.

Our view of potential growth is more pessimistic at about 1.5%, but our estimate is weighted heavily to current trends and is not equivalent to the Fed’s long-run estimate. Board staff have likely assumed that productivity growth, which has been much slower in the post-recession environment, rebounds over time as headwinds to the US economy dissipate. We do not discount this possibility, but leave this as an open question for the data to resolve over time.

Figure 4: Real GDP growth slows after this year

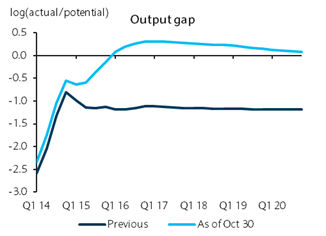

And the most important chart: The output gap: Board staff now see the output gap as closing by Q1 2016. To achieve this closing especially given their mark down of real GDP growth, they sharply lowered their estimate of potential growth in 2015. This change likely has policy implications as it indicates a staff view that there is no longer substantive slack in the US economy.

Figure 5: Potential output slashed to close output gap despite slower growth profile

This kind of modelling is exactly what got the US economy into its current pickle. If you’re not going to look at the quality of growth – that is, is it driven by debt, by certain wild cat capital flow patterns, or something a little more sustainable – then how can you possibly anticipate when the economy is going to break with trend? The Fed’s cash rate curve modelling is particularly amusing. Imagine what that would do to the US consumer, the US dollar and emerging markets…

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.