From Bill Evans:

Our current forecast is for the Australian dollar to finish the year around $US0.68 and fall further to $US0.66 in the first quarter of 2016. It is currently around $US0.725 and is looking strong. However we are sticking with our view for a number of key reasons.

These are mainly around the Federal Reserve; commodity prices and Australia’s chronic external deficit.

Markets remain in denial about the Fed. Current market pricing is for a 25 per cent chance of a rate hike in December and only two hikes in total by the end of next year. With our expectation of a move in December, markets will have to quickly reprice the profile for the course of 2016.

The case for a move in December is much stronger than implied by market pricing. In September, 13 of the 17 members of the Federal Open Market Committee indicated that they expected rates to be rising by the end of the year. More importantly, Chair Yellen indicated publicly that she expected to raise rates by year end. That was supplemented by Vice FOMC Chairman Dudley who also expected that rates would rise by year end. Recall that it was Dudley who shifted his position on the September move to “less compelling” following the market gyrations in August.

The argument against raising rates has always been around the low level of inflation. Both Chair Janet Yellen and her deputy at the Board of Governors Stanley Fischer have recently addressed this issue. The Chair calculated that of the 1.6 percentage points inflation is currently printing below the 2 per cent target, 0.8 percentage points is down to falling energy prices; 0.6 percentage points is down to the 15 per cent increase in the US dollar over the previous year and only 0.1 percentage points is due to slack in the economy.

The contribution from the slack in the economy has fallen from 0.5 percentage points in 2013 and 0.3 percentage points in 2014. Stability in energy prices and the US dollar would soon see inflation bounce back to 1.6 per cent and, arguably, a tightening labour market could see further near term pressure on the inflation rate. Fed speakers have consistently argued that inflation does not need to be back at 2 per cent to justify higher interest rates – only that there is a reasonable prospect that inflation will reach 2 per cent. Given the extent of the moves, some stability in energy and the US dollar seems to be a reasonable assumption.

The recent slowdown in US jobs growth has further weakened the case for a Fed move according to market assessments. Contrasting the current three month average gain of 167k against the 2015 average of 198k and the 2014 average of 260k highlights that, while not weak overall, there has been a distinct loss of momentum in job creation during the past 12 months.

With the unemployment rate having fallen near to levels typically viewed as consistent with full employment, a moderation in the pace of jobs growth should not necessarily be a concern for policy makers. Much faster jobs growth is normal in the recovery phase compared to the consolidation phase.

The key question then is whether the deceleration in jobs growth has largely run its course and will stabilise at these recent solid rates or whether it is the beginning of a more substantial trend deterioration that would put at risk the current low level of unemployment. There will be two more jobs reports before the December FOMC meeting.

Our second likely downward force for the Australian dollar is the outlook for the iron ore price. In 2014 BHP Billiton reported income from its iron ore business of $12.1bn. In 2015 that income fell to $6.9bn. However that performance could have been a lot worse. Specifically, if management had taken no action, income from iron ore activities would have fallen to $3.1bn due to the collapse in the price. Part of the difference came from ramping up production ($1.8bn). That was complemented by $2.0bn in cost savings. Various industry estimates point to both BHP Billiton and Rio Tinto now lowering their cost bases to $25-30 per tonne. That is a solid profit margin compared to spot prices around $56 per tonne. It is reasonable to expect that the supply of iron ore will be boosted at current prices. Over the year Australian exports of iron ore have lifted by an impressive 11 per cent and recent export figures point to a further lift in sales.

On the demand side we can comfortably look at China. China produces 50 per cent of the world’s steel output and 70 per cent of that steel goes into domestic construction market. We have recently seen some evidence of stability emerging in the Chinese housing market with house sales rising and prices increasing in Tier 1 cities. But, to date, starts continue to fall as developers deal with large unsold inventories. Overall we expect that steel production will be flat over the next twelve months suggesting that demand will not be strong enough to absorb the likely increase in supply. Downward pressure on iron ore prices is likely to also pressure the Australian dollar.

Weaker commodity prices and a narrowing interest rate differential with the US are a reliable combination to push the Australian dollar lower. A third factor is the ugly trade deficit, which is driving a deterioration in Australia’s broader external balance, which is also a key variable in our fair value model.

In August, Australia’s trade deficit surprised by widening out to $3.1bn. Indeed the cumulative trade deficit over the last 6 months reached an impressive $18.4bn. That is the largest cumulative 6 month deficit since March 2008 ($18.45bn) when household spending was booming.

Despite modest import demand, rising commodity supply and a clear improvement in services trade (now non resources exports are around equal with resources exports), weak commodity prices have left their mark on the deficit.

While we expect most of this damage to the Australian dollar to occur in the 6 months to March next year markets are likely start to reassess the 100 per cent probability of an RBA rate cut by next March. That will provide some support for Australian dollar but the major damage is likely to already have been done.

The exchange rates currently prevailing represent an opportunity for Australian importers to secure US dollars at levels that we would be most surprised to see persist into 2016. For multinationals looking at tactical repatriation or profit hedging decisions, the same reasoning applies.

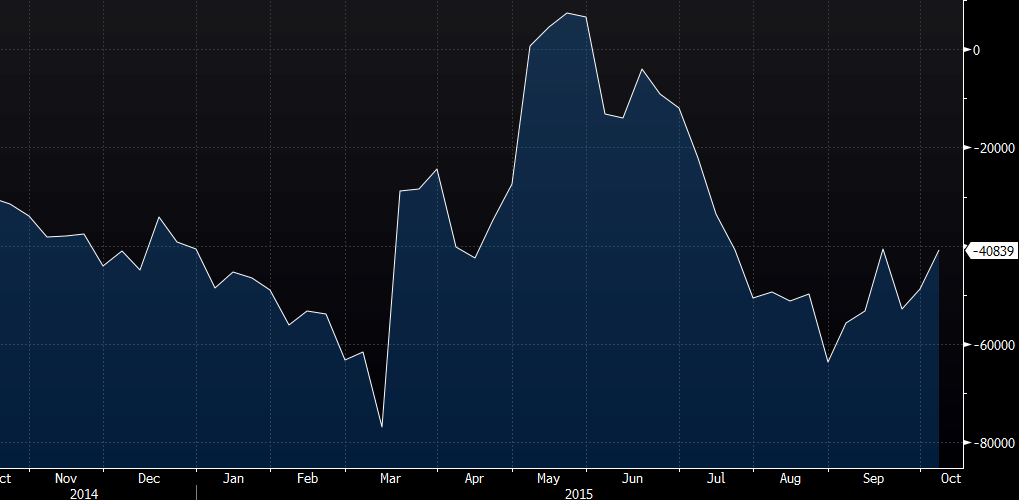

That’s right. Certainly the larger trend for the Australian dollar remains down. Bill is right about China and iron ore, is too bullish on Australia, though for the dollar that is reversed by his view on the deficit, and is far too hawkish on the Fed. The odds favour the Fed tightening entering an extended pause without swinging to more QE so once the short squeeze in the Aussie passes the roll over will come. However, the bias remains up for now with the market still very short Aussie at -41k contracts (from the last week’s CFTCCOT) no doubt on lingering views of Fed hawkishness:

I’d expect a much bigger washout of the shorts before we can stabilise.