by Chris Becker

The Westpac-MI Leading Index was released this morning and it makes for dour reading in addition to highlighting Westpac’s own cognitive dissonance with its near-delusional growth forecasts.

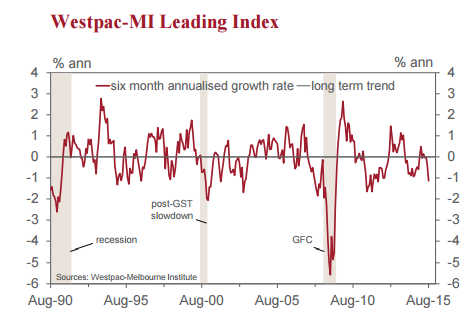

Here are the core points:

The economy seems to be losing momentum as we move through 2015. In the first four months of 2015 the average growth rate of the Leading Index was 0.16% above trend. That seemed to be a welcome lift in momentum from the second half of 2014 when the average growth rate was 0.67% below trend. However in the last four months the growth rate has slowed from 0.03% below trend to 1.14% below trend.

The longer term view which looks “vulnerable”:

- This emerging below trend growth profile for the economy is certainly in line with our own views.

- Note that the June quarter national accounts confirmed that Australia’s six month annualised growth slowed to a 2.1% pace in the first half of 2015 with our forecast for the second half of a still below trend 2.5%.

- Looking further out we expect growth in 2016 of 2.7% (recently revised down from 3.0%).

- With trend growth in the economy now likely to be nearer 2.75% than 3% our forecast for GDP growth in 2016 of around trend growth looks a little vulnerable based on this recent print from the Leading Index.

Headline GDP growth rates are near useless in this context, as this is supported almost wholly by net exports due to volumes, with household income continuing its decline, the residential construction boom waning and the jobs market steady but with huge slack.

The interest rate trajectory remains pretty clear too, with the growth outlook for next year looking gloomy, the RBA is unlikely to move maybe even through to 2017, according to Bill Evans:

This print of the Leading Index is casting some early doubt around the Bank’s forecast of 3% growth for 2016. However the Bank is still expecting that the unemployment rate has stabilised despite growth in 2015 likely to be in the 2-2.5% range.

A particularly important point here is that the make-up of growth seems to be more ‘jobs intensive’ than we may have expected, with the lift from dwelling construction, household expenditure and net services exports being particularly important. The Board is very likely to await more evidence around the labour market and specifically the beneficial impact on the jobs market resulting from the sharp fall in the Australian dollar before it moves again.

At Westpac we do not expect any further rate movements before 2017.

At MB, we do and its down. The Bill Evans roll over will be fun!