the bond market is clearly not pricing default risk properly;

the bond market has taken a few SME bond defaults in stride and seems to be counting on bail-outs of the few SOE bonds that are reportedly facing default risk; and

leverage in the bond market is rapidly building up.

On the current trajectory, we doubt the market can stay stable beyond a few quarters, especially if some SOE and/or LGFV bonds indeed default.

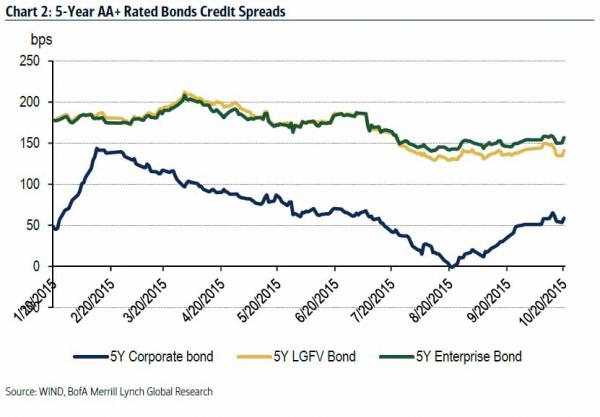

When a developer can issue a 5y bond at 3bp lower than 5y quasi-sovereign CDB bond’s yield, the market appears grossly mispricing risks in our view. Credit spreads of LGFV, corp. and enterprise bonds are all at or close to five-year lows at the moment.

Investors are chasing yield, due to rapid money expansion (M2 at 13.1% in Sept vs. 6.2% nominal GDP growth in 3Q). AUM of bond and money market mutual funds expanded by Rmb1.6tr Jan-Sept and by Rmb1.3tr alone since July after the A-share correction vs. Rmb44.1tr bond outstanding as of Sept.

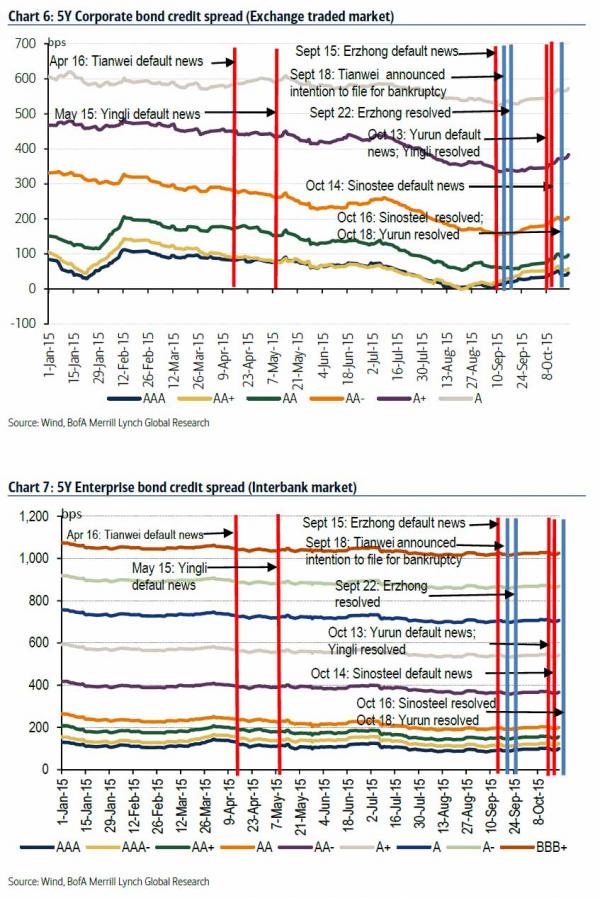

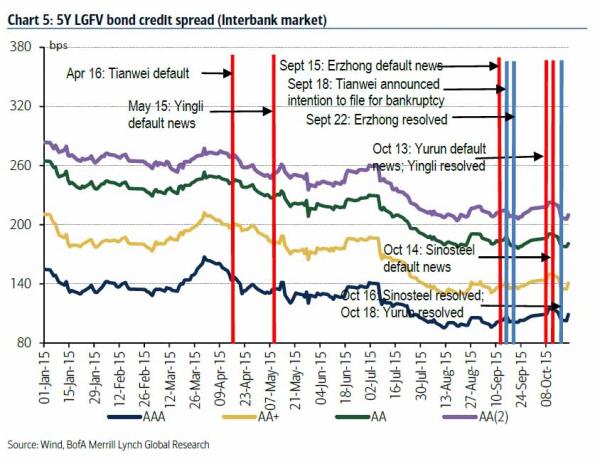

Moral hazard is playing a key role – there is no official default so far in the bond market other than some small SME bonds. Credit spreads narrowed on most occasions when major bond default threats surfaced, suggesting that most investors probably counted on bail-outs (Chart 5-7). Meanwhile, about 2/3 of repos are on less than 7-day term.

Chinese “markets” are really warped. When default risk triggers bond buying you know you’re stuffed. Anyway, if the bubble does go then we can expect to see even more rate cuts and greater pressure on the yuan to fall again.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.