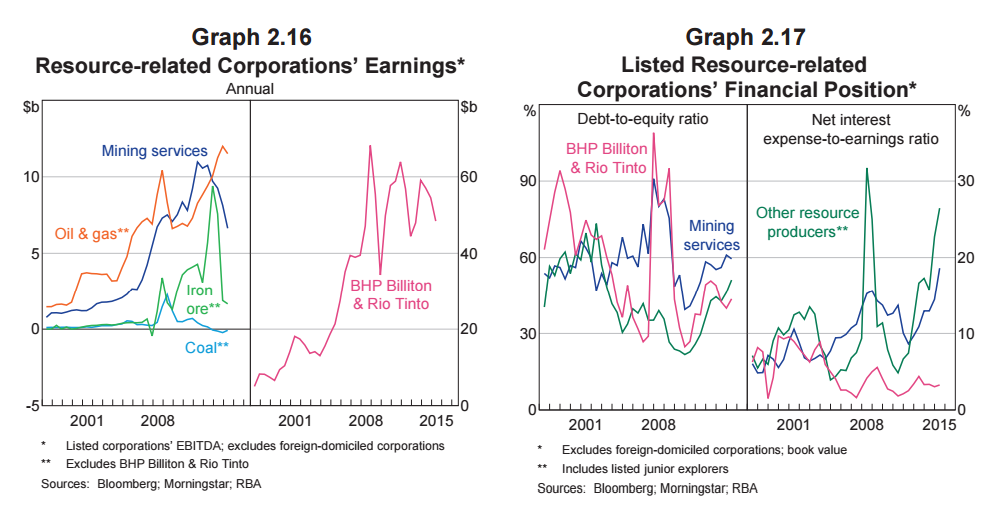

In contrast to the benign overall conditions in much of the business sector, risks appear to have increased further in the resource-related sector over the past six months. The sustained falls in coal, iron ore and oil prices are weighing heavily on the earnings and cash flow of producers of these commodities, particularly those higher up the cost curve. Most smaller producers are struggling to cover costs at current prices, with many already reporting losses. Where producers have been cutting costs to preserve profit margins, further cuts could prove progressively harder. The dwindling investment pipeline and ongoing cost-cutting by resource producers have in turn reduced the output and earnings of mining services companies. Overall, the earnings of businesses in the resource-related sector have fallen sharply over the past two years, although consensus analyst forecasts point to some recovery in earnings over the coming years (Graph 2.16).

Bank lending to the resource sector has increased rapidly in recent years, and large resource producers have increased their issuance of debt into financial markets, especially offshore, even as they cut investment spending. Higher debt and the steep fall in profits have resulted in a significant rise in the debt-servicing ratios of smaller resource producers; the aggregate debt-servicing ratio of listed mining services companies has also risen (Graph 2.17). Although the debt-servicing capacity of many of the smaller resource producers has been supported by strong liquidity positions to date, continued low commodity prices would erode these positions in time. Indeed, some smaller resource producers have come close to breaching debt covenants and a range of firms have had their credit ratings downgraded. Putting further pressure on their debt-servicing ability, resource-related companies may face difficulty rolling over their debt, with the bonds of some companies currently trading at very high yields. Despite the low business failure rate, banks indicated in liaison that the performance of their resource-related loans had deteriorated somewhat. They also noted that the low level of interest rates could be masking underlying stress in this sector.

In line with these developments, a market-based measure of default risk for listed corporations – derived from equity prices and reported liabilities – suggests that the financial health of some parts of the resource-related sector has deteriorated noticeably as commodity prices have fallen. Over the past year, the distance-to-default estimated for the more vulnerable (and usually smaller) resource producers and mining services companies have fallen to their lowest levels since the financial crisis (Graph 2.18).

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

In line with these developments, a market-based measure of default risk for listed corporations – derived from equity prices and reported liabilities – suggests that the financial health of some parts of the resource-related sector has deteriorated noticeably as commodity prices have fallen. Over the past year, the distance-to-default estimated for the more vulnerable (and usually smaller) resource producers and mining services companies have fallen to their lowest levels since the financial crisis (Graph 2.18).