A shaky start to the week that will culminate in the long awaited FOMC Meeting overnight, followed by a slew of very important CPI prints that could shake central banks out of their deflationary stupor. Stocks fell around 1% in Europe after a scratch day in Asia as tensions rise in the South China Sea, with modest falls in the US as earnings results created no real interest. Commodities were sold off, especially oil as it continues its fall to key support as inventory levels rose while gold marched time alongside most sovereign bonds as US Treasury yields head to the elusive 2% level again and German bunds were heavily bid.

On the datafront, UK GDP came in a bit lower than expected for the year while in the US its durable goods orders for September was better than expected on the headlines, but the internals lacked robustness.

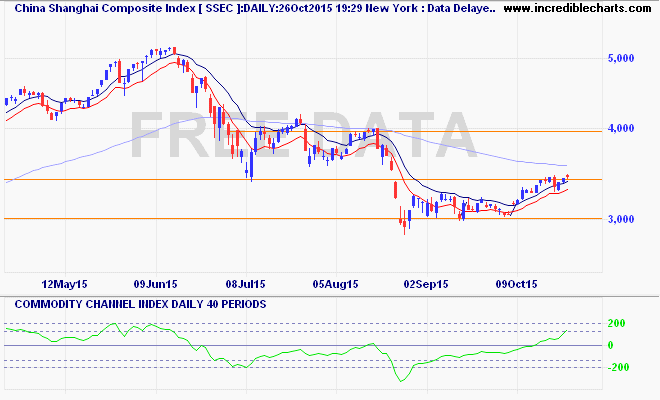

Recapping Asia’s session where the Shanghai Composite barely meeked out a positive day remaining just above 3400 points. Again, this is not a decisive follow through on the back of the interest rate and reserve rate cuts, and as the 200 day moving average crossover approaches, we should be seeing a bear market rally right back up to 4000 points but internal momentum remains weak: