Shanghai is flat today but its rebound has come to an interesting inflection point:

The downtrend is broken and we have the beginnings of rising channel which is approaching long term resistance. A breakout here would set up a run towards 4000 points, unwise certainly, but who the Hell knows with the Shanghai shocker.

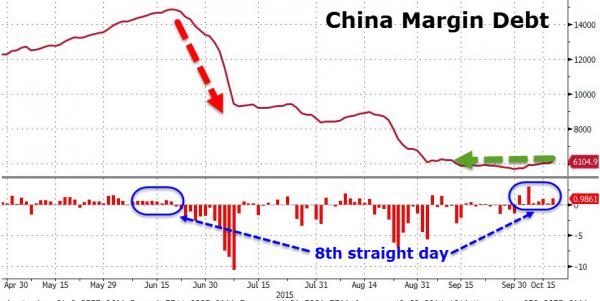

Investors traded 5 billion shares on the ChiNext Composite Index on Oct. 16, more than at any point during this year’s rally. The Shenzhen gauge, dominated by small technology companies, is up 33 percent from its Sept. 15 low. Traders have borrowed extra debt to buy the city’s stocks for seven days straight.

The resurgence in appetite for China’s smallest, most volatile and most expensive equities contrasts with an almost-dead futures market and a more muted rebound in Shanghai, where volume remains less than half its peak. The world’s second-biggest economy expanded last quarter at the slowest pace since 2009, according to figures published on Monday.

“With macro indicators not looking great, investors are speculating that the government will roll out stimulus to help technology companies,” said Steve Wang, chief China economist at Reorient Financial Markets Ltd. in Hong Kong. “They seem to believe it’s easier to flip small stocks for quick gains.”

Adding to the lunacy, there has also been a sudden turn up in margin lending volumes though we are far from the bloom of the past year, from Zero Hedge:

As I’ve said many times, the index adds next to nothing economically but it will inevitably (and bizarrely) lift Western market sentiment if it runs again. My own guess and it is 100% punt – is that it will fall over again and go lower yet.

“We cannot know whether [emerging markets] have reached a bottom, but we do know that the markets are no longer presuming the best of outcomes and the fierceness of the sell-off of highly cyclical stocks and commodities worldwide looks very much like capitulation of a bear trend,” said Kerr Neilson, Platinum Asset Management’s founder and managing director, in his quarterly update.

The billionaire investor said he was pleased with the opportunities the sell-off had created.

Mr Neilson said, regarding China: “In an environment of low inflation where incomes are rising, the prospects for consumer-focused companies are still favourable. The art is to correctly price each individual opportunity.”

How can a value investor possibly persist in a communist casino that has no capacity for price discovery?

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

Investors traded 5 billion shares on the ChiNext Composite Index on Oct. 16, more than at any point during this year’s rally. The Shenzhen gauge, dominated by small technology companies, is up 33 percent from its Sept. 15 low. Traders have borrowed extra debt to buy the city’s stocks for seven days straight.