The Chairman of the Basel Committee on Banking Supervision, Stefan Ingves, has signaled that rules governing the internal models used to calculate the capital requirements of the world’s biggest banks could be tightened as the global regulator prepares to release its latest proposed iterationions of the Basel Capital Accord – know as Basel 4 – at the end of the year. From The AFR:

“Ample evidence has accumulated to suggest that the current role of internal models in the regulatory framework does not strike the right balance between simplicity, comparability and risk sensitivity,” Mr Ingves said in a speech delivered in Spain on Monday.

Given the “common equity tier 1” (CET1) ratio – the key constraint in Australia – uses risk weighted assets to determine the level of capital, he said global regulators also want to measure banks using leverage ratios, large-exposure limits, the liquidity coverage ratio and the net stable funding ratio. “These constraints complement one another, resulting in a more robust regulatory framework,” he said.

The Australian Prudential Regulatory Authority (APRA) currently allows Australian authorised deposit-taking institutions (ADIs) – i.e. banks, building societies and credit unions – to use one of two approaches to determine their capital requirements.

Smaller ADIs – effectively everyone except the Big Four banks and Macquarie – are authorised to use APRA’s Standardised Approach to managing credit risk, which is summarised in the below table as it pertains to residential mortgages – the major loan item in Australia:

Whereas most lending to corporate borrowers is ascribed a 100% risk-weighting (i.e. an 8% capital charge), most residential mortgage lending is ascribed a risk-weight of just 35% (i.e. a 2.8% capital charge).

By contrast, the Big Four banks and Macquarie have to date gained a significant capital advantage by utilising APRA’s Advanced Internal Ratings-Based (IRB) approach, and therefore using their own internal models to calculate their capital held against mortgages.

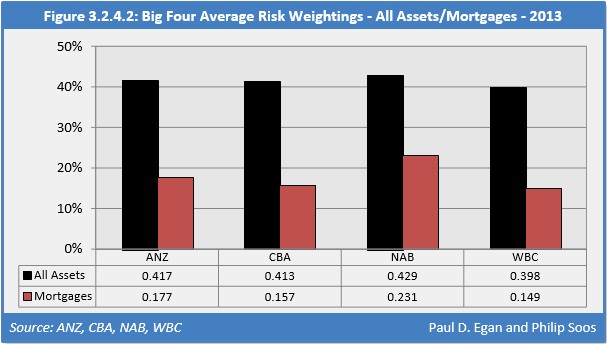

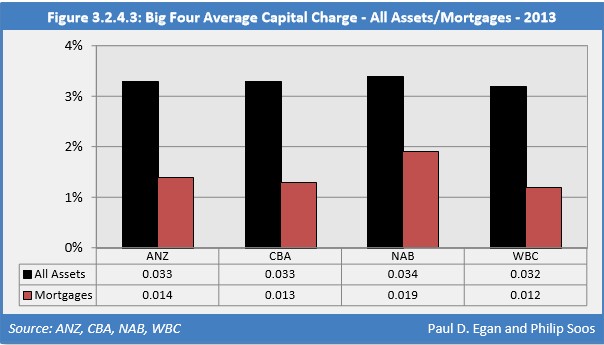

For example, under these IRB models, the Big Four’s capital charge on their total residential mortgage books range from only around 15% to 23%, with the average capital charge against mortgages a meager 1.2% to 1.9% (see below charts).

Times are already changing, however.

In its response to the Murray Financial System Inquiry, APRA has already announced that it will raise the average IRB mortgage risk weights to at least 25% from 1 July 2016, which has led to the major banks undertaking capital raisings to increase their capital levels.

The Government has also endorsed APRA introducing a leverage ratio to act as a backstop to ADIs’ risk-weighted capital positions.

The extent to which APRA would implement further tightening of bank capital in response to the Basel Committee’s recommendations remains to be seen but hey have already made clear that Australian banks must follow the international rules. There would also likely be long implementation timetables, which would lessen the adjustment.

Regardless, the days of hyper loose capital requirements around mortgage lending, and extreme leverage, are coming to an end, which is good news for those of us concerned about financial stability and excessive levels of housing lending.