From Westpac’s Elliot Clarke comes a useful dissection of US GDP, which points to a robust underlying growth trend once inventories and net exports are stripped-out:

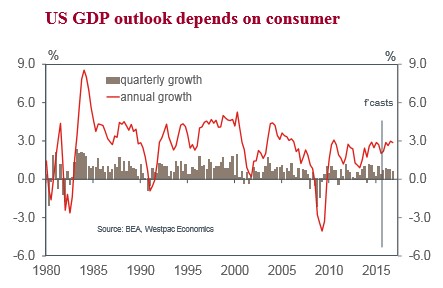

US GDP growth decelerated to a sub-trend pace in Q3 following a particularly robust Q2. Despite the 3.9% annualised gain recorded for Q2, Q3’s 1.5% increase together with Q1’s 0.6% result leaves average-annualised growth for 2015 at 2.0%, broadly in line with most estimates of trend growth. Despite the rapidly improving labour market, aggregate growth has been stuck around this pace since the beginning of 2011.

In assessing the strength and persistence of US growth, it is important to recognise the impact that inventories and net exports continue to have on headline results. Inventories added significantly to growth through the first half of 2015 on rapid inventory accrual; but a more modest pace of stocking in Q3 resulted in a 1.4ppt subtraction from quarterly GDP growth. Similarly, while net exports reduced the annualised Q1 headline outcome by 1.9ppts, it subsequently added modestly to growth in Q2, circa 0.2ppts.

If we omit both factors from our assessment (and thereby focus on domestic final demand, DFD), we see a robust, enduring underlying growth trend. Annualised DFD growth in 2015 averages out at 2.7% – or 3.3% if we focus solely on the past six months, when the weather was more favourable. Together with the 2014 average of 3.1%, the 2015 outcome implies that the past two years have seen considerably stronger underlying growth versus the 2011–13 period, when annualised DFD growth was running at just 1.5%.

Of the components of DFD, the standout has been consumption. Initially concentrated in durable and non-durable purchases, consumption momentum broadened into the services sector through 2014–15, with the average quarterly gain over that period twice what it was during 2011–13. To the extent that services are generally domestically produced and more labour intensive than goods, this trend is of great import to the US’ economic health.

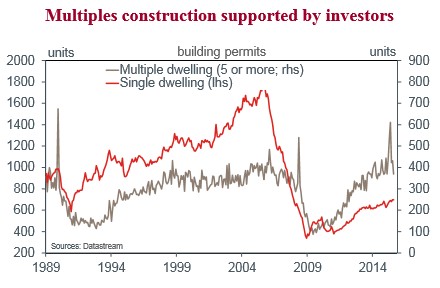

As the balance sheet impact of the GFC has receded, household spending has also spread to residential investment. House prices have now seen substantial gains since the trough, freeing upgraders to reconsider their housing needs; credit availability has also improved markedly. Paradoxically, reduced home ownership has also aided residential investment of late. This is because small and large investors have stepped in to profit from the need for greater rental stock, building new apartments to lease out for yield (and in time, capital gain). This trend has received additional support in major metropolitan areas from strong foreign interest for new-build apartments. Dwelling investment rose at a 6.1% annualised pace in Q3, and by 8.9% over the year.

Business investment remains the primary disappointment of this recovery. This was again the case in Q3. After a 25% post-recession surge over the 15 months to June 2012 and a likely energyinduced 13% swoon over the year to March 2014, non-residential construction activity has since been flat – the declining price of oil arguably a key impediment. Remaining spare capacity and the strength of the US dollar are likely to keep pressure on structures investment for the foreseeable future.

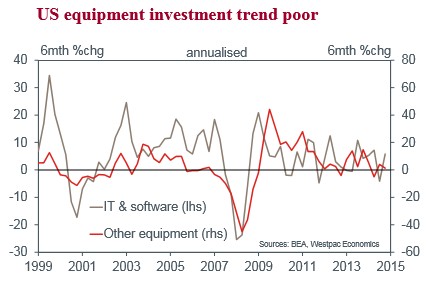

Equipment investment by US firms has also been very disappointing in 2015. Despite a 5.3% annualised gain in Q3, growth over the past year stands at just 0.7%yr. That is down from a (brief) peak of 10.2%yr a year ago. As for construction, the oil price and strong US dollar have been key factors behind this weak trend. Yet they are not the sole contributors. Since the beginning of 2011, annualised growth in equipment investment has averaged 6.7%. This is only marginally above the pace we see as necessary for the maintenance of the capital stock, let alone its expansion.

As we have highlighted on numerous occasions, US firms continue to use financial efficiency to boost profitability. This sees corporates borrow to buyback shares and engage in M&A activity instead of undertaking real investment in new capital.

On the whole, stripping away the impact of inventories and net exports, the past two years have seen a material improvement in the growth trend. This acceleration has primarily been the result of stronger consumption growth, particularly within the services subsector and in housing construction. Given the ongoing improvement in the labour market and credit availability as well as robust consumer confidence, this trend should endure into 2016.

For the FOMC, this provides a strong argument to begin the normalisation process in December, despite headline inflation being well below target. A better underlying demand backdrop for the first rate hike seems unlikely. How growth responds to the first hike will dictate the scale and timing of the overall normalisation process.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.