AMP has five reasons why we’re not in a global bear market:

China is not collapsing: company earnings show little sign of a ‘hard landing’, continuing to grow at a healthy pace

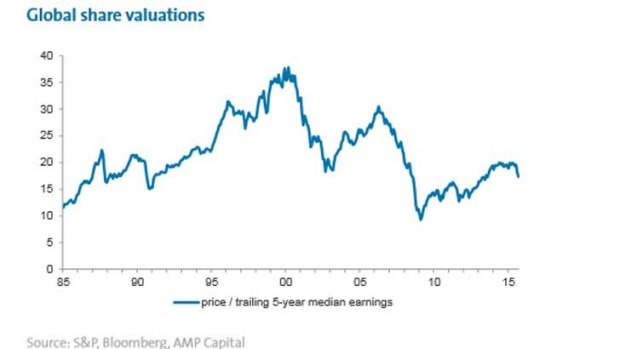

Shares aren’t too expensive: global valuations do not point to excessive optimism in shares

US interest rates won’t rise much: the Fed is only expected to tap the monetary breaks over the next few years. European and Japan central banks may even step up unconventional easing

Banks are better capitalised: banks have increased equity by over two trillion US dollars since the financial crisis. Confidence in the banking system to absorb shocks is just as important as the ability to absorb them

House price overvaluation relatively concentrated: house prices look overvalued in New Zealand, Canada, Australia and Belgium. A rapid adjustment in any of these markets would hurt the respective local economies but would not undermine the global economy or banking system.

Versus the reality:

China was never collapsing. This is a bull’s straw man. It is, rather, in structural adjustment to lower and less commodity-intensive growth. This is what I describe as a “glide slope” that is destroying global commodity prices and commodity-dependent emerging market economies.

Which shares are not expensive? Australian, no, for good reason, we’ve got no earnings growth. But everywhere else is bloody expensive.

The reason US rates won’t rise much is because growth sucks hitting earnings. If the ECB and BOJ ease then the US dollar will remain strong making point one worse.

Banks are not much better capitalised.

Try looking at house prices in emerging markets like China, Brazil and India and tell me they’re not overvalued.

Advertisement

This is a bear market based around emerging markets and commodities. It could play out as either a lost decade or a bust in those markets. It may be slow moving enough to appear like something else but it ain’t.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.