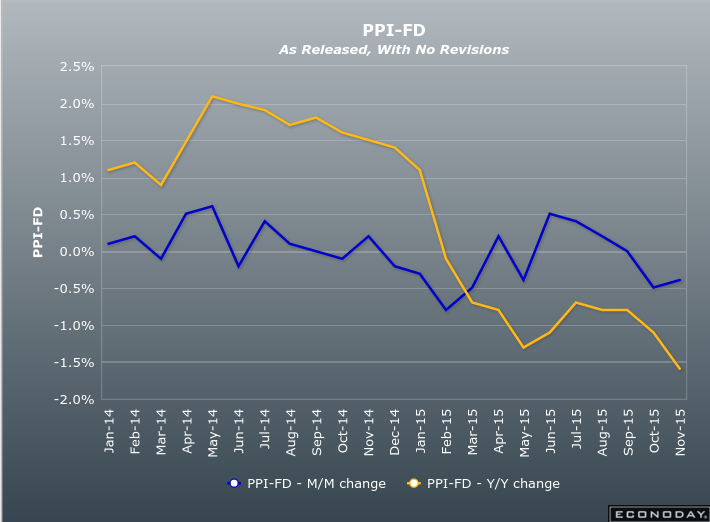

The US released its third quarter producer prices Friday night and boy was it soft, from the BEA:

The Producer Price Index for final demand decreased 0.4 percent in October, seasonally adjusted, the U.S. Bureau of Labor Statistics reported today. Final demand prices moved down 0.5 percent in September and were unchanged in August. On an unadjusted basis, the final demand index fell 1.6 percent for the 12 months ended in October, a record 12-month decline for this index, which was introduced in November 2009.

In October, 70 percent of the decrease in the final demand index can be traced to prices for final demand services, which moved down 0.3 percent. The index for final demand goods declined 0.4 percent.

Within intermediate demand, prices for processed goods fell 0.4 percent, the index for unprocessed goods was unchanged, and prices for services decreased 0.4 percent.

Expected was 0.2 so it was an huge miss. Year on year deflation is deepening:

This is obviously an oil story and if oil were to stabilise then the PPI would lift by mid next year. The problem is it is not stabilising and as the Fed hikes it’s going to get worse not better.

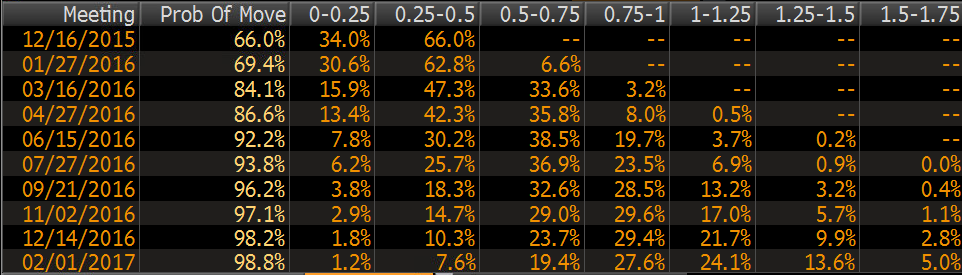

Even so, I do not think that the Fed can pause now. It has painted itself into a corner and will look like a complete fool if it squibs it again. That’s how OIS markets still see it:

But it does show three things.

First, the rate of ascent in US interest rates is going to be defined by its slowness not speed as the charging US dollar keeps pressure on commodity prices not least oil.

Second, the oil price is going to remain under pressure for longer than many expect.

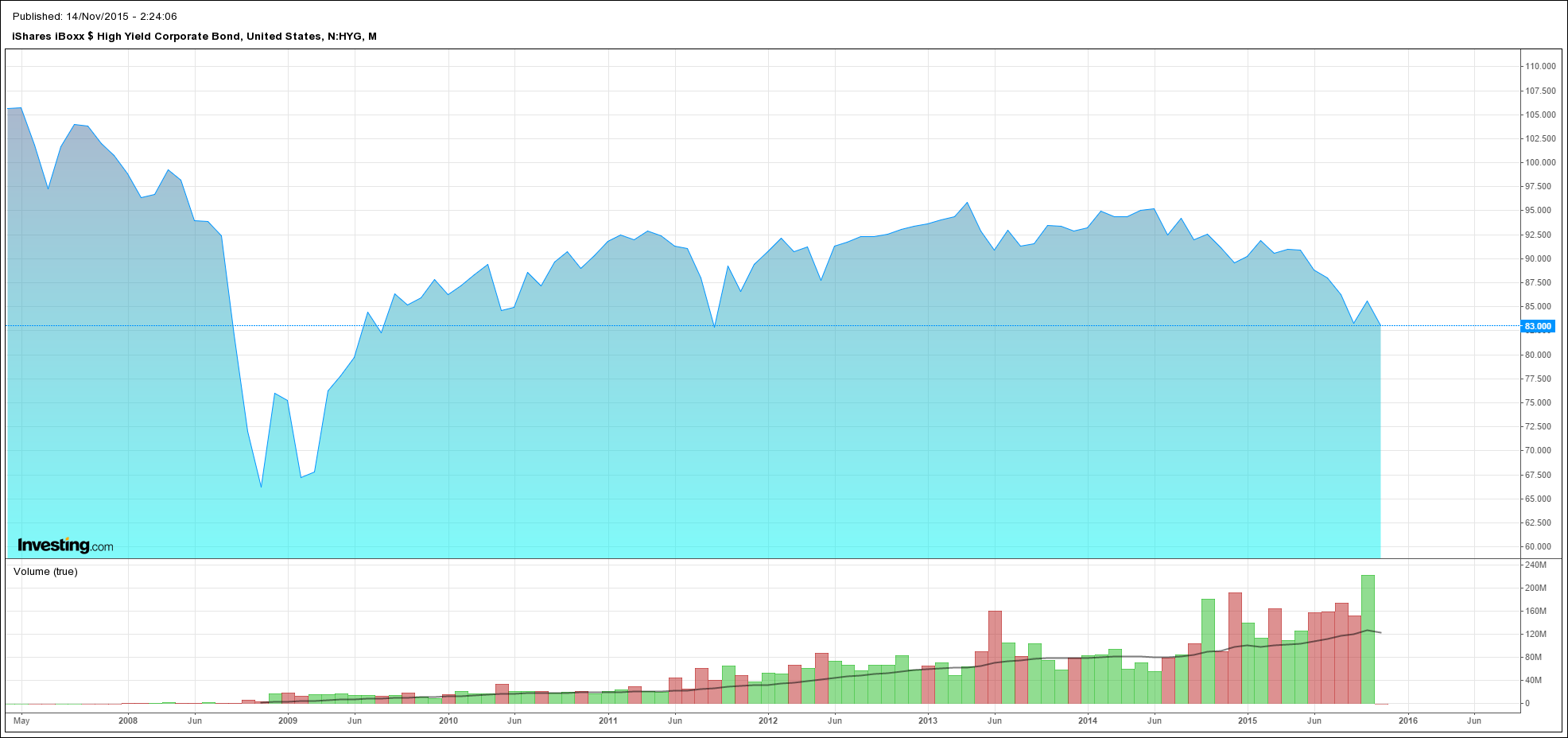

Third, the combination of rising US interest rates, a bullish US dollar and falling oil remains a toxic one for emerging market oil producers and may prove so destructive that it will not end until a debt reckoning finally cleans out oil supply. US high yield credit, which is decent proxy for energy debt, is threatening European crisis lows:

It sure is a bizarre set up with credit in clear distress at the margin yet rate hikes imminent. Even more strange, if the credit distress does mushroom and succeeds in choking off US shale oil production then inflation could actually rise as the oil market recovers some supply balance, leading to more rate hikes.

Whether that is possible before debt contagion spreads to other emerging market and commodity debt is, of course, the trillion dollar question.

Either way, the Fed appears now committed.