Angus Nicholson for Chris Weston, Chief Market Strategist at IG Markets

Markets have been mulling over the recent Non-Farm Payrolls numbers all week, but the big selloff we have been seeing in the past 24 hours seems indicative that they have come to a conclusion…and they’re not happy about it.

A rate hike by the Fed in December seems almost palpable now, and markets are still scrambling to reposition themselves ahead of it.

However, China’s deeply concerning credit and monetary data released overnight does seem to have been the smoking gun behind last night’s renewed selloff in commodity markets. The far larger-than-expected oil inventory data reported by the EIA was the precipitating factor behind WTI oil’s drop below US$42. But the broad-based decline seen across a range of hard commodities can only point to renewed demand concerns fuelled by China’s dismal credit growth in October.

Total Social Financing (TSF), China’s broadest measure of credit, came in at only CNY 476.7 billion, its smallest amount since July 2014. New Yuan Loans came in at CNY 513.6 billion, also the smallest amount since July 2014. The weakness in the TSF number was driven by the weak new loan growth and impacted further by a major contraction in Bank Acceptance Bills. The bright spot was strong 13.5% year-on-year growth in M2 money supply and 14% in M1 money supply, which show evidence of China’s stepped up fiscal spending coming through in the data.

October is traditionally a weak month for credit in China with the Golden Week holiday upsetting the data and certain quarterly targets necessitating some of October’s loans being issued in September to meet the Q3 deadline. Nonetheless, the data was very weak and given the amount of monetary easing and increased fiscal spending we have seen in China over the past twelve months, it is concerning to see such a weak October number. The November data will be key in evaluating how transient the weakness in the figure is. Despite the weak figure, longer term trend metrics such annual growth (12 months-on-12 months) do point to a noticeable pick up in credit growth from the middle of this year. Given the weak figures it seems no surprise that the Chinese State media chose to disseminate Li Keqiang’s speech he gave recently in which he emphasised that China’s current 2.3% fiscal deficit leaves plenty of room to support the economy.

ASX – Some hard truths about an imminent reversal

The renewed selloff in commodities in the wake of that disappointing Chinese credit numbers did not augur well for the ASX today. BHP and RIO both had a terrible session on the FTSE overnight. The index was brought low again with the materials and energy sector leading the way. But telcos and consumer stocks also had a pretty disappointing day, with big falls by Metcash, Wesfarmers and TPG Telecom.

The bigger question for Australian investors is how far could the current renewed selloff go? With bellwether of the materials sector, BHP, opening below A$20 at its lowest level since 2009 some may be wondering if we are primed for a turnaround. And there are certainly a number of investors who think BHP is a screaming buy below $20. The unfortunate news is that based on a range of metrics on the ASX , the current selloff could well have quite a bit further to run.

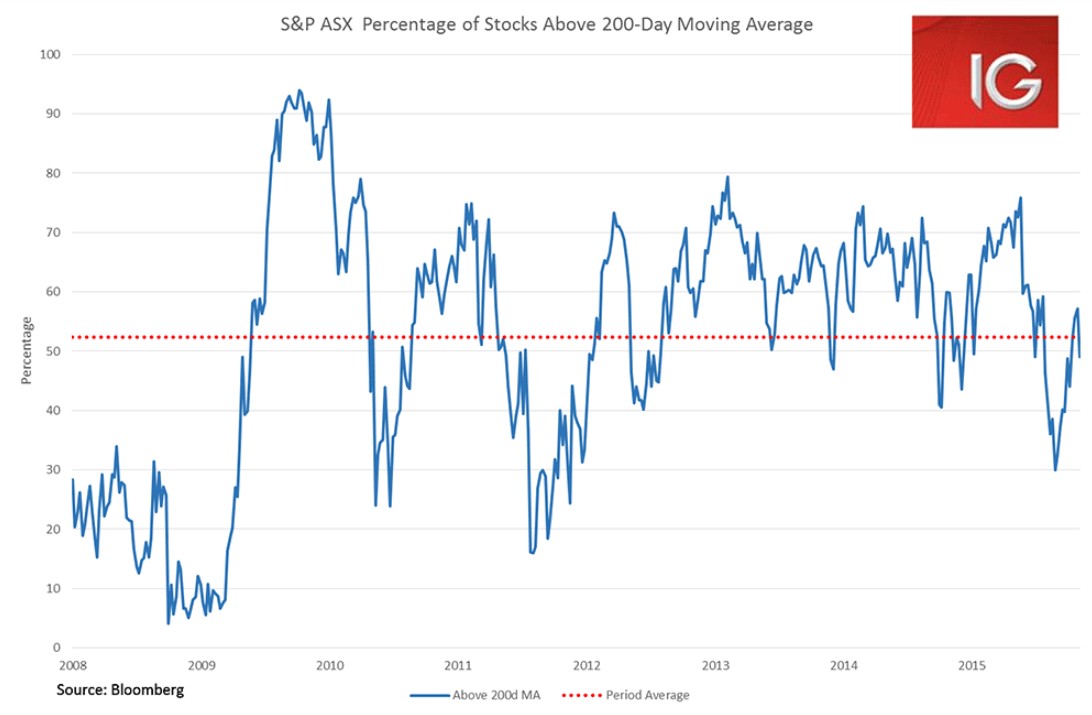

I would particularly point to the number of stocks trading above their 200-day moving average. Currently 49% of stocks are trading above their 50-day moving average, which is only slightly under the seven-year average of 52.4%. Unfortunately, in previous years it has not usually been until this metric moves below the 40% range that the ASX definitively moves into oversold territory and one could reliably argue the case for an imminent turnaround.

The other metric that looks like it has a fair bit further to run before it starts screaming oversold is the number of stocks trading at 52-week lows. Tuesday saw this metric jump up to nine, and one can clearly see it has been picking up in the wake of last month’s Fed meeting. But looking back over the past couple of years, it normally takes a reading of 20 or higher for this metric to really start showing that the market is oversold.

In short, this market is still a falling knife, so be very careful about jumping in trying to bottom pick stocks even if they are trading at seven-year lows.