ABC’s The Business last night ran an excellent segment (above) examining upcoming changes to global bank capital rules that are to be released at the end of the year by the Basel Committee on Banking Supervision.

According to the segment, there are likely to be big changes to the way that banks calculate the capital held against their exposures, which are aimed at improving financial system stability.

The United States is leading a group that is lobbying for an end to the Internal Ratings-Based (IRB) approach, which allows certain larger banks to use their own internal models to calculate their capital held against exposures, preferring instead some type of leverage ratio. The United States claims that it doesn’t trust the IRB models, and believes that they contributed to the financial instability experienced during the GFC.

If the US gets its way and is successful in jettisoning the IRB approach, it would deal a massive blow to Australia’s big four banks and Macquarie, who have used their IRB models to reduce the capital held against their mortgages to paper thin levels, in turn juicing the amount of mortgage lending and profits.

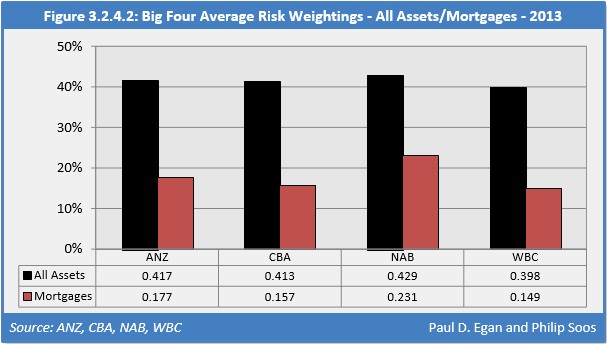

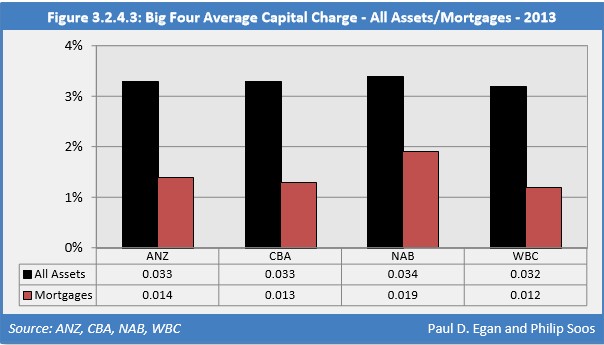

For example, in 2013, the big four banks’ capital charges on their total residential mortgage books ranged from only around 15% to 23%, with the average capital charge against mortgages a meager 1.2% to 1.9% (see below charts).

Accordingly, the big four banks have engaged in incredible levels of leverage – measured as the dollar value of equity divided by the dollar value of assets – averaging 22-times over the past two decades.

In its response to the Murray Financial System Inquiry, APRA has already announced that it will raise the average IRB mortgage risk weights to at least 25% from 1 July 2016, which has led to the major banks undertaking capital raisings to increase their capital levels.

The Government has also endorsed APRA introducing a leverage ratio to act as a backstop to ADIs’ risk-weighted capital positions.

So times are already changing.

What should become clear is that any reforms announced by the Basel Committee are likely to make the capital environment much tougher for Australia’s banks, and therefore Australia’s highly indebted mortgage holders.

The days of hyper loose capital requirements around mortgage lending and extreme leverage are coming to an end, which is yet another sign that the Great Australian Housing Bubble is on borrowed time.