Cross-posted from Investing in Chinese Stocks.

First-tier cities are not going to revive the national housing market by themselves, but if there’s a national recovery, first-tier cities are likely to lead the way. WSJ Blog: Why Some Chinese Cities Boom Amid Property Bust

China’s richest cities – called first-tier cities – are generally regarded as Beijing and Shanghai as well as the southern manufacturing hubs of Guangzhou and Shenzhen. Experts say there are signs that Shanghai and Shenzhen in particular are overheating.

Average new home prices in Shenzhen are up 31.3% year-over-year in August, according to official data, much higher than the next highest year-on-year growth of 5.6% recorded in Shanghai.

…“The demand and supply dynamics in Shenzhen are vastly different from any other Chinese city,” he said.

The news out of Beijing, at least, says this move may be fading. According to data from 5A Home Loan Services, mortgage transactions fell 15% from the first half of October. This is significant because Beijing sales were weaker in the first week of September due to the military parade in Beijing, so the comparison period is a favorable one. Home sales are also falling in early October:

According to the chain of home network Institute data show that during the National Day holiday this year (10.01-10.07) Beijing secondary residential net signed volume is 101 units, compared with last year increased by 45 units, an increase of 80.4%. But in the second week of October (10.05-10.11), Beijing 1565 sets of existing home transactions, net signed volume decreased by 47.6%. The actual time between the online record and the actual signing of the contract is a week or so, so this number reflects the actual situation of existing home sales during the national holiday, which is also a direct cause of the decline of mortgage transactions in the first half of October.

There’s still optimism though, from Ifeng:

In the second-hand housing transactions, home network chain LI Qiao-ling Institute believes that since September the central bank continued introduction of further easing of monetary policy will boost the market, second-hand housing turnover is expected in the coming weeks there will be further increased.

A niche recovery looks a prospect, thanks to rising prices, the trend in Beijing will be towards luxury housing, from Ifeng:

Yesterday, after 104 rounds of intense competition, Gezhouba to 4.95 billion yuan, with the construction of 41,000 square meters of public rental housing, 61,800 square meters to move back to the room price to win the Fengtai District Huaxiang fanjia village land. Analysts pointed out that, after subtracting the public rental and other land area, the floor price of the land has exceeded 75,000 yuan per square meter, can be said that the floor price of Beijing residential high.

It is understood that from June 2015, Beijing appears far more than premium prices phenomenon. Dawei that this proves the first-tier cities housing prices to compete for land. Future high-end real estate projects will become a trend.

And of this is the best China can do then a very bearish Nomura is too bullish, from CN Gold:

Nomura Forex Jens Nordvig, general manager of research directors report that the bank is now on China’s GDP growth is expected at the low end, it is expected to only 5.8% GDP growth next year, but even so let everyone feel low data may also be compared High actual level, because Nomura forecast for investment in infrastructure may be biased optimistic. That is, in the next year China’s infrastructure spending grew about 20% of GDP is expected to grow 5.8 percent premise.

However, if infrastructure spending did not reach the level of about 20 percent of China’s economy will be like?

Report that infrastructure may indeed have less than expected, growth has plummeted since 2009. And there are also short-term lack of attractive items such risks. If the overall growth of China’s investment next year unchanged this year, assuming that other Nomura projected expenditure unchanged China, then China next year GDP will grow by only about 3.5%.

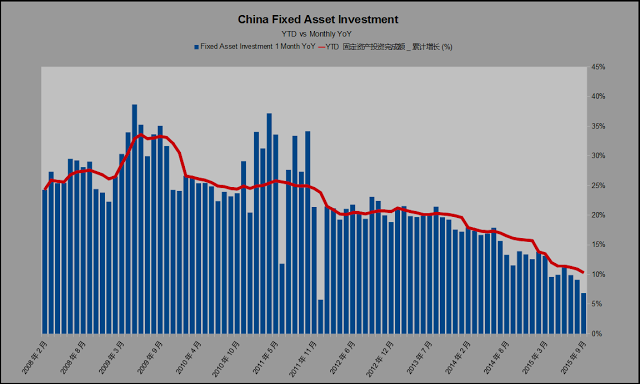

To review, fixed asset investment slumped to a 7% yoy rate in September, from the 10% rate of the prior few months. The trend points to fixed asset investment going lower, not higher.

If you assume China hasn’t rebalanced much, and you look back at old models of GDP growth (old as in a couple of years ago), GDP should already be much lower. From June of last year:

The IMF once estimated that a 1% decline in China’s real estate investment would shave about 0.1% off China’s real GDP within the first year. And so a 7.5ppt deceleration in real estate investment growth would drag down GDP growth by about 0.75ppt.

Real estate investment growth was down 17% since then, or 1.7% of GDP growth from June 2014. Maybe the model is junk, but actually most economist think real estate in much more important. Also from that post:

About 60% of China’s manufacturing and financing activities are related to the property sector, China’s state media quoted a senior government economist as saying Monday.

The GDP number might be artificial, but the underlying data points (electricity, real estate investment, fixed asset investment) aren’t being massaged and all paint a clear picture: slowdown. NBS isn’t lying about GDP and lying about investment because they wouldn’t put out such negative sub numbers. The investment figures are real and represent a real slowdown in the economy. Copper, iron ore, oil, steel and other commodities say the same thing: slowdown. To an extent the GDP figure is irrelevant because the oil market, outside of speculation, doesn’t care about GDP numbers, it cares about how many people show up to buy and sell today. It matches buyers to sellers and that’s the price. For markets that lack price discovery, such as currency and debt markets, you have Shrodinger’s Cat in the box with the CCP and PBoC keeping you from opening the lid.