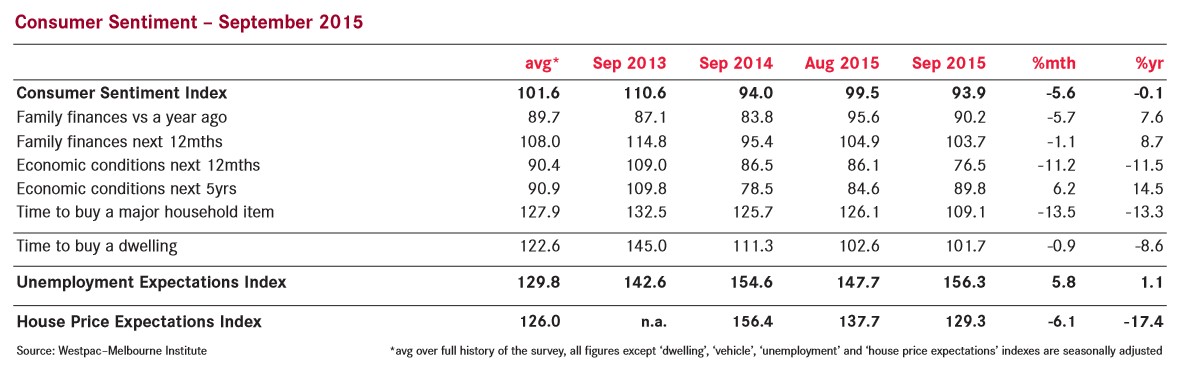

Westpac has released its consumer sentiment index for September, which registered a sharp 5.6% decline, from 99.5 points in August to 93.9 points in September. Below is Westpac chief economist, Bill Evans’, commentary:

This solid fall in the Index comes as no surprise. We were somewhat puzzled by the surprise increase in the Index last month of 7.8% and there was always likely to be some correction this month. Of course the deluge of disturbing news around violent gyrations in both Australian and overseas equity markets; poor economic data from China; a disappointing report on Australia’s growth rate and the weakness in the Australian dollar were also likely to have unnerved households.

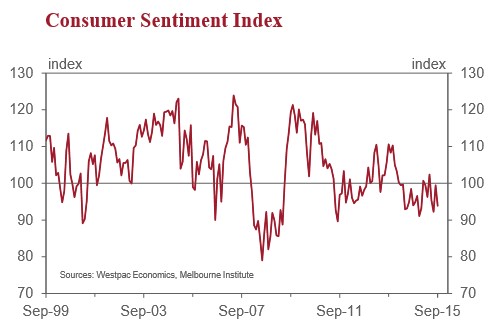

This print on the Index now marks the 17th out of the last 19 months that the Index has been below 100. A level of the Index below 100 indicates that pessimists outnumber optimists. After acknowledging some volatility in the series the underlying picture is that confidence has been little changed over the last year – firmly stuck below 100 and averaging around 96.

For the September survey we also ask respondents about the news items they most recall. This provides an objective test of our assumptions around the factors driving the movements in the Index. For this survey the most recalled news items were around domestic economic conditions overseas issues. Nearly 42% of respondents recalled overseas news items – the second highest proportion on records back to 1975. The highest proportion came in December 2011 (55%) when the European financial crisis was dominating headlines. Domestic economic conditions (54%) were also important this month. Respondents were significantly more negative around domestic conditions than in June.

News on the Australian dollar was noted by 15.5% of respondents – the highest on the dollar since June 2002.

The government would be pleased to see that ‘Budget and taxation’ caught the attention of only 23.1% of respondents compared to 62.7% in September last year.

This heightened concern around the world economy unnerved respondents about the labour market. Almost all respondents who recalled news items about the jobs market noted that the news was unfavourable. There was a sharp 5.8% increase in the Westpac– Melbourne Institute Index of Unemployment Expectations (a higher print indicates heightened employment concerns). The Index is now at its highest read since December 2014.

Most of the components of the Westpac-Melbourne Institute Consumer Sentiment Index fell in September. Households responded negatively around their own finances. The sub-index tracking assessments of ‘family finances vs a year ago’ fell by 5.7%, while that tracking expectations for ‘family finances over the next 12 months’ fell by 1.1%. Nevertheless, both of these components is comfortably higher relative to September last year (7.6% and 8.7% respectively). The volatile sub-index tracking expectations for ‘economic conditions over the next 12 months’ fell by 11.2% (down 11.5% over the year) while the sub-index tracking expectations for ‘economic conditions over the next five years’ increased by 6.2%.

However, the biggest move came from the sub-index tracking assessments of ‘time to buy a major household item’ which fell by 13.5% to be down by 13.3% over the year. While the fall in the ‘finances’ components would explain part of this fall the near 5% drop in the Australian dollar since the last survey may have discouraged purchasers who will now be expecting higher import prices.

Confidence around the housing market continues to erode. The ‘time to buy a dwelling’ index fell by 0.9% to be 8.6% down on a year ago and 30% lower than two years ago. The New South Wales Index continues to underperform with a 14% fall this month to be 34% down on a year ago and 55% over the last two years. Within that Index the Sydney component is down by 46% over the last year and has reached its lowest level since the survey began in 1975.

House price expectations are also waning. The Westpac House Price Expectations Index fell from 132.7 in August to 127.3 in September (down by 6.1%). This Index is now down by 17% over the last year although remains well above 100 indicating that more respondents still expect prices to continue to rise.

This month we also asked respondents about their choice of the wisest place for savings. Bank deposits remain the most popular choice at 27% (down from 29.4% in June). However this was lowest proportion registered since September 2009.

This evidence of lower risk aversion is further highlighted by the lift in real estate as a favoured form of saving. The proportion of those respondents favouring real estate increased from 24.6% in June to 28.2% in September. This represents the highest proportion of respondents favouring real estate since September 2003 – the last time we had an investor-led boom in real estate.

The increase in the proportion favouring real estate is likely to be capturing the improving optimism of investors in the housing market whereas the deteriorating prints on the ‘time to buy a dwelling’ index is probably reflecting affordability concerns of upgraders and first home buyers. In that regard note that the Westpac – Melbourne Institute Index of House Price Expectations continues to point to rising prices, albeit at a slower pace.

The Reserve Bank Board next meets on October 6. We expect the Board will maintain its steady rates policy for the remainder of this year and throughout 2016.

The key to any decision to further cut rates, as expected by the financial markets, will be whether the Bank’s current forecast that the unemployment rate can stabilise around current levels proves sustainable. Despite soft economic growth, jobs growth has been strong over the past year partly because of the strong contribution to jobs from the improving export services sectors. A sustained deterioration in the jobs market will not be apparent until next year complicating the market’s expectations of a rate cut by year’s end.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.