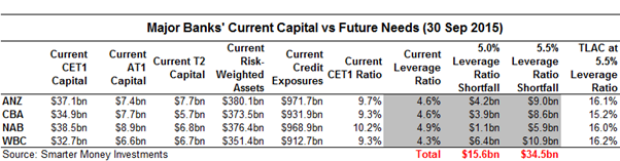

The next big story for the banks will likely derive from the government’s decision to embrace the FSI’s recommendation that APRA introduce a minimum leverage ratio of up to 5 per cent. My analysis indicates that even after raising $31 billion in equity, the majors’ leverage ratios remain well below 5 per cent (see table). Significantly, Westpac is by far the worst at just 4.3 per cent, which is miles below the median peer bank globally and may explain its more aggressive attempts to expand mortgage margins (more equity raisings are coming).

If APRA only lifts the minimum leverage ratio to 5 per cent (as Switzerland did this week), the majors will have to find another $15.6 billion of tier one capital, which will put them around the 50th percentile peer bank globally. It is, however, hard to fathom how APRA could define this as “unquestionably strong” given that the 75th percentile bank is at 6 per cent. If we suppose that the de facto target ends up being around, say, 5.5 per cent, the majors will have to accumulate an extra $34.5 billion in tier one equity over what they have currently (asset growth lifts that number by about 6 per cent annually). The neat thing about a 5.5 per cent leverage ratio is that it also gives the majors “total loss absorbing capacity” (TLAC) of 16 per cent, which is set to become the standard for the biggest banks by 2019.

All of this is very achievable and will furnish investors and taxpayers with materially lower risks.

Correct, but they’ll be bleeding capital via bad debts long before then! That’s why this current chase for yield rally tipping into renewed RBA cuts is the bank’s last great party.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.