by Chris Becker

The Reserve Bank of New Zealand is having its monthly interest rate meeting on Thursday with expectations of a 0.25% cut to the currently 3% OCR all but baked in. This will have important ramifications for the Australian dollar as the August print for unemployment in Australia will be released shortly after on the day.

Why the cut? Like Australia, New Zealand’s little economy is tied to the commodity cycle, namely agriculture. Dairy prices have fallen as Chinese demand moderates, driving down corporate profits as well

Here’s UBS take, via Forexlive:

We see a subsequent move to 2.5% as the risk scenario (i.e. less than 50%), and below that as unlikely. Nonetheless, we expect the RBNZ to keep its options open.

In terms of forecasts, the above-3% forecast this year will be downgraded but that may only be focused on the near term. Look for a forecast of 2% or 2.5%. If medium/long-term forecasts are left unchanged, that’s a signal that the RBNZ is at or near the bottom.

Inflation forecasts will also be lowered but the reason the RBNZ may be close to a base in interest rates is that the fall in the New Zealand dollar is inflationary.

Growth forecasts have been tumbling across the Tasman as well, down to 2.5% and maybe even further as unemployment continues to rise to nearly 6%.

The problems the Kiwis face, in a similar vein to Australia, is both an outbreak of tradable inflation as the currency drops and a continuation of major capital city bubbles. Although inflation expectations are subdued – barely flicking along below 2% according to the RBNZ- as Roger Kerr at Interest.co.nz explains, outside of the beleagured agricultural sector and helped along by robust construction and tourism sectors as well as lower interest rates (most of the major banks just cut their rates again, outside of the RBNZ) inflation could rise sharply:

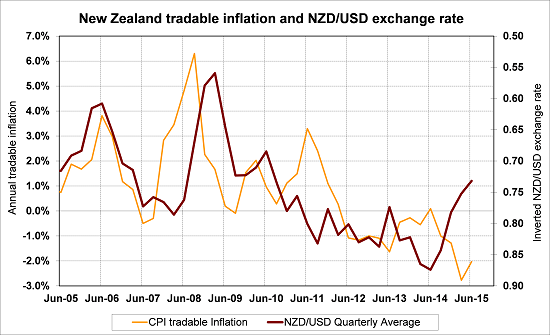

The historical correlation between the NZD/USD exchange rate and tradeable inflation has always been very close.

The 28% depreciation in the NZD/USD rate from 0.8800 to 0.6300 over the last 12 months reliably points to annual tradable inflation increasing from -2.00% to well above +1.00% over coming months.

As the chart below depicts, the quarterly average for the NZD/USD exchange rate (red line) will continue to fall to below 0.7000, potentially suggesting even higher tradable inflation to +2.00%.

On the assumption that non-tradable inflation (domestic prices not impacted by the exchange rate) remains stable at its current +2.0% level, the overall annual CPI inflation rate looks set to increase sharply from +0.4% to over 2.00% over the next nine to 12 months.

This is the problem when dealing with a global currency war – the race to devaluation – when you’ve let inflated asset markets get into bubble territory.