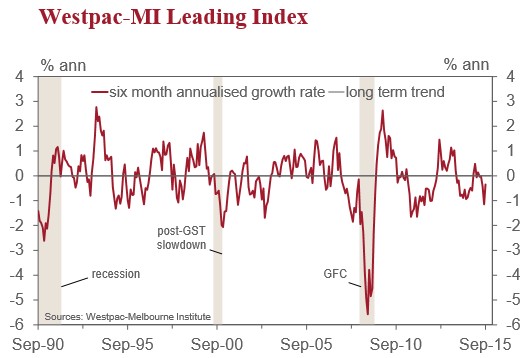

The Westpac-Melbourne Institute today released its Leading Index for September, which indicates the likely pace of economic activity three to nine months into the future.

The Index increased from minus 1.14 per cent in August to minus 0.35 per cent in September, with growth in the index running below trend for the last five months.

According to chief economist, Bill Evans:

This below trend growth profile is in line with our own views. Note that the June quarter national accounts confirmed that Australia’s six month annualised growth slowed to a 2.1% pace in the first half of 2015 with our forecast for the second half of a still below trend 2.5%. Looking further out we expect growth in 2016 of 2.75%.

With trend growth in the economy now likely to be nearer 2.75% than 3% our forecast for GDP growth in 2016 of around trend growth looks a little vulnerable based on this current run of below trend growth rates for the Leading Index. The Leading Index gives us a guide into the likely momentum in the economy through the final quarter of 2015 and into the first half of 2016.

Key factors behind our current expectation of a modest lift in the growth pace in 2016 are: a lift in consumer spending growth from 2.5% in 2015 to 3.0% in 2016; a modest improvement in non-mining investment and an increased contribution from net exports (adding 1.3ppts to GDP growth, up from 0.8ppts in 2015). These positive factors will be partly offset by a slowdown in dwelling investment from 10.0% to 2.2% as the residential building boom reaches its peak.

Over the last six months the six month annualised growth rate in the Leading Index has slowed from being 0.16% above trend to 0.35% below trend. The key components driving this slowdown have been: S&P/ASX 200 (–0.64ppts); dwelling approvals (–0.50ppts); the Westpac-MI Consumer Expectations Index (–0.06ppts); aggregate monthly hours worked (–0.05ppts); and US industrial production (–0.05ppts).

Partially offsetting these have been the yield curve (0.38ppts); commodity prices in AUD terms (0.23ppts) and the Westpac-MI Unemployment Expectations Index (0.21ppts).

The Reserve Bank Board next meets on November 3. We do not expect the Board to decide to cut rates.

The minutes from the October Board meeting emphasised that the Bank is comfortable with the outlook for the labour market and the apparent slowing in the housing market. It will take some time to assess the size and impact on the economy of any tightening in financial conditions that might be associated with independent increases in mortgage rates from banks.

However the Board did highlight the importance of the global outlook and seems to be more downbeat on China.

The risks to our current view that rates will remain on hold for the remainder of 2015 and 2016 are to the downside.

A rate cut in early next year would require the Bank to be forecasting growth in 2016 to be 2.5% or less without a policy response. The Leading Index is signalling a somewhat lower growth outlook in the first half of 2016 than our 2.75% and the RBA’s current forecast of 3% for the whole of 2016, pitching rate risks to the downside.

With the triple shocks of falling mining investment, falling housing (both and construction and prices), and the car industry’s closure very likely to hit the economy in 2016-17, it is inevitable that the RBA will be forced to cut rates. The only questions are when and by how much.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.